Hydrogen deployment in the road transportation sector (II/II): US decarbonization strategy

· 26 min read

Co-author: Raqib A. Chowdhury (M.S. Candidate in Energy Policy and Climate. The Johns Hopkins University)

To read Part 1 of this article click here.

As discussed in the previous section, the absence of sufficient hydrogen fuel supply and hydrogen infrastructure; high costs; disadvantages of domestic decarbonization policies; the necessity to improve safety codes/standards and fueling protocols for medium/heavy-duty vehicles are potential risks to successful hydrogen deployment in the road transportation sector. At the same time, the abundance of domestic natural resources, the plethora of existing and developing technologies, storage and liquefication resources; supportive domestic pro-hydrogen policies; and the advantages of FCEVs in contrast to BEVs and ICEs represent the prospects for this specific decarbonization strategy in the United States.

Section 2 describes the methodology and the purpose of this study, which is the presentation of a specific roadmap to reach NREL's economic potential for the road transportation sector in the Lowest-Cost Electrolysis scenario, where hydrogen is widely utilized as a vital solution for significant decarbonization in the United States. This scenario results in the most significant reduction in the usage of petroleum (15%) since it has the highest level of FCEV penetration: 5 MMT per year of hydrogen fuels 22% of medium/heavy-duty vehicle fleet, and 12 MMT per year of hydrogen fuels 26% of light-duty trucks and 18% of light-duty vehicles. This maximum level of FCEV penetration is possible due to the highest availability of affordable electrolytic hydrogen. Under this NREL scenario, about 90% of the hydrogen is produced through the LTE process, with the remaining 10% nuclear HTE. NREL researchers state that "an increased hydrogen market size can be realized even if low-cost LTE is unavailable as long as other hydrogen production options are available" (Ruth et al., 2020, p. xiii). Such options are 1) SMR with affordable natural gas, 2) biomass, and 3) low-cost HTE, even if limited to the use of nuclear energy only. The hydrogen market size may increase if HTE hydrogen production technology can employ supplementary cost-competitive energy resources (grid electricity with natural gas-generated heat or affordable, dispatch-constrained electricity from nuclear, wind, and solar generation) (Ruth et al., 2020).

In the conclusion of the report, which informed the methodology of this study, NREL researchers suggest several paths for future analysis of the transition from current infrastructure and market conditions to five future scenarios of hydrogen deployment. The researchers recommend that future analysts identify potential regulatory and market modifications in hydrogen deployment, the timing of R&D investments and initial commercialization of hydrogen applications, specific regions for regional support decisions, and near-term opportunities for hydrogen as a vital energy carrier (Ruth et al., 2020).

This research study strives to extend the NREL research in describing the ambitious decarbonization strategy, which deploys hydrogen in the US road transportation sector. The highly optimistic and aggressive growth strategy consists of four phases: 1) 2022-2024 (immediate steps), 2) 2025-2027 (short-term scale-up); 3) 2028-2032 (mid-term steps), and 4) 2033-2050 (long-term roll-out). The strategy facilitators are 1) policy facilitators and 2) hydrogen fuel and supply chain facilitators. First, policy facilitators play an important role "since they are needed to create the right incentives to help the private sector invest and develop the hydrogen market" (FCHEA, p. 13). Policy facilitators cover policy support (federal, state, and municipal), public initiatives for bridging economic barriers to initial market launches, and the establishment/improvement of hydrogen standards (safety and fueling protocols). Second, hydrogen fuel and supply chain facilitators outline specific steps for hydrogen integration into the road transportation sector, namely technological attempts to increase hydrogen fuel availability, hydrogen infrastructure/FCEVs developments, and initiatives to lower costs throughout the entire hydrogen supply chain. The hydrogen supply chain includes equipment manufacturers, infrastructure operators, FCEVs manufacturers, etc. The next section describes "Immediate Steps" (2022-2024).

