· 7 min read

The hype related to a hydrogen economy continues, relatively unabated. The fossil fuel industry, the natural gas utilities, Hyundai, and Toyota continue to push the illusion that hydrogen will be a source of heating, transportation fuel, and energy in general, despite the basics of physics and economics. Europe is especially susceptible to lobbying efforts at present it seems. They are, of course, going to be proven wrong unless their heavy thumbs on the scales of policy force us down that expensive dead end.

The basics of physics and economics have a way of winning arguments against lobbyists eventually, so the hydrogen problem will be eliminated.

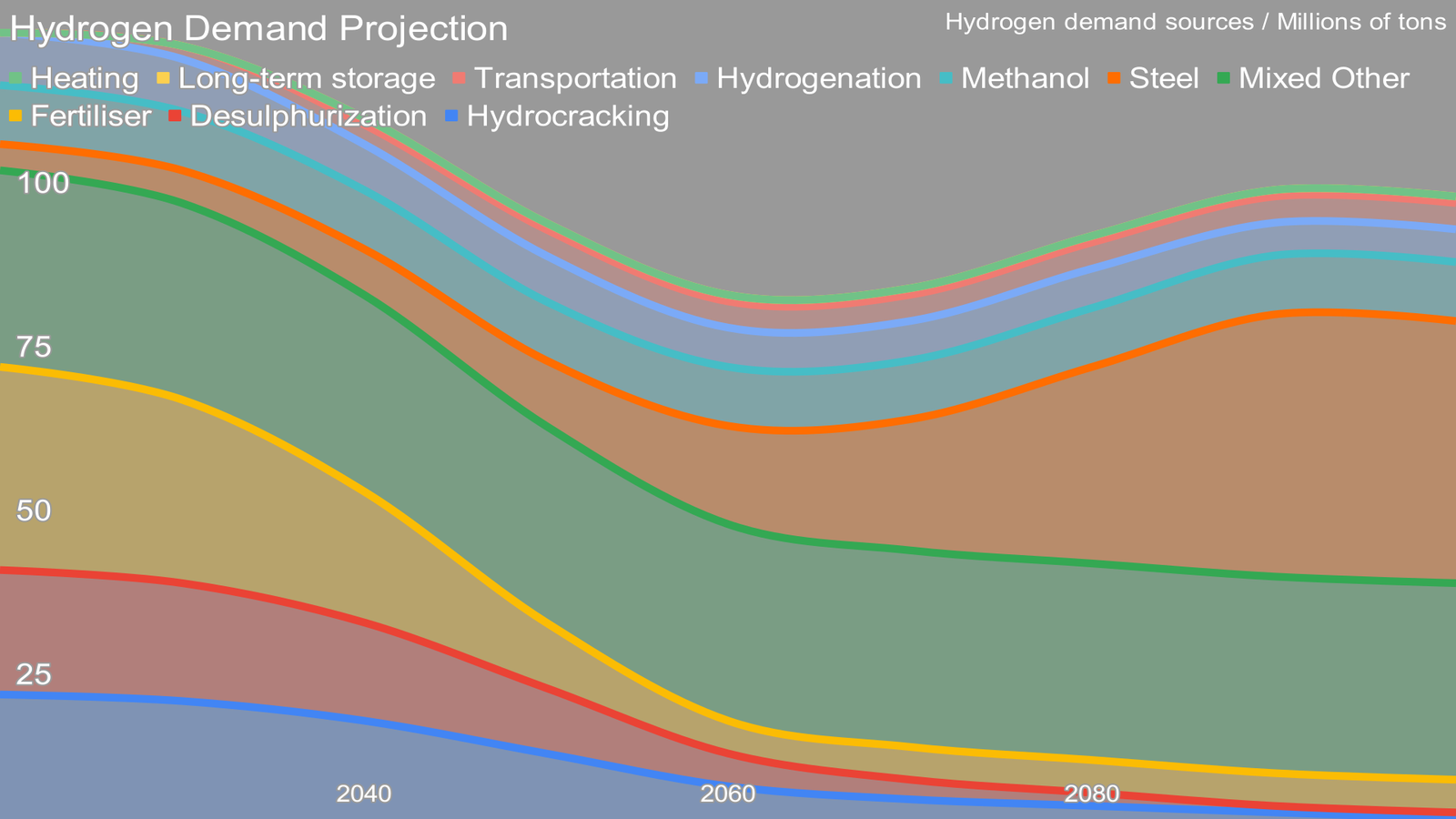

In mid-2021 I published my first version of a heterodox scenario of hydrogen demand through 2100 (part 1, part 2, part 3). It showed hydrogen demand falling before rising somewhat again. Pure hydrogen’s highest demand sectors are 55% in oil refineries for manufacturing engine fuels, and in 37% for fertilizer manufacturing, both of which have to diminish substantially through the middle of the century and beyond to meet climate goals. This is the third iteration of it.

The argument for fossil fuels being eliminated is obvious. I project perhaps 5% of refineries will be operating by 2100 to manufacture the valuable industrial chemicals which we currently get from the parts of a barrel of oil which don’t turn into fuel or asphalt, and which we have not found lower-negative externality biological replacements for. Hydrogen’s primary role in refineries is desulphurization and I project that only the lowest-sulphur crude that’s closest to water will still see demand in 2100, so hydrogen consumption will diminish in two different ways in this sector.

In the case of fertilizer, the hydrogen component of ammonia and fertilizers made from it currently comes from fossil fuels using steam reformation of natural gas with 10-11 times the mass of CO2e as hydrogen, or coal gasification with 20-35 times the mass of CO2e. When it is spread on fields much of it turns into nitrous oxides with global warming potentials 265 times that of