EU's carbon market: not yet fit-for-frontrunners

· 5 min read

Following Wednesday 14.07.21's Fit-for-55 package, here's Leon's initial analysis of the EU Emissions Trading System (EU ETS) revision proposal. Long story short: it becomes more difficult to pollute, but sustainable frontrunners are still disadvantaged compared to laggards.

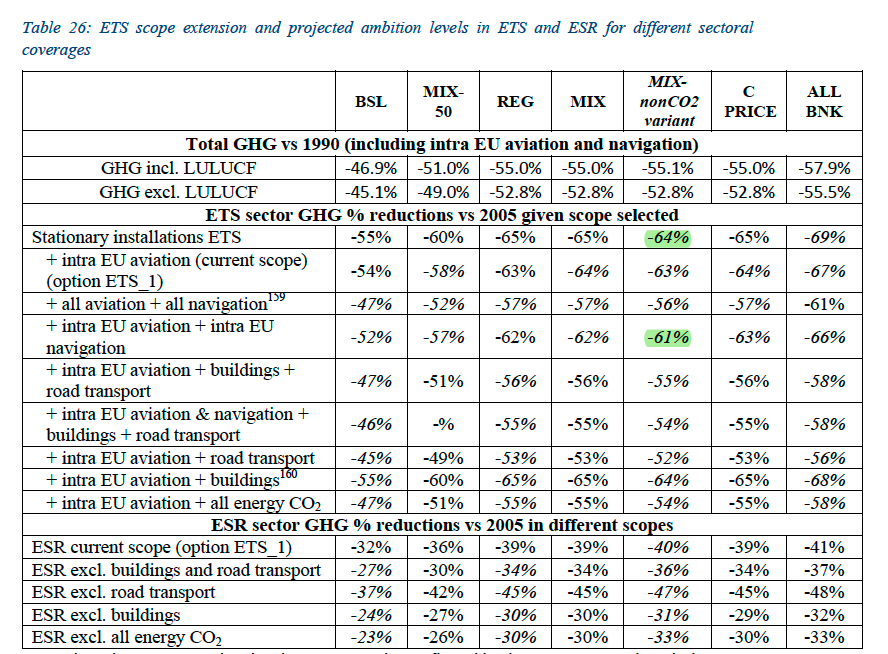

The emission reduction goal increased to -61% by 2030 compared to 2005, which covers the sectors of industry and power, but also intra-EU aviation and maritime.

As some who were around last year remember, this is taken from last year's 2030 Climate Target Plan (see table below). Unfortunately, this implies that the target for stationary installations (industry/ power) is only -64%, which means the EC picked a less ambitious scenario.

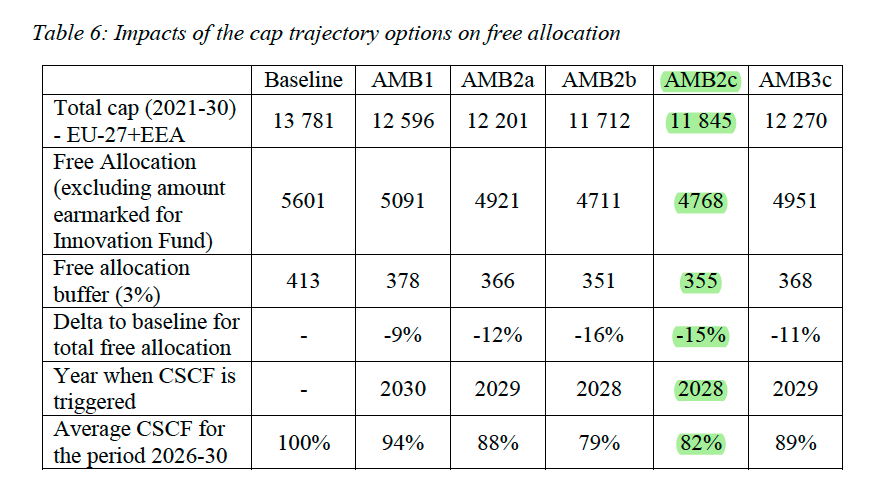

A big plus: the Linear Reduction Factor, which reduces the annual cap of all allowances in the system, almost doubled to 4.2% as of 2024, combined with a one-off reduction or "rebasing" of 119 mln allowances (scenario AMB2c in the picture). This leads to a big 15%-POINT cut in free allowances (FA). This LRF was a huge battle in the previous reform, so hope it stays.