Under Section 40314 of the Bipartisan Infrastructure Investment and Jobs Act (HR. 3684), policymakers develop National Energy Strategy for Hydrogen during the first phase. The nationwide deployment of hydrogen in the road transportation sector cannot happen without the supportive pro-hydrogen regulatory framework at the federal, state, and municipal levels. This policy framework is also needed to encourage private investment into hydrogen production and the supply chain for the road transportation sector. Hart (2020) explains the federal government's critical role in assisting energy transition and ensuring competitiveness by funding R&D efforts for advanced technologies, supporting financing to the private sector through the tax code, providing debt financing to innovative projects, spreading information about best practices, and purchasing goods and services.

While devising the national strategy, the policymakers rely on the current DOE's Hydrogen Program Plan, namely on established coordination and collaboration with other federal agencies, such as the Department of Defense, to identify areas of common interest and prospects/risks in hydrogen deployment for road transportation (DOE, 2020c). For instance, the Office of Naval Research Global Tech Solutions Program sponsors the Massachusetts Institute of Technology (MIT)'s research to convert aluminum into hydrogen fuel for all kinds of vehicles in expeditionary environments (Eurasia Review, 2022). Such innovative R&D efforts might benefit remote area-hydrogen deployment in the road transportation sector.

The policymakers also draw on the current Program's coordination and collaboration with several state governments to ensure the activities' integration at the federal, state, and municipal levels. Such activities include public outreach and education, real-world demonstrations, and early-market deployments. In addition, the policymakers utilize the best practices from the Program's engagement with the stakeholders from the private and non-profit sectors. For instance, the Program has developed vital partnerships that support the integration of R&D efforts between the government, private sectors, and academia, focusing on the US road transportation sector. Such partnerships are US DRIVE (Driving Research and Innovation for Vehicle Efficiency and Energy Sustainability) and the 21st Century Truck Partnerships with VTO, which focuses on advancing the next generation of medium/heavy-duty trucks, including the usage of hydrogen fuel cells (DOE, 2020c). The policymakers also benefit from the engagement with other stakeholders, such as the Fuel Cell and Hydrogen Energy Association (FCHEA) or private-sector-based associations and coalitions.

Other steps, informed by FCHEA (2020), occur during the initial two-year period. First, the federal and state governments establish solid, technology-neutral decarbonization goals and remove regulatory barriers. However, as Gross (2020) warns, "policymakers must ensure that their actions do not crowd out further advances in new fuels, especially hydrogen" (p. 17). Such awareness helps prevent drawbacks from decarbonization policies, as mentioned in Section 3. Second, dedicated policymakers increase awareness about hydrogen safety through public outreach to the federal and state-level officials and the general public. Third, other changes happen, namely, the implementation of hydrogen codes and safety standards, establishment of fueling standards for medium/heavy duty vehicle fleets, modernization of existing hydrogen-related regulations, and the establishment of hydrogen-related workforce programs.

Lastly, in this phase, California and other Section-177 states implement specific FCEV targets with existing zero-emission vehicles (ZEV) mandates or low-carbon fuel emissions standards. According to FCHEA (2020), Section 177 of the Clean Air Act allows states to adopt California's instead of federal standards. These progressive states can continue encouraging heavy-duty FCEV adoption by supporting FCEV purchase programs and infrastructure. State governments can also lead in FCEV adoption by gradually switching to an FCEV fleet while balancing this procurement with the BEV adoption in specific market segments. Additional policies focusing on FCEV user advantages (public cost-neutral incentives) and compensation policies for FCEV purchase programs support vehicle adoption. Eventually, other states, the follower states, can also follow similar roadmaps in developing clean energy policies and supporting hydrogen deployment. At the end of this phase, National Energy Strategy for Hydrogen helps solidify national targets and approaches for large-scale hydrogen deployment, particularly in the road transportation sector.

