BlackRock has moved rapidly on climate – but Adani exposures remain a major obstacle

· 6 min read

A glaring inconsistency in the US$10 trillion giant’s commitment to climate action

One success of the COP26 summit was the UN Global Finance Alliance growth to a US$130 trillion, almost double the total of just six months ago. Enforcement of the substance of this pledge comes next. And within that, BlackRock has moved massively on the issue of climate finance.

Just two years ago IEEFA wrote about the financial costs of climate inaction for BlackRock’s investors, with devastating wealth destruction at GE and Exxon clear examples of engagement with no time limits, transparency or consequences. Fast forward to 2021 and BlackRock repeatedly articulates both the imperative for climate finance action and the trillion-dollar investment opportunities emerging. And a Net Zero pledge is pending.

Self-interest is a powerful motive. There is nothing more compelling to a finance executive than a review of a decade-long pair trade – going long Tesla / short General Motors. Or long Nextera / short Exxon. Or long Adani Green Energy / short Adani Power (more on this below). Investing in fossil fuels is a wealth hazard, notwithstanding the massive fossil fuel inflation evident in 2021, an event that is likely to accelerate investment in low volatility, domestic, cheaper, zero emissions energy.

BlackRock has stepped up on engagement, public transparency, investor education, and investing in the zero emissions new industry opportunities, pushing for comparable global climate risk disclosures (TCFD, SBTi, SASB, IFRS) and even divesting (as a last resort for dinosaur industries in terminal decline i.e. coal).

The International Energy Agency (IEA) made a profound pivot in 2021, saying getting to net-zero emissions by 2050 means the world can’t afford any new oil, gas or coal developments. The global climate policy leadership of China, Japan and South Korea in the last 12 months has strengthened the EU’s sustained conviction, and this has been elevated by the return to the Paris Agreement of the U.S. in 2021 under President Biden, driving ambitious interim 2030 targets, reinforced by the China-U.S. Joint Declaration. The financial markets’ newfound understanding of climate risks may be evidenced by the EU emissions trading system (ETS) hitting a record high this week of €85/t, doubling in the last year, and up tenfold over five years.

BlackRock has been staunch in its insistence that divestment policies are a last resort. There are now 187 globally significant financial institutions with formal coal divestment policies, including BlackRock itself (but only for its active debt and equity funds, and only for thermal coal mining). Engagement and voting can be entirely ineffective for promotor dominated firms like Adani Enterprises.

In October, Bank of China’s coal exit abroad policy sounded the death-knell for new coal power, following the exits of Japan and Korea. And China’s historic support for coal-fired power projects in developing countries is now history with the greening of the Belt and Road Initiative.

The groundswell to align with the IEA policy and divest all fossil fuels is building, with leadership from the likes of the European Investment Bank, ABP of Netherlands, AXA of France and Zurich. And when the new ADB climate policy was watered down to leave its gas policy ambiguous (thanks to Japan), we saw a very telling U.S. vote abstention. And with the EU commitment to climate action undermined by gas industry lobbyists and wavering thanks to the Russian-EU gas crisis, it is great to see China stepping up as a global leader, driving for a credible green finance taxonomy.

While some in finance view divestment as a poor policy, to IEEFA this thinking ignores the growing global capital flight from fossil fuels, starting with thermal coal, but now spreading to coking coal, oil and gas. Wood Mackenzie now warns that the pool of climate-agnostic investors continues to shrink, elevating stranded asset risk. And the growing threat of $60bn of unfunded rehabilitation liabilities is significant enough to force even climate science denying governments to act to avoid taxpayers being left holding the can. With the growing tsunami of capital reallocation away from high emissions assets into zero emissions industries of the future, divestment is one tool to reduce growing stranded asset risks.

IEEFA sees the critically important role that the US$130 trillion UN-convened Glasgow Financial Alliance for Net Zero is playing, given its pledge to align with a 1.5°C world, and interim 2030 targets. Momentum is entirely one-directional.

