Carbon Border Adjustment Mechanism: basic notions

· 6 min read

This article is part of Carbon Academy, a new illuminem series exploring the essential concepts within the world of carbon.

In our article on Compliance Carbon Markets, we highlighted carbon leakage as a significant issue within these markets and pointed to the Carbon Border Adjustment as a key measure adopted by the EU to address this concern. Here, we provide the basics of this policy tool, with information directly sourced from the EU website, and break it down into easily understandable terms.

A Carbon Border Adjustment (CBA) is a policy tool designed to address concerns related to the competitiveness of domestic industries in the face of varying carbon prices between different countries.

The concept involves imposing a charge on the carbon content of imported goods to ensure that they face a similar carbon cost as domestically produced goods, thereby preventing companies from relocating production to regions with lower environmental standards.

The Carbon Border Adjustment strive to achieve 4 key objectives:

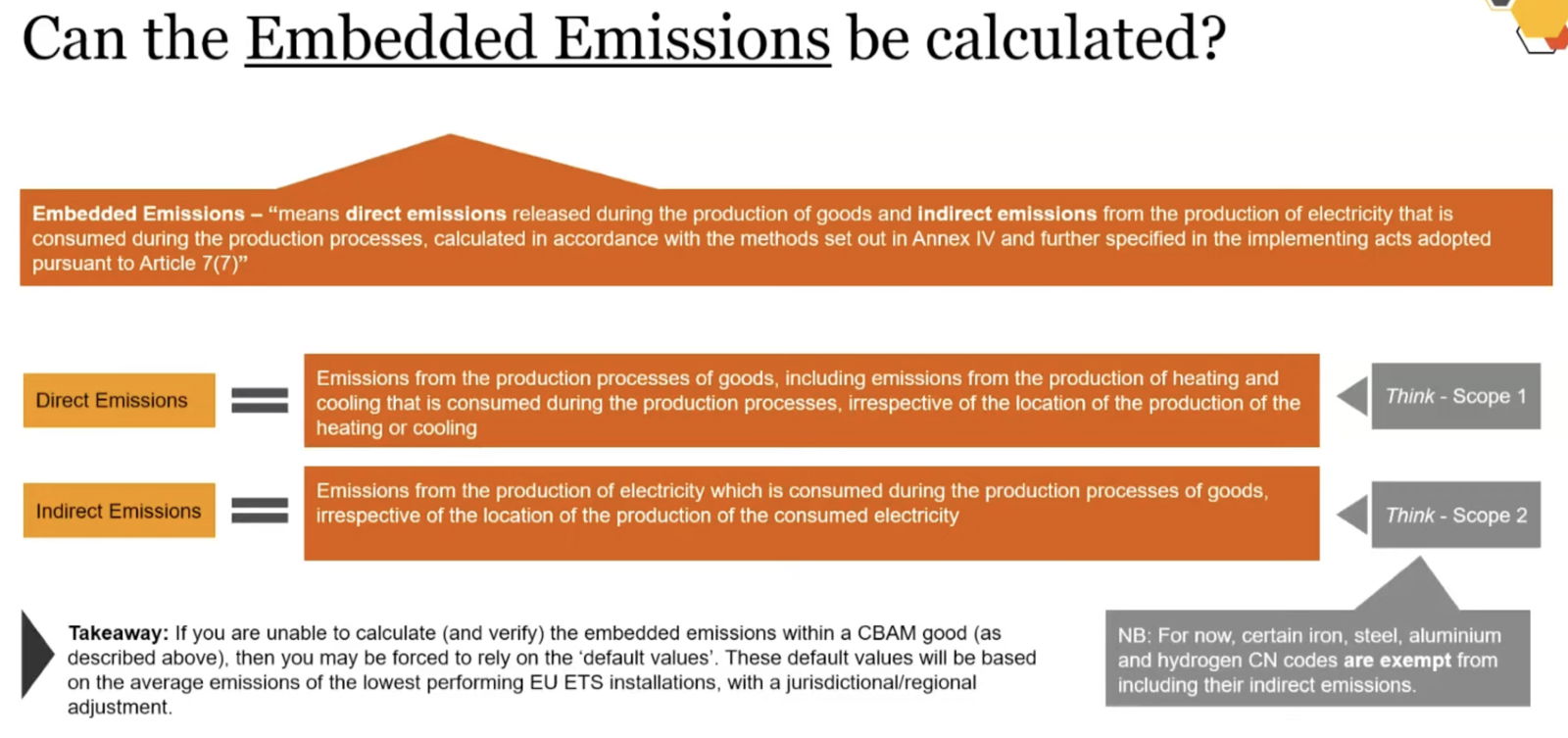

The CBAM works as follows: EU authorized declarants, representing the importers of certain goods, will declare embedded emissions within their imports. Embedded emissions are both direct emissions released during the production of goods and indirect emissions from the production of electricity that is consumed during the production process. The infographic below clarifies this concept:

Source: PwC

Embedded emissions will be calculated based on the carbon data provided by the supplier to the importer. Importers will then purchase and surrender CBAM certificates based on the embedded emissions of their imported goods and surrender the corresponding number of certificates at the same price they have been purchased. This will become compulsory in 2026 (see below ‘Timeline’). The certificates surrendered by the CBAM declarant shall correspond to the amount of embedded emissions of the relevant goods expressed in tonnes of CO2.