During the first phase (2022-2024) and in the second phase (2024-2026), the creation of Regional Hydrogen Hubs ($8 billion funding over four years) helps increase hydrogen fuel availability for the road transportation sector. According to John (2022), this law requires at least one of the hubs to be used for pink hydrogen, at least one for blue hydrogen, and two other ones for green hydrogen production. There are multiple proposals for such Regional Hydrogen hubs. For instance, HyDeal LA public-private consortium seeks to produce green hydrogen to replace fossil fuels for transportation and a large portion of natural gas used for power generation and heating. The project needs funding for $27 billion over the next fifteen years, including the cost of new pipeline infrastructure and underground storage (John, 2022). Second, a Utah consortium, the Advanced Clean Energy Storage project, is expected to be the world's largest industrial-scale green hydrogen production and storage project. On April 26, 2022, this project received $504.4BB in debt financing from DOE's Loan Program's office (MP, 2022). Third, nuclear energy producers want to use excess nuclear electricity to produce pink hydrogen in Xcel Energy's Prairie Island and Arizona Public Service's Palo Verde nuclear plants. There are other promising projects for clean hydrogen production in New York and other states (John, 2022).

The federal funding for the Clean Energy Electrolysis Program ($1 billion) and R&D grants ($500 million) during the first and second phases help reduce hydrogen deployment costs. Other steps suggested by FCHEA (2020) also increase hydrogen fuel availability for the road transportation sector: 1) dedicated hydrogen production for ground transportation, 2) scaling up hydrogen production through water electrolysis (10-50 MW electrolyzers); 3) as a bridge technology to LTE-produced hydrogen, usage of large-scale hydrogen production from SMR or ATR with renewable natural gas and mid-scale hydrogen production (SMR/ATR) with CCUS.

The expansion of hydrogen's use for decarbonizing the US road transportation sector is connected with the growth of hydrogen's infrastructure. The current clean hydrogen projects are built on bilateral arrangements between hydrogen purchasers and producers (John, 2022). In the first phase, multilateral agreements for clean hydrogen are arranged for the hydrogen industry to grow to scale. Such arrangements involve multiple producers and buyers in the road transportation sector, preferably developing Regional Hydrogen Hubs. Such mutually-reinforcing networks in various regions can grow hydrogen's supply and demand in the road transportation sector.

Other steps in developing hydrogen infrastructure involve addressing hydrogen transportation, storage, and distribution (dispensing and fueling). The National Academy of Sciences (2008) advocates the "phased introduction" of FCEVs and fueling stations, starting from major cities and moving to other cities in phases. In so doing, "the so-called lighthouse concept reduces infrastructure costs by concentration the development in relatively key areas termed 'lighthouse cities'" (p. 78). During the first phase, liquid and gaseous distribution are developed throughout "lighthouse cities" and pioneer states.

In addition, according to FCHEA (2020)'s suggestions, the following immediate steps take place: 1) integration of hydrogen-tolerant equipment, 2) rollout of second-generation FCEVs and hydrogen fueling stations for buses and light-duty vehicles, and 3) rollout of heavy-duty FCEVs and related fueling stations. R&D efforts are also essential in overcoming the infrastructure challenges described in Section 3, namely, improving the reliability of materials used in the compressors and new designs for cryogenic transfer pumps, compressors, and dispensers to ensure they have sufficient throughout the medium-heavy-duty vehicle fleet. The following section describes "Short-Term Scale-Up" (2025-2027).