An important miss: while everyone's commenting on the Commission's proposal to add road transport and buildings to the EU ETS, the major polluting sector missing is the municipal solid waste sector. As long as they are left out of the ETS, it improves the business case to burn municipal waste and does not incentivise investments in recycling/reusing infrastructure. This is a major problem.

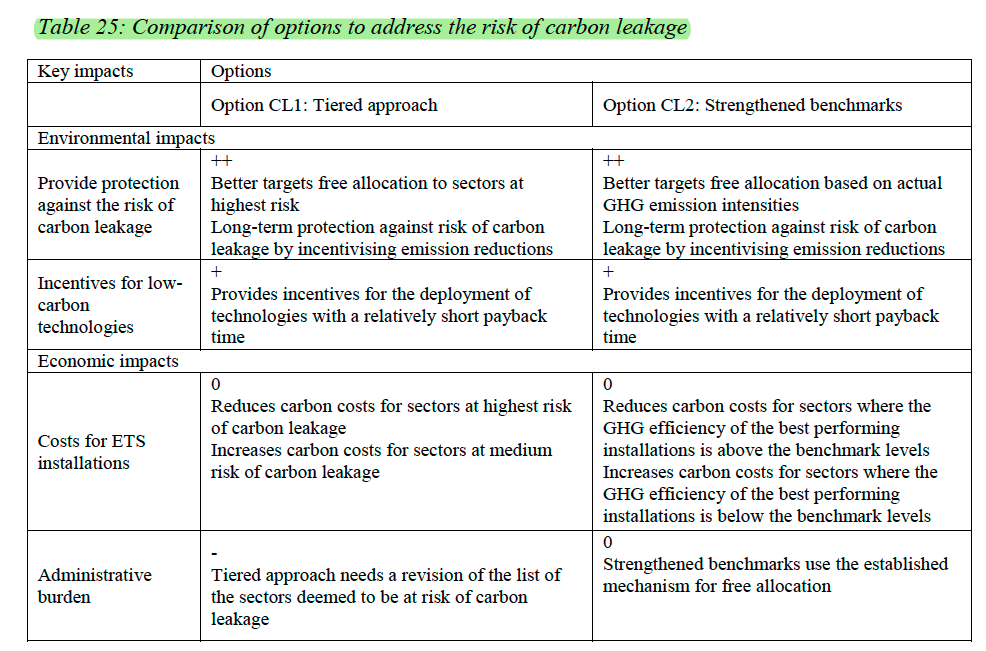

Another big miss: preventing the Cross Sectoral Correction Factor or CSCF, which would shave off FA for all EU ETS sub-sectors if applied. The famous tiered approach (option CL1, which creates different grades of carbon leakage risk and based on that caps the FA per sector) lost to the "strengthened benchmark" option (CL2 in the picture).

First of all, what are EU ETS product benchmarks? They and their main issue are described in the picture, which is taken from another op-ed article.