CO2. The combination leads to nine or more times the mass of CO2e as fertilizer. Clearly this is a climate problem, and the solutions of low-tillage and precision agriculture, and nitrogen fixing plant and soil microbe enhancement through agrigenetics will cause a major fall in demand in this sector as agriculture decarbonizes and becomes a carbon sink again.

Only steel manufacturing is a significant growth area for hydrogen in this projection although a smaller one than most suppose. My projection has a significant increase in demand met through steel recycling in electric steel minimills, including a very large percentage of existing fossil fuel infrastructure and transport vehicles. After all, 40% of oceanic shipping alone is for coal, oil and gas, and that will go away. Similarly, natural gas pipelines, most refineries, oil trucks and the like will all become obsolete and available as scrap over the coming decades. Finally, cheap steel from overseas will become more expensive as marine shipping refuels with low-carbon alternatives, so more local scrap steel will be more economically advantageous.

There is no value proposition for heating with hydrogen outside of some very specific and likely niche industrial processes. In all cases, heating with electrically powered heat pumps and heat sources like electric arc furnaces powered by renewables will be less expensive, more convenient and safer than first making expensive hydrogen from renewable electricity. Hence the line for heating being flat at approaching zero tons through 2100.

Since the initial publication, I’ve fielded a wide variety of critiques of my assessment and had substantive discussions with experts such as Paul Martin of the newly formed Hydrogen Science Coalition, refineries experts and people engaged in biofuels. This is now the third version of the projection, and it’s fairly stable so far. Refinery use has hunted up and down a bit. Transportation has gone from no hydrogen demand to four million tons by 2100, but that’s specifically as a process enhancer for biofuels, not as a fuel in its own right, and definitely not as a synthetic fuel component.