In the second phase, aggressive expansion of hydrogen production and infrastructure helps maintain momentum in hydrogen deployment in the road transportation sector. Federal support remains critical in removing any regulatory barriers toward using hydrogen in the US decarbonization, as per the country's broader Nationally Determined Contributions (NDC) declarations (DOS, 2021a). The private sector is incentivized to implement NDC goals to create a resilient, net-zero future. In pursuit of such targets, informed by FCHEA (2020), state policies remain essential in the pioneer states and the follower states, which have started pursuing decarbonization goals on a larger scale. In the pioneer states, local governments support the minimum hydrogen infrastructure expansion for coverage in its core markets. Such efforts can be undertaken through technology-neutral subsidies, joint ventures funded by large industrial conglomerates, market-based policies, or request-for-proposal (RFP) funding. In addition, the follower states pursue the pioneer states’ strategies, focusing on measures covering the FCEV cost difference with the incumbent technology (ICE) and supporting the expansion of hydrogen infrastructure. In other words, in the second phase, federal and state incentives, primarily in the early pioneer markets, assist in transitioning from government support to large-scale market-based mechanisms.

During the second phase, the utilization of Regional Hydrogen Hubs continues to grow the large-scale hydrogen fuel supply for the road transportation sector. The federal funding for R&D and demonstration projects for novel clean hydrogen-related technologies and the increase in demand from the road transportation sector also decrease hydrogen costs. The Clean Energy Electrolysis Program proves to be successful as the federal grant recipients reach the main Program's goal – a reduction in the cost of hydrogen production using electrolyzers to less than $2/kg by 2026. The mechanism for coordination between US National Laboratories, research institutes, and universities instills additional innovation into clean hydrogen production. In general, during this phase, the US witnesses the growth in the industrial-scale hydrogen production, a reduction in the cost of electrolyzers, and an increase in hydrogen demand from its road transportation sector.

Other strategies, informed by FCHEA (2020), continue expanding the hydrogen supply and improve all parts of hydrogen infrastructure for the road transportation sector. For example, as economic factors connected to electrolyzers continue to improve, industrial companies can ramp up large-scale LTE hydrogen production of more than 50 MW and the smaller production facilities at remote fueling stations. This development fosters the usage of hydrogen for the integration of variable renewable electricity production and transportation demand on a large scale. At the same time, innovations occur, such as successful industrial-scale demonstrations of SMR or ATR with CCS, which can also be dedicated to hydrogen production for the road transportation sector.

On the hydrogen infrastructure side, informed by FCHEA (2020), the following steps take place: 1) the introduction of pure hydrogen-tolerant equipment and 2) the integration of dedicated hydrogen delivery systems in industry clusters. The road transportation sector continues to transform as new and improved FCEVs are brought to market, for example, to meet the California Fuel Cell Partnership goal of 1 million FCEVs by 2030. Heavy-duty vehicle infrastructure grows as fueling stations get introduced through the follower states, and second-generation heavy-duty vehicles are presented throughout the US. Multiple hydrogen producers and buyers from the road transportation sector continue arranging multilateral arrangements for the buildout of clean hydrogen projects in additional Regional Hydrogen Hubs.

In addition, federal grants toward R&D efforts in the Infrastructure Investments and Jobs Act support innovation in the second phase, reducing fuel cells' costs. The cost of a fuel cell accounts for nearly half of the investment cost for FCEVs (Moriarty & Honnery, 2019). As mentioned in Section 3, the main contributor to the cost of a fuel cell is the catalyst, which is based on the platinum group metals that are highly dependent on imports. Promising R&D projects lead to the commercialization of technologies. For example, in 2020, the multi-institutional group discovered the non-platinum catalyst that can lead to longer-lasting and cheaper power (The Source, 2020). Another promising project from UCLA/Caltech found out that altering fuel cell catalyst shape can lower costs since it requires only 1/50 as much platinum as a regular smooth one (UCLA, 2016). In the second phase, it is assumed that these technologies are commercially ready for widescale deployment within the US. The following section describes "Mid-Term Steps" (2028-2032).