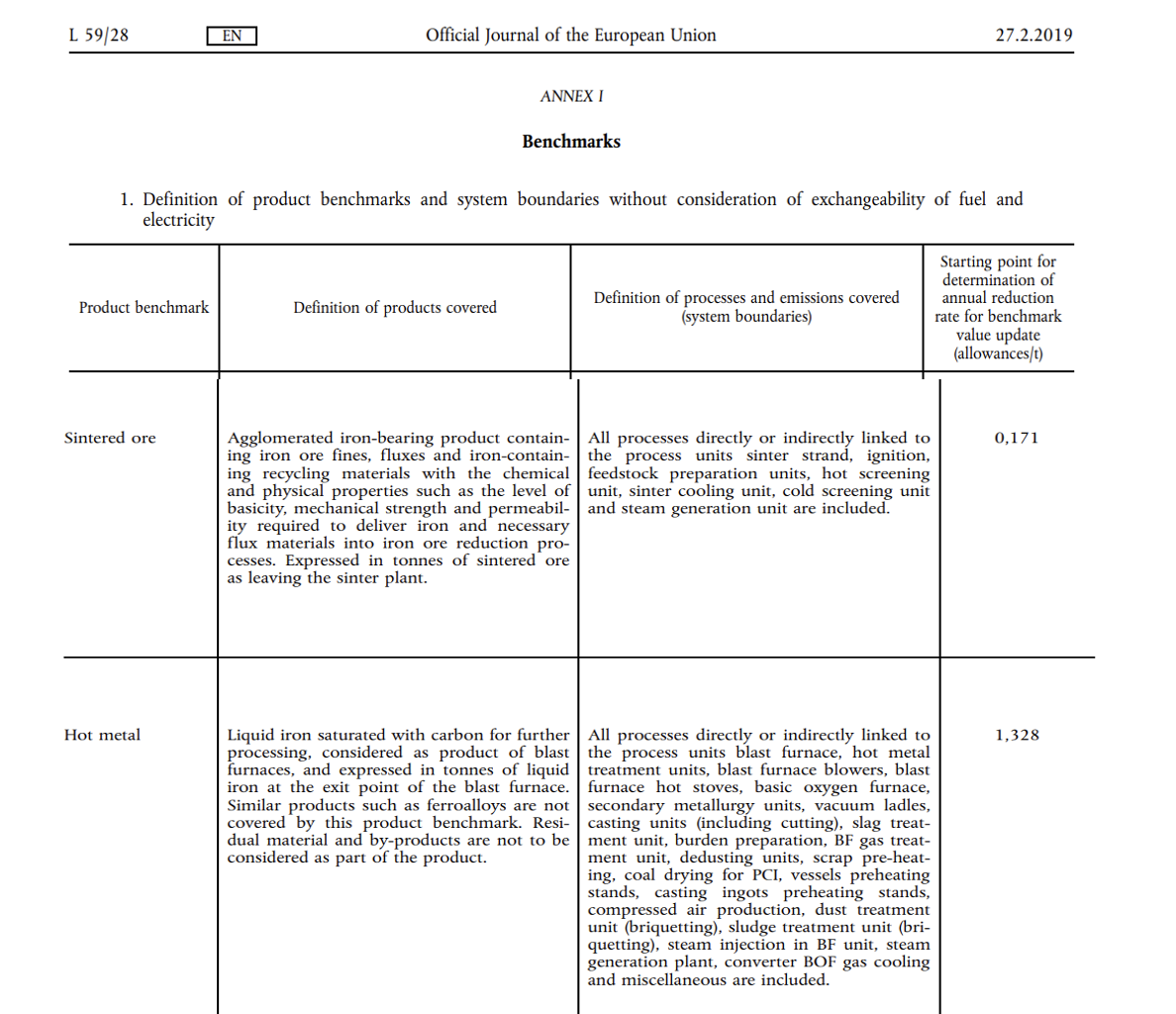

How could this have happened? Well, the way these free handouts are given out is based on a very technical process called “product benchmarks”. A whole value chain like that of steel is not put into a single benchmark, but instead each technique in the production process gets its own benchmark. For example, the key ingredient for iron to produce steel is iron ore. Therefore, most producers of iron ore are placed in the so-called Sintered Ore benchmark. Within this benchmark, each Sintered Ore producer competes to produce the “cleanest” sintered ore and this determines who receives the most free allowances. The big problem with this? Cleaner techniques to produce iron are excluded from this benchmark. For example, the Swedish iron ore group LKAB produces iron with a technique using iron ore pellets, which are basically little iron ore balls, whereas sintered ore are small iron ore rocks. Both can be used interchangeably to produce iron and eventually steel. The big catch? LKAB’s production of pellets emits only around one tenth of the greenhouse gases emitted by the average sintered ore installation. By a rough estimation, a large-scale transition from sintered ore to pellets production and use in the EU would – in itself – represent yearly climate gains of 16 million tonnes of CO2 emissions. This by comparison is almost equal to the annual CO2 emissions of Sweden’s entire industry. However, because it is a slightly different technique, the Commission and the EU steel lobby do not want it to be included in the sintered ore benchmark, and therefore LKAB is prevented from setting the standard for CO2 efficiency in its industry. Its dirtier competitors meanwhile are being kept alive with free handouts because they only have themselves to worry about. Sustainable frontrunners like LKAB are being heavily disadvantaged.

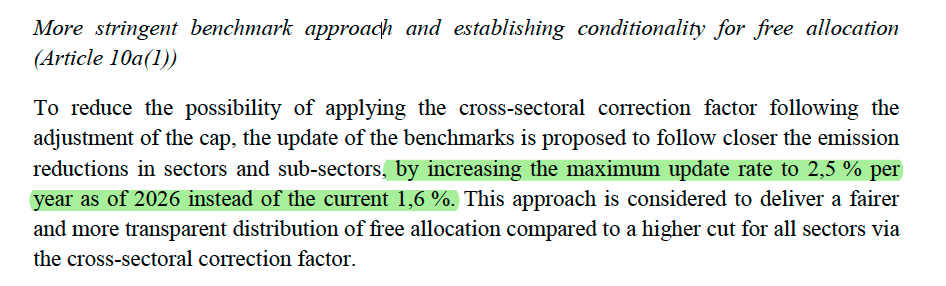

"Strengthened benchmarks" mean these benchmarks get a higher maximum annual improvement rate, from 1.6% to 2.5%.