Question: what if suppliers cannot or don’t want to provide details/data needed to do the CBAM reporting? This presents a significant issue within the CBAM. Currently, the CBAM reporting system lacks a legal framework requiring suppliers to disclose data, placing the responsibility squarely on importers. In cases where suppliers resist sharing data, importers may eventually seek alternatives, such as relying on default values.

The CBAM initially applies to imports of goods in the following sectors:

Importers have two options for calculating emissions reductions:

CBAM will go through two main phases: a transitional and a definitive period

Within the framework of the EU ETS, the allocation of free allowances diminishes across all sectors as time progresses. The Carbon Border Adjustment Mechanism (CBAM) will be phased in gradually as free allowances decrease. Particularly for CBAM sectors, this reduction rate will escalate starting from 2026, ensuring that the EU ETS effectively contributes to the EU's ambitious climate objectives. The cost of these certificates will be directly linked to the EU Emission Trading System (EU ETS) allowance price. Once the full CBAM regime becomes operational in 2026, the system will adjust to reflect the revised price of EU ETS allowances. The price will be based on the weekly average auction price of EU ETS allowances, expressed in € per tonne of CO2 emitted. The goal of this approach is to harmonize the carbon pricing for imported goods with those produced within EU ETS participating installations.

N.B. At its core, the Carbon Border Adjustment Mechanism (CBAM) applies to imports from all non-EU nations. However, countries with their own emission trading systems are exempt. An authorized CBAM declarant can apply for a reduction in the number of CBAM certificates to be surrendered if non-EU producers have already paid for embedded emissions under a carbon emissions reduction scheme, whether in the form of a tax, levy or fee or in the form of emission allowances.