By the end of the third phase, the US achieves emissions reductions of 50% below the 2005 levels, which is critical for the decarbonization of the road transportation sector (DOS, 2021b). The following developments are informed by FCHEA's (2020) futuristic projections. First, the full-scale deployment of medium/heavy-duty vehicles is scaled up, supported by the strategic placement of fueling stations along the high-usage of freight corridors. The regional infrastructure networks start connecting to create a nationwide network to assist the coast-to-coast travel. Light-duty vehicles and buses continue to disseminate beyond the pioneer states. More importantly, "hydrogen production has been scaled up, the critical infrastructure has been put in place, and hydrogen equipment is manufactured in scale" (FCHEA, 2020, p. 73). In other words, the US is on the stable trajectory of deploying hydrogen broadly in its road transportation sector.

Such developments are possible due to the continuing federal and state policies, which support the transition from direct government support to large-scale market-based mechanisms. In the pioneer states, industrial conglomerates, supported by tax incentives and FCEV targets, expand the fueling network through investment in critical locations. Local governments develop dependable ZEV strategies and targets in the follower states, including FCEVs in all market segments.

During the third phase (2028-2032), the DOE "Hydrogen Shot" initiative reaches its goal of slashing the costs of clean hydrogen (green, pink, blue, or turquoise) to $1/kg by 2030. The LTE-based hydrogen production increases in the states, where dedicated variable solar and wind generation keeps electricity costs low. Moreover, a nationwide portfolio of small modular nuclear reactors (SMRs), which will start replacing the traditional reactors in the 2030s, produces pink hydrogen at a stable, affordable cost and a high-capacity factor. Andrews and Jelley (2017) describe various types of SMRs under consideration, such as LWRs and fast neutron reactors (FNRs) in addition to molten salt reactors (MSRs). Within an MSR, the operators use the uranium fuel and dissolve it in a sodium fluoride salt coolant, which circulates through a graphite moderator. The high-level waste is reduced due to the continuous removal of fission products and recycling of the actinides. The plant maintains a high operating temperature for hydrogen production during the process. Since there is a passive cooling of a core, the safety of the SMR is also improved.

Informed by FCHEA (2020), other steps in the roadmap, which increase hydrogen fuel availability and infrastructure for the road transportation sector, occur. For example, electrolyzer production costs reduce capital and operating costs due to the increasing volume of manufacturing processes. Blue hydrogen also scales up as CCS and CCUS technologies develop to support increasing hydrogen demand in the road transportation sector.

Hydrogen infrastructure expands as the production of fueling station components and fuel cells for all types of FCEVs scales up. The private sector also gets fully involved in developing FCEVs and hydrogen dispensing (fueling stations). The road transportation players learn best practices from the Hydrogen Mobility Europe project (H2ME) initiative, which supports the deployment of FCEVs and fueling stations across the European Union (Hydrogen Mobility Europe, 2022). In addition, hydrogen distribution has expanded further since dedicated hydrogen pipelines began to connect industrial-scale clean hydrogen sites with demand centers focused on the road transportation sector. The next section describes "Long-Term Roll Out" (2032-2050).

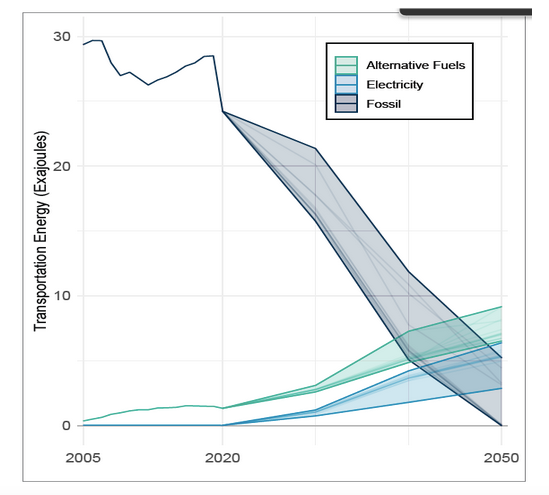

By the end of 2050, the US is very close to achieving net-zero GHG emissions goals articulated in The Long-Term Strategy of the United States - Pathways to Net Zero Greenhouse Gas Emissions by 2050. Such accomplishment is possible due to the coordinated action based on four strategic pillars: federal leadership, innovation, non-federal leadership, and all-of-society action (DOS, 2021b). It is anticipated that specific transport segments, especially the FCEVs, achieve cost parity with fossil-fuel alternatives. Additional policy support fully corrects for externalities between FCEVs and ICEs. Figure 5 shows how, from 2020-to 2050, electricity and alternative fuels (hydrogen, bio-energy) will become primary fuel sources in the road transportation sector.