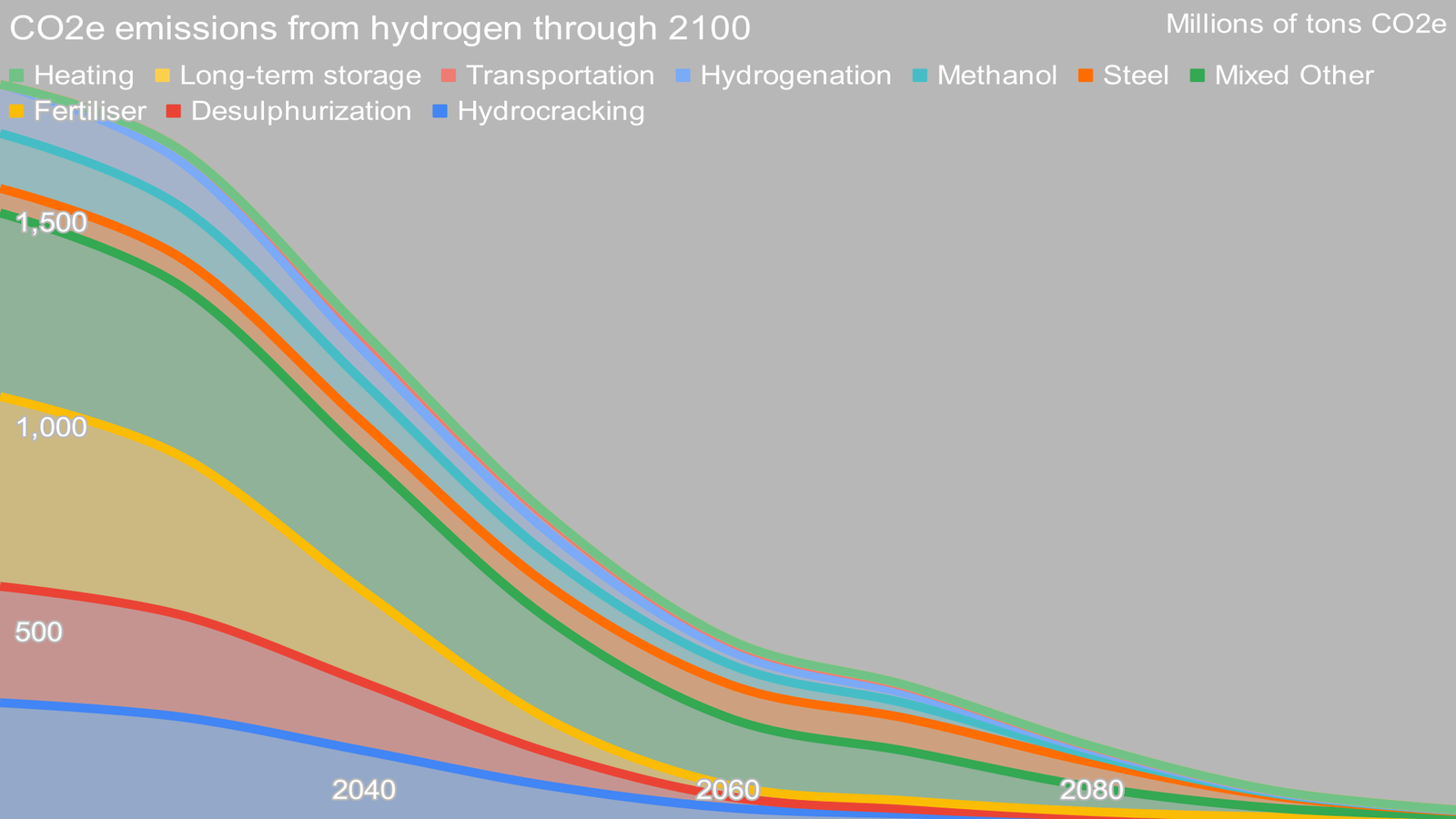

However, as with my projection of aviation refueling through 2100, the important question is What are the impacts on CO2e emissions? For the purposes of this assessment, I stayed solely with the scope 1 emissions associated with the manufacturing of hydrogen. Scope 2 and 3 emissions are critical, and in the case of both fossil fuels and fertilizers dwarf emissions from the hydrogen itself, but those are problems with different solutions.

