A new perspective on decarbonising the global energy system

· 10 min read

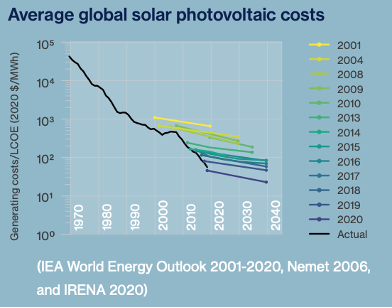

A rigorous analysis of the historical cost trends of energy technologies shows that the decades-long increase in the deployment of key renewable energy and storage technologies (e.g., solar, wind, batteries, and hydrogen) has gone hand-in-hand with consistent steep declines in their costs. For example, the cost of solar PV has declined by three orders of magnitude (more than 1000-fold decrease) as it has become more widely deployed over the last 50 years – declining so much that the International Energy Agency recently declared solar PV in certain regions “the cheapest source of electricity in history” (IEA, 2020). Such cost reductions are the consequence of experience gained in design, manufacture, finance, installation, and maintenance – and the overall pattern of development is hence known as the ‘experience curve’.

In contrast, non-renewable energy technologies have seen no significant deployment-related cost declines over the last 50 years. The cost of electricity from coal and gas has largely remained steady, fluctuating by less than an order of magnitude. The average cost of nuclear electricity has even increased over this same period, partly in response to safety concerns.

These long-term technology cost trends appear to be consistent and predictable (Farmer & Lafond, 2016; McNerney et al., 2011). Alongside advances in the technologies themselves, we have seen advances in our understanding of how technological change unfolds in the economy more broadly and of the characteristics that fast-progressing technologies have in common with each other (Wilson et al., 2020). Several new methods that are statistically validated and firmly grounded in data have been developed for forecasting technological progress (Nagy et al., 2013; Way et al., 2019).

Incorporating technology cost trends into a simple, transparent energy system model has produced new climate mitigation scenarios that starkly contrast to those currently produced for the IPCC and the International Energy Agency (IEA). It may come as a surprise that in most major climate mitigation models, such as the IPCC’s Integrated Assessment Models (IAMs), the costs of energy technologies are not handled very transparently. They assume unsubstantiated limits to cost declines and often contain out-of-date data (Jaxa-Rozen & Trutnevyte, 2021; Krey et al., 2019). We use an alternative approach to explore the implications of these discrepancies and have found an exciting new decarbonisation scenario we have named the Decisive Transition in recognition of the commitment to a clean energy system that this scenario represents. This scenario is created by selecting deployment rates for new energy technologies, based on their historical trends, and allowing such trends to continue for around a decade before tapering off. Technology costs are then simulated hundreds of thousands of times to generate probabilistic forecasts based on the methodology published by Farmer & Lafond (2016). These probabilistic cost forecasts are generated for the various key technologies to model a lower cost evolution of the energy system that has yet to be explored by the major mitigation models of the IPCC and IEA.

This new perspective suggests a reassessment is due regarding the potential cost and pace of the global energy system’s transition. At present, policymakers usually assume that the transition of the energy system to a Paris-compliant emissions pathway will be expensive; that it will require a net reduction in the provision of energy services or economic growth; and that it will rely critically on technologies that are currently expensive, unproven, or potentially controversial – such as carbon capture and storage (CCS), second-generation biofuels, and new nuclear energy designs (e.g., small modular reactors).

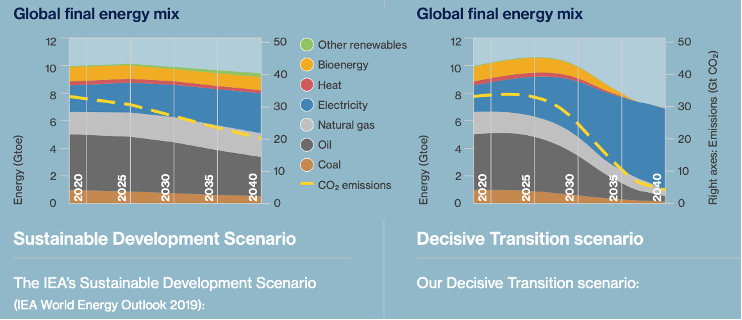

In this report, we present two contrasting scenarios that illustrate how properly accounting for technological cost trends can challenge common perceptions regarding the costs and benefits of a Decisive Transition to clean energy technologies. The modelling presented in this report contrasts two very different scenarios: a Stalled Transition, in which total demand for energy services continues to grow at its historical average of 2% per year, but with the ratios of the different energy technologies frozen at their current values. This scenario provides a useful ‘worst-case’ baseline and a counterfactual for estimating relative costs. The second scenario is a Decisive Transition in which current exponential growth rates in clean energy technologies continue for the next decade, then gradually relax back to the low systemwide rate. Here we see that within 25 years, fossil fuels are displaced from the energy sector, with all essential liquid fuel use replaced by “green” hydrogen-based fuels. Solar and wind provide most of the energy; transport and heat are mostly electrified; and reliable electricity is maintained using batteries and chemical-based energy storage technologies. To provide a like-for-like comparison with the Stalled Transition, useful energy also grows at 2% per year, a rate much higher than in other deep decarbonisation scenarios.