Big sectors have lobbied the EC in the past to show their technological progress was very small, hence they will get a very low improvement rate.

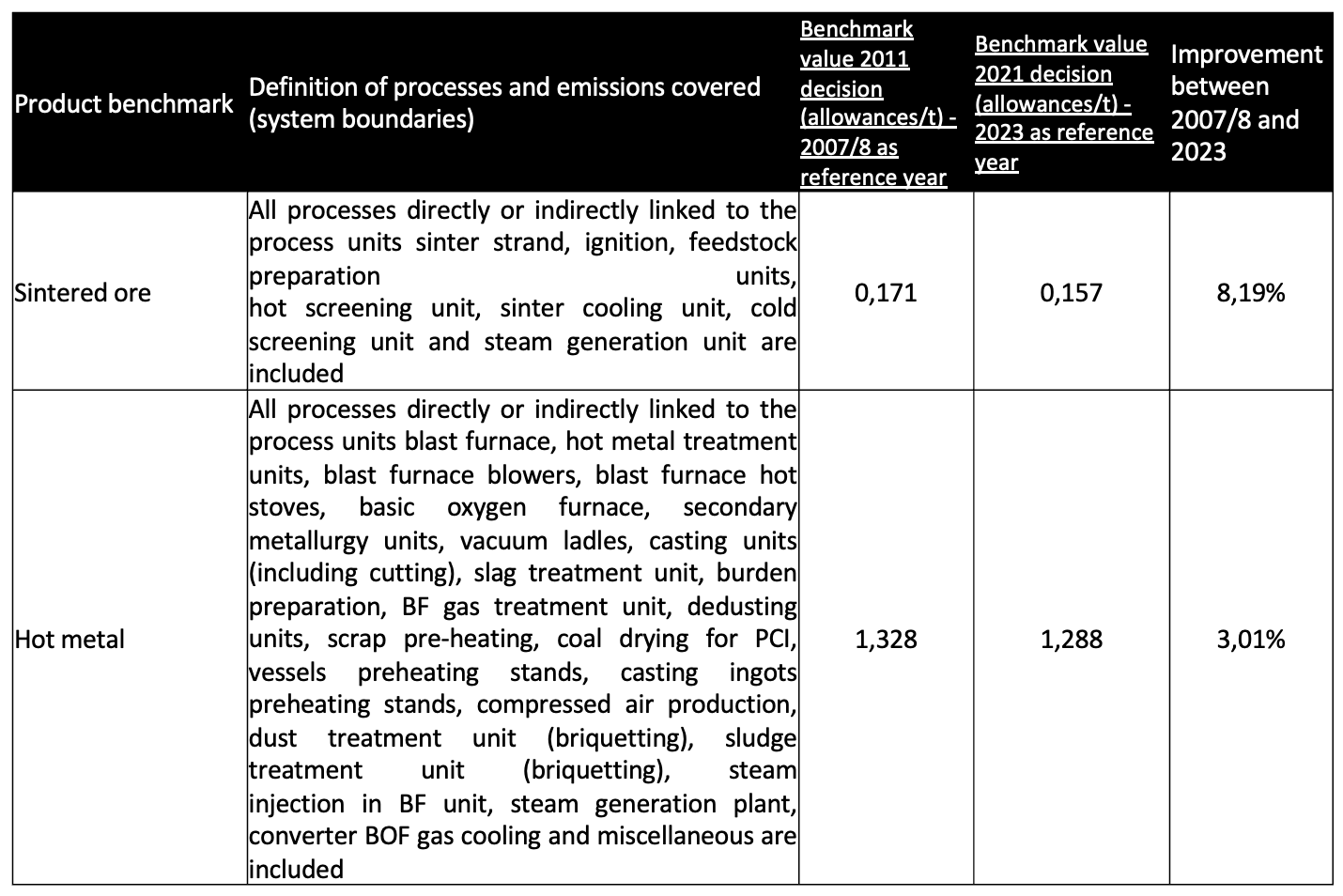

Comparing the benchmark values from Decision 2011/278/EU with the recently published updated benchmark value list for 2021-2025 you see that the Sintered ore benchmark will be “improved” from 0.171 t CO2/ton product in 2007/2008 to 0.157 by 2023 (8.2% improvement over a 15-year period!) and the Hot metals benchmark from 1,328 to 1,288 (3.0% improvement).