At present, black and gray hydrogen from coal and natural gas account for over 99% of hydrogen manufacturing, with 20-35x and 8-10x as much CO2 as the mass of hydrogen resulting. It’s skewed to natural gas, so I chose an initial baseline of 15x, and trended that down to 4x through 2100, as whatever hydrogen comes from fossil fuels will be forced to deal with emissions for the most part. At the same time, fossil-fuel sourced hydrogen will drop in demand decade by decade until only minor hold-out regions still use it. Note that these numbers for scope 1 emissions from hydrogen manufacturing are by the author, and as such should be considered to include significant error bars, as with the projections of hydrogen demand through 2100.

Replacing it will be green hydrogen, currently under 1% of total supply, but growing to 99% of supply by 2100. Per work I did related to the Carbon Engineering direct air capture air-to-fuel boondoggle in 2018 and 2019, PEM electrolysis manufacturing of hydrogen would have a carbon debt of roughly 10x the mass of hydrogen created on grid electricity with 200 grams CO2e / kWh, a not unreasonable number for modern grids. That number will fall through 2100 as more and more renewables come on line, reaching 0.2x the mass of CO2e as hydrogen created. Hydrogen will become low-carbon, but it is only low-carbon from fully carbon-neutral electricity, and that’s not the global standard yet.

The combination of shrinking demand through 2060 as we electrify transportation and shift away from fertilizer, and decarbonization of hydrogen manufacturing as we shift to renewably powered electrolysis (and some faint hope ‘blue’ hydrogen production) will cause the massive emissions from hydrogen we currently experience to plummet.

To put this in context, just manufacturing hydrogen today creates around as much CO2e as all global aviation in 2019. That sector will decline substantially in emissions through 2100 as well, but it won’t be doing it with hydrogen-powered airplanes.

Hydrogen is a very significant contributor to global warming when only scope 1 emissions are considered. When the emissions from fossil fuels stripped of sulfur are considered, emissions skyrocket. When emissions from nitrous oxides baked off of fertilizer spread on fields globally are considered, emissions skyrocket.

This is why hydrogen is a climate problem, not a climate solution.