On the policy front, consistency and acceleration in policy implementation remain crucial in achieving net-zero GHG emissions in the United States. During this phase, informed by FCHEA (2020), federal policymakers focus on building a comprehensive hydrogen code and standardizing hydrogen practices across the country to enable broader deployment in the road transportation sector. Federal regulations also recognize LTE-based hydrogen production as one of the leading technologies in increasing hydrogen fuel supply for the industry. In addition, best practices and lessons from the pioneer states are disseminated across the rest of the country to deploy hydrogen in the road transportation sector in the most efficient way. Lastly, carbon tax proposals get broader support across the US as an efficient way to increase revenues while encouraging lower GHG emissions past 2050, especially in the road transportation sector.

After 2032, according to the FCHEA (2020), hydrogen is being deployed broadly throughout the US economic sectors, especially in the road transportation sector. This expansion of hydrogen usage leads to further cost reduction across the entire value chain in hydrogen deployment, particularly in the road transportation sector. Both production and hydrogen infrastructure for the road transportation sector reach maturity and continue to expand to meet the increase in the US transportation demand. According to FCHEA (2020), other steps happen, such as 1) retrofitting SMR/ATR capacity with CCUS due to policy incentives or climate regulations and 2) competition between LTE production and SMR/ATR plus CCS production due to the search for lower-cost production.

Hydrogen infrastructure continues to evolve as efforts are made to upgrade existing gas infrastructure to withstand high hydrogen integration. At the same time, if required, new hydrogen-compatible pipelines are built throughout the nation. The full hydrogen deployment into the road transportation sector is complete as the US obtains a large-scale clean hydrogen production network and an efficient infrastructure. The variety of vehicle models for light/medium/and heavy-duty markets are readily available for US customers.

This study describes a specific strategy to decarbonize the US economy: unlocking hydrogen’s potential in the US road transportation sector. The strategy is intended to become a potential part of the US portfolio of decarbonization approaches to reach net-zero GHG emissions by 2050. The study affirms that hydrogen is a crucial piece of the US decarbonization puzzle. It also shows that, given many opportunities, challenges, interdependencies, and tradeoffs, the decarbonization of the US road transportation sector is a complex issue. The analysis in this paper draws on domestic/international case studies and quantitative indicators to describe challenges and opportunities for hydrogen deployment in the road transportation sector. The study’s methodology is also informed by NREL methods to estimate hydrogen's economic potential as an energy carrier, a transportation fuel for light-medium-heavy duty FCEVs in the contiguous United States. This research study uses NREL’s economic potential estimation for the road transportation sector, calculated in the most ambitious, Lowest-Cost Electrolysis scenario. NREL researchers warn that “we identify the economic potentials for several scenarios but do not consider how to reach those potentials” (Ruth et al., 2020, p. 116). This analysis aims to extend NREL’s research by describing a four-phase ambitious decarbonization strategy that deploys hydrogen in the road transportation sector from 2022 to 2050.