Having established this critical global initiative, the next imperative is to lift the bar and cull the nonsense idea that global climate laggards like Vanguard or JP Morgan Chase can be included without any decisive change in practice. With the U.S. Treasury’s Financial Stability Oversight Council identifying climate as a key financial risk, this adds to the weight of the SEC actions to reduce investor deception from greenwash.

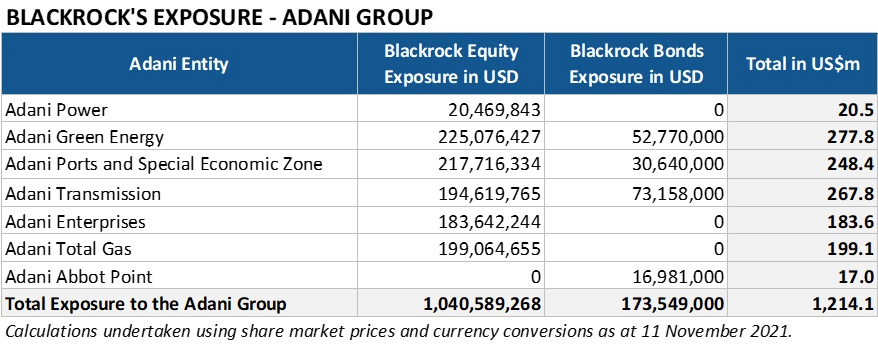

Returning to BlackRock: the bar has been raised, but some gaping inconsistencies remain. One of the starkest is the fact that BlackRock has an estimated cumulative exposure to the Adani Group of India of over US$1,200m (debt and equity). This conglomerate is possibly the largest single private developer of new coal globally, with 110Mtpa of new Indian coal mine capacity under development. And 9GW of new coal power plants, more LNG import terminals, a US$4bn imported coal-to-PVC proposal, and new gas reticulation systems.

Adani’s brand in Australia has been trashed with its unbankable Carmichael coal folly, which is due to commence exports close to a decade behind schedule, and despite repeated traditional owner objections. While the Adani Group is a leader in investing in zero emissions industries of the future in India, it has failed to give even a pretence of alignment with the IEA roadmap.

BlackRock argues that investing in one subsidiary is not the same as investing in another subsidiary. This is fallacious thinking for a family controlled conglomerate which has intercompany transfers as standard operating procedure. BlackRock must call out and divest global laggards at the group level, not just at a subsidiary level. Hiding behind the passive excuse is greenwash, and action on changing indexes is overdue.

Investing in Adani Ports is investing in the largest private coal and LNG import infrastructure provider in India, and related party transactions are an ongoing investor issue, whilst Adani Ports, along with Adani Enterprises, has regularly invested in the controversial and unbankable Carmichael mine-to-port project. As a result of this and other ESG issues, S&P Dow Jones removed Adani Ports from its ESG indices in April 2021 and MSCI will likewise drop Adani Ports over Carmichael controversies in November 2021.

IEEFA has long trumpeted the developing world leadership of India’s energy transition, and how strong government policy frameworks are driving an unstoppable momentum for decarbonisation. Solar costs are half that of imported coal-fired power generation. India provides a clear example for other developing countries can leverage global finance.

Moves by corporate leaders like Tata Power and Reliance Industries’ net zero by 2035 suggest a massive acceleration in Indian ambition. Adani’s corporate position is far worse than an each-way bet.

We would encourage BlackRock to use its full unprecedented fiduciary power to underpin and accelerate the advances achieved at COP26, including its massive index position. When a US$10 trillion giant moves decisively, the global investor pack will follow.

This article is also published on IEEFA. Energy Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Effects · Climate Change

illuminem briefings

Public Governance · Climate Change

illuminem briefings

Public Governance · Climate Change

The Economist

Nature · Environmental Sustainability

UNDP

Adaptation · Climate Change

Offshore Energy

Carbon Capture & Storage · Carbon