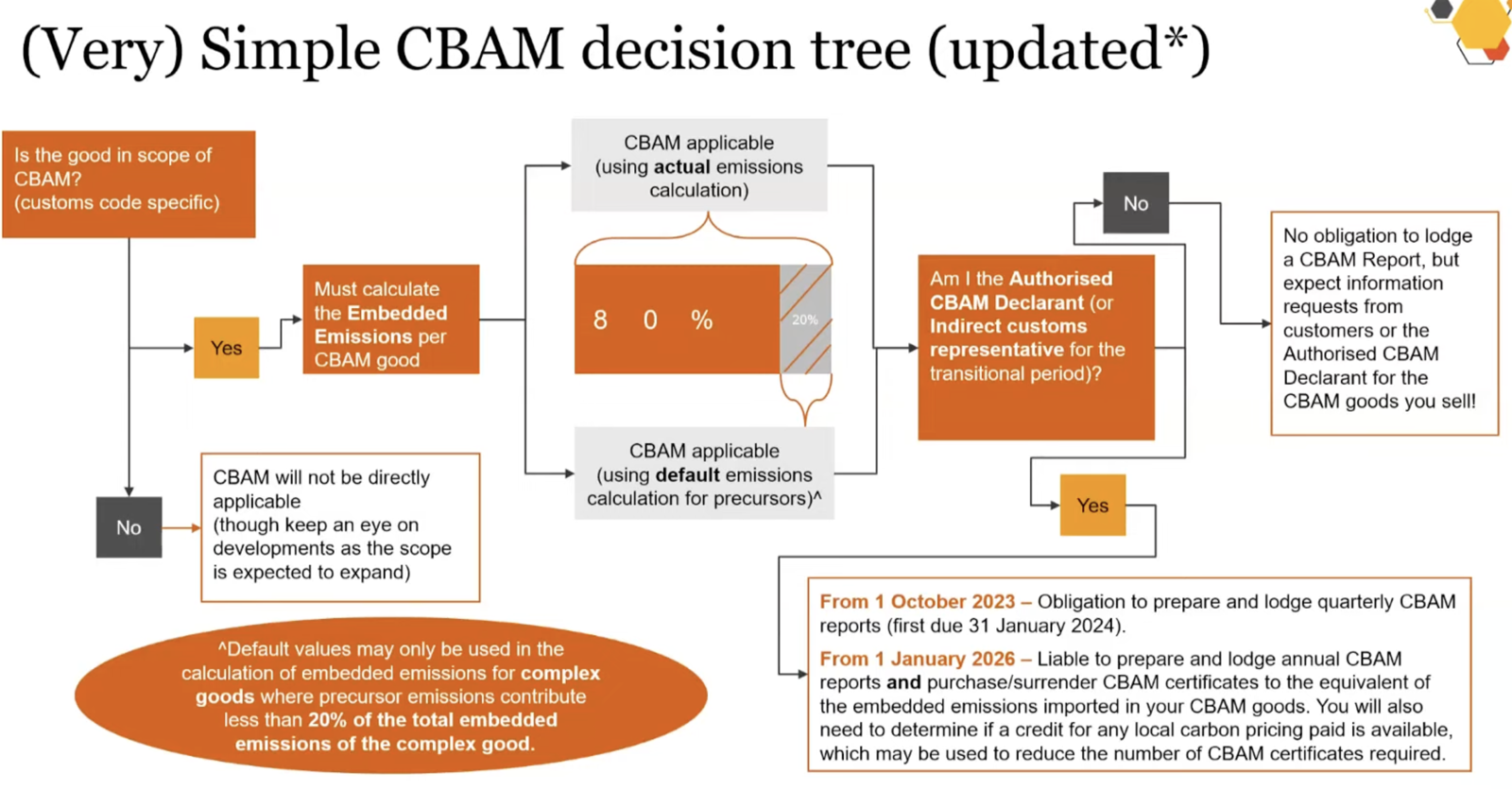

The infographic below provides a recap of the functioning of the CBAM scheme:

Both Reporting of embedded emissions (from 1 October 2023) and the purchase of CBAM certificates (from January 2026) are compulsory.

Each Member State has appointed a National Competent Authority (NCA) tasked with verifying the accuracy of the quarterly CBAM reports, with support from the Commission. In instances where CBAM reports are found to be missing, incorrect, or incomplete, the National Competent Authority (NCA) may impose penalties ranging from EUR 10 to EUR 50 per tonne of unreported emissions.

The purpose of the CBAM extends beyond mere compliance—it's a crucial support for the EU's heightened climate ambitions. It safeguards against the risk of relocation to regions with less stringent policies. Simultaneously, it incentivizes non-EU producers to adopt greener practices and encourages other nations to implement carbon pricing measures. In essence, the CBAM's purpose is to track and report emissions directly associated with the production processes of products subject to its regulations.

Are you a sustainability professional? Please subscribe to our weekly CSO Newsletter and Carbon Newsletter

illuminem briefings

Effects · Climate Change

illuminem briefings

Public Governance · Climate Change

illuminem briefings

Public Governance · Climate Change

The Economist

Nature · Environmental Sustainability

UNDP

Adaptation · Climate Change

Offshore Energy

Carbon Capture & Storage · Carbon