As with every research, this study is not without limitations. The limitations of the study’s methodology are connected to the limitations of NREL's methods for estimating hydrogen's economic potential as a transportation fuel in the road transportation sector. In acknowledging NREL’s analysis limitations and needs for additional analysis, its researchers describe the necessity for 1) the supplementary analysis of the threshold prices for hydrogen applications; 2) the cross-cutting analysis of the light-duty vehicle market; 3) a construction of the supply curve for HTE integrated with grid electricity and heat generation from natural gas, biogas or another feedstock, 4) detailed cost estimates for future HTE and LTE technologies to increase the confidence in supply curves, 5) supplementary analysis to ascertain the economics of regional hydrogen markets and to estimate exports/imports across the US regions, 6) analysis of potential policy implications on both regional and national hydrogen demand and supply curves, 7) sensitivity analyses for price variations (natural gas and petroleum prices) and impact of regional hydrogen exports/imports on hydrogen market sizes, and, lastly, 8) incorporation of effects of the competition for hydrogen-producing/enabling resources (land, water and variable renewable/clean electricity sources) on hydrogen prices (Ruth et al., 2020).

In Section 3, this analysis may benefit from an additional discussion about the impact of lifespan challenge on hydrogen deployment in the road transportation sector. Lifespan challenge for vehicles is a critical issue since ICE vehicles, especially in the medium/heavy-duty segment, can stay around for a long time. Gross (2020) claims that heavy trucks have a lifespan of 15 years. Therefore, it might take decades for a novel technology to be spread throughout the vehicle fleet, especially if introduced slowly (McCollum et al., 2009).

The proposed decarbonization strategy has limitations as well. First, as acknowledged earlier, this strategy represents the most ambitious pathway for quickly ramping up the hydrogen deployment in the road transportation sector. All barriers (technological, infrastructural, economic, political, and standards-related) need to be surpassed to achieve favorable decarbonization outcomes. Undoubtedly, it would be challenging to achieve NREL's targets for hydrogen production under the Lowest-Cost Electrolysis scenario. Under the scenario, about 90% of the hydrogen is produced through the LTE process, with the remaining 10% nuclear HTE (Ruth et al., 2020). Perhaps, during the first two phases, the US might employ an alternative mix of technologies (proposed by NREL) to ensure a rapid scale-up of hydrogen fuel supply for the road transportation sector. Second, due to enormous decarbonization challenges, a longer deployment time might be necessary to scale hydrogen deployment in the sector. Third, the paper only focuses on hydrogen deployment in the road transportation sector, disregarding the roll-out of other decarbonization technologies, like vehicle electrification. Perhaps, a multi-technology approach, a scale-up of both FCEV and BEV charging infrastructures, will lead to faster decarbonization that is faster and more cost-effective, serving all US customers based on their specific needs. Lastly, due to the lack of access to special transportation-related modeling tools, the strategy's authors primarily focus on qualitative recommendations and provide quantitative indicators whenever possible. The rigorous modeling assumptions and outcomes, incorporating all NREL methodology limitations, may have led to better decarbonization approaches.

Regardless of the presented shortcomings, this study extends the current literature concerning decarbonization in the US road transportation sector. Also, this analysis underscores the urgency of hydrogen deployment in the sector by presenting a specific detailed strategy to decarbonize the US economy. The authors of the study agree with Hart (2020)’s belief about the necessity of rapid energy transition in the US, “The longer we resist the future, the more time is lost. Time is limited before we are technology followers in the next generation of clean energy power generation and transport technologies” (p. 20).

Finally, this closing section proposes a few future research directions about hydrogen deployment in the US road transportation sector. First, the researchers can build upon this study's ideas and incorporate rigorous transportation modeling tools to develop better projections and recommendations regarding the integration of hydrogen in the road transportation sector. Second, the analysts may devise a similar strategy that includes potential rebound effects when the prices for competing technologies and resources change due to hydrogen's influence on their market shares. Lastly, as hydrogen production/infrastructure-related technologies continue to improve and develop, future researchers may propose strategies for coordinating hydrogen-related decarbonization in the power and transportation sectors.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Energy Transition · Green Hydrogen

illuminem briefings

Hydrogen · Energy

Diego Balverde

Battery · Hydrogen

Interesting Engineering

Hydrogen · Aviation

Deutsche Welle

Green Hydrogen · Hydrogen

BioEnergy Times

Green Hydrogen · Hydrogen