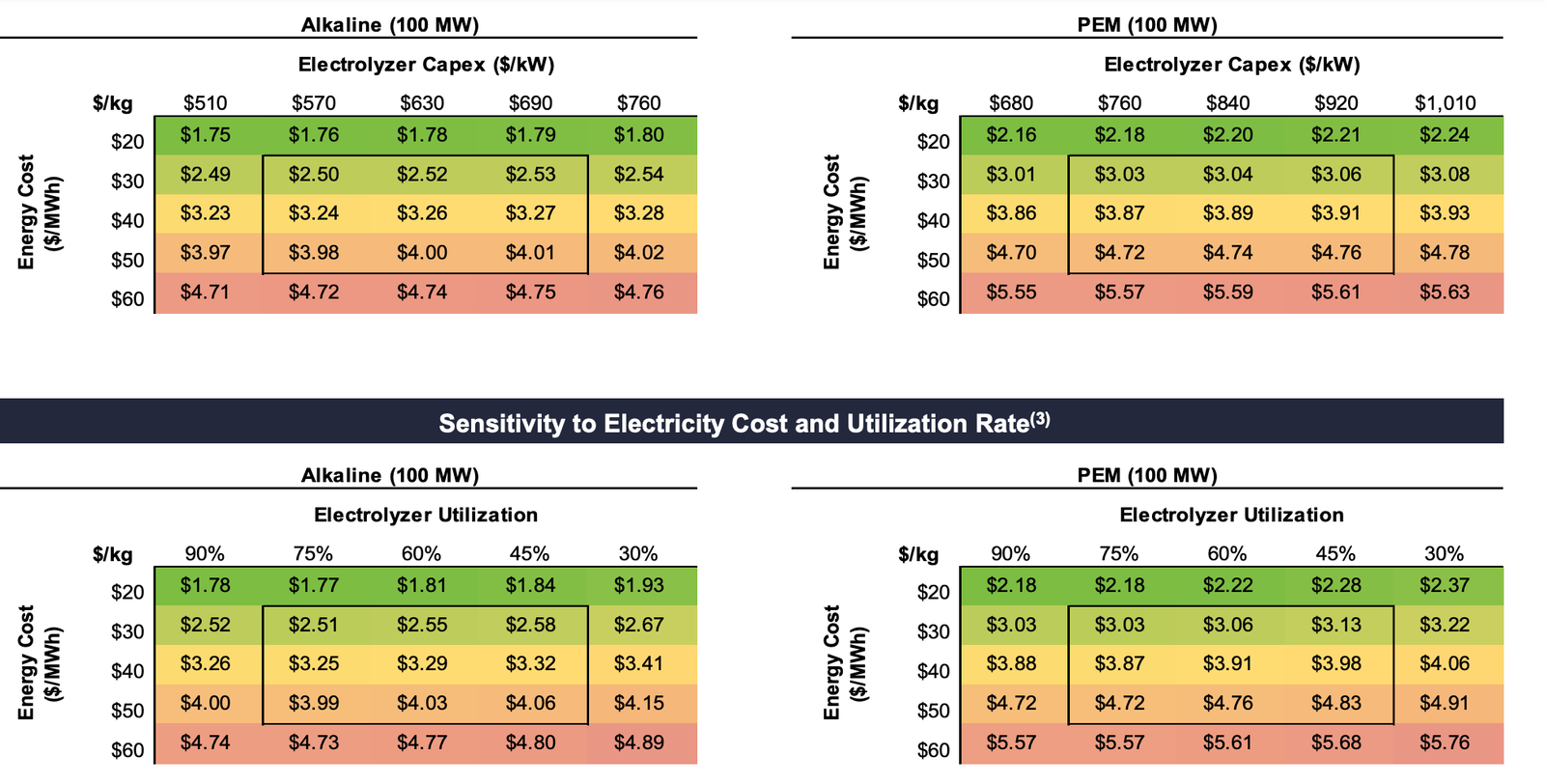

We can only decarbonize hydrogen manufacturing slowly. Manufacturing green hydrogen somewhat economically — but still more expensively than when we are allowed to treat the atmosphere as an open sewer — requires running cheap electrolyzers at very high capacity factors with very cheap electricity.

Electricity available 90% of the time from renewables isn’t going to drop below $20 / MWh. Electrolyzers aren’t going to become so cheap that we give them away in Cracker Jack boxes. Further, a hydrogen manufacturing plant has a significant number of additional components, most of which are standard and no longer subject to Wright’s Law efficiency improvements, so most of the plant components will be subject to normal inflation, not innovation-related deflation.

We aren’t going to be producing dirt cheap hydrogen from massive amounts of free renewable electricity 20% of the time. Green hydrogen will be significantly more expensive than gray hydrogen is today. Among other things, the transmission costs still have to be paid for. While McKinsey in one odd report projects that 2040 costs of hydrogen will be 15-20% of 2021 prices for fossil fuel-sourced black and gray hydrogen with no CCS, delivered and supercooled, that’s just a ludicrous assumption that ignores economics and physics. As a result, we’ll have an increasing ratio of green hydrogen displacing the problem area of black and gray hydrogen through 2100, and little new demand in areas with cheaper alternatives.

So there’s the bad news / good news story. Hydrogen is a problem today. It will be a problem for much of the century. However, by the end of the century, CO2e emissions related to hydrogen will be approaching zero. That projection rests on markets, industry, and policy makers eventually being rational about hydrogen of course, something which is in short supply today if you believe the press. But the basics of physics and economics have a way of winning arguments against lobbyists eventually, so the hydrogen problem will be eliminated, not expanded.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.