So, the fact that the maximum benchmark improvement is now set higher does not mean that polluting industries will actually be imposed that maximum improvement if you lobby hard enough.

Problematic: EU ETS benchmarks are the basis for how many FA are handed out. This is exactly the issue with the current product benchmark system. Old technologies are only competing with themselves for FA instead of with newer, cleaner solutions.

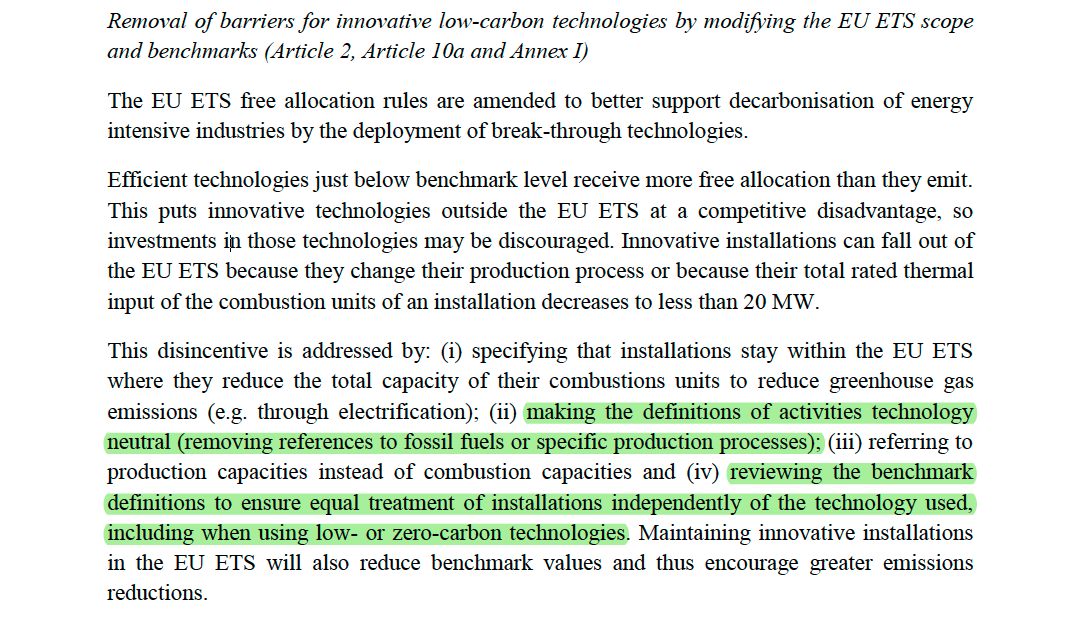

And this is where the EU ETS proposal brings some hope: it states that the EC wants to make the product benchmark system more technologically neutral and by ensuring equal treatment of installations independent of the technology or production process used. This sounds very promising, BUT:

It's not at all clear yet how the EC will translate its intentions to change the scope of the EU ETS product benchmarks into Annex I to Delegated Regulation (EU) 2019/331, which is where the benchmark descriptions are placed. The EC will have to probably do this through new delegated acts in the future.

The goal for the sustainable frontrunner lobby should be: it shouldn't matter how you produce something (e.g. steel), as long as it's done as cleanly as possible.

Therefore, benchmarks should move away from technology-specific EU ETS product benchmarks to value chain-wide product benchmarks that stimulate competition between different technologies on their CO2 reduction potential.

Only phasing out free allowances for CBAM sectors by 2035 is way too slow to enable a level-playing field with sustainable frontrunners, who hardly benefit from these things while their laggard competitors do.

So now what? It is now up to ambitious Members of the European Parliament (e.g. Pascal Canfin, Michael Bloss, Back Eickhout and Mohammed Chahim) and Member States in the Council to show more vision on the aforementioned concerns and make this EU ETS reform work for sustainable frontrunners.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

Glen Jordan

Sustainable Lifestyle · Sustainable Living

illuminem briefings

Architecture · Carbon Capture & Storage

illuminem briefings

Labor Rights · Climate Change

Financial Times

Carbon Market · Public Governance

GB News

Carbon · Sustainable Mobility

The Independent

Effects · Climate Change