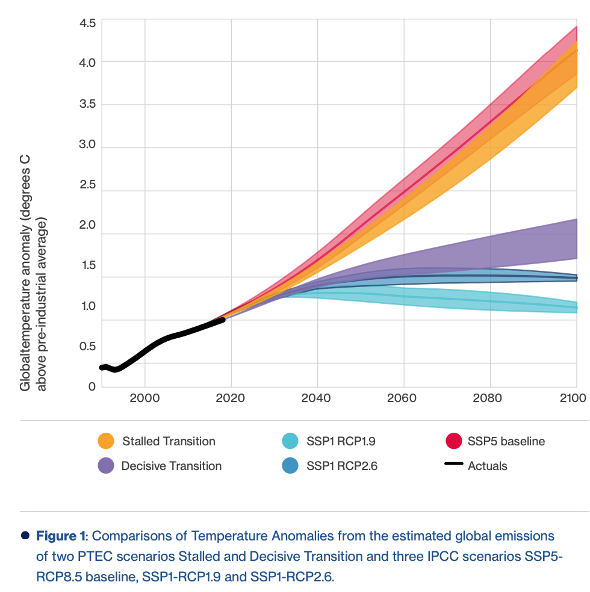

Our Decisive Transition achieves almost all the reductions in greenhouse gas emissions necessary to match the most ambitious IPCC scenarios. Figure 1 presents the global warming associated with the Stalled (orange) and Decisive Transition (purple) scenarios compared to three key IPCC warming scenarios. Our Stalled Transition scenario is most closely aligned with what is regarded as the ‘worst-case’ IPCC scenario (SSP5 RCP8.5). The Decisive Transition is most comparable to the SSP1 RCP2.6 high mitigation ambition “Taking the Green Road” scenario. This is a remarkable outcome because, in contrast to the high ambition IPPC scenarios (SSP1 RCP1.9 and SSP1 RCP2.6), the Decisive Transition scenario achieves this result without reducing non-energy-based emissions; without any significant deployment of nuclear, carbon capture and storage, or energy-saving technologies; and without requiring a reduction in energy demand or economic growth. It is merely a result of extending the current high growth rates in deployment of clean energy technologies for another decade.

The Decisive Transition is significantly cheaper than the Stalled Transition. The modelling show-cased in this report suggests that a clean energy system could be trillions of dollars less expensive to engineer than continuing with the current system based on fossil fuels (Way et al., 2020). This is even without factoring in pollution and associated morbidity and mortality (Vohra et al., 2021), or the multitude of additional physical climate costs likely to result from higher levels of global warming (Arnell et al., 2019).

In the short- and medium-term, situations may arise where renewables cannot cheaply meet the energy demands of certain regions. In these situations, arguments might be made for investment in interim fossil-fuel-based solutions, such as natural gas. However, it should be kept in mind that such investments may not contribute to the final transition and can instead lead to carbon lock-in and create additional transition risk. Foreign aid should be aligned to enable developing states to instead “leapfrog” to electrification and new clean electricity generation, load balancing, and storage technologies.

Unlike most other ambitious scenarios, the Decisive Transition scenario does not rely on underdeveloped technologies, such as carbon capture and storage (CCS) and Bioenergy with CCS (BECCS). This raises questions about whether we should continue channelling investment towards technologies like CCS and nuclear fusion for energy provision. Neither may mix particularly well with renewables and will detract investment away from driving down costs in renewables and storage technologies.

It is still vital that we counter institutional and social barriers to a Decisive Transition, that financial stability is maintained, that gender and social equality is maintained or improved, and that job losses in the fossil fuel industries are addressed. The IEA has shown the potential for renewables to provide far more jobs than other energy-related investments (IEA, 2020), but these jobs may not be created in the areas where coal mines are being closed. Industrial strategies will therefore need to be developed to counter such transition risks. Efforts to maintain or improve gender and social equality should be prioritised now to avoid perpetuating existing gender inequalities (Pearl-Martinez & Stephens, 2016). Social equity concerns also go well beyond the implications for coal miners and include communities tied to coal-fired power stations and communities linked to oil extraction and refinement (Carley & Konisky, 2020). Countries with high reliance on coal-fired energy will also require international support in establishing grid balancing, storage, and efficient power markets to enable higher renewable penetration.

Transition risks are real and likely, given how rapidly technological trends are moving, but it must be remembered that, unlike physical climate risks, stranded assets are only a one-off cost. If we do not end climate change, the more frequent and damaging extreme hurricanes, floods, droughts, and wildfires are likely to cause far greater economic costs that will be constant, long-term, and potentially permanent. Our estimates show the costs of climate damages up to the end of the century from a Stalled Transition are at least ten times greater than any transition risk associated with the Decisive Transition.

In summary, the Decisive Transition scenario indicates that the decarbonisation of the global energy system:

This new perspective also suggests that renewable technologies like solar and wind can provide a steady and secure energy supply, rebutting common beliefs regarding the intermittency problems with renewables. There is a belief that the large-scale deployment of renewables in the global energy system will lead to energy supply failures and high grid integration costs in the future. Our model challenges these perceptions by coupling solar and wind deployment with the deployment of sufficient short-term storage (e.g., batteries) and long-term storage (e.g., hydrogen and ammonia) technologies to ensure high levels of energy security. This feature allows these storage technologies to also “ride” down experience curves of their own, reaching far higher deployment levels than are commonly anticipated. In doing so, the model demonstrates that it is economically feasible to create a carbon-neutral energy system which:

This research offers the opportunity to revisit thinking around the most financially effective speed to transition to a Paris-compliant world. We have found strong evidence to suggest renewable and energy storage technologies will continue their current decreasing cost trends. Most, if not all, of the major climate mitigation models informing decision makers, have continually underestimated these trends. For instance, most major climate mitigation models have minimal electric vehicle take-up in the next few decades. However, if electric vehicle costs continue on current trends, they could be cheaper to buy and run than internal combustion vehicles in less than a decade (Sharpe & Lenton, 2021). Somewhat counter-intuitively, this increased electricity demand from electric vehicles might actually drive down electricity costs (Lafond et al., 2020). This is due to the positive feedback dynamics that our model is designed to capture and that standard economic models do not. Increased adoption of electric vehicles will lead to more demand for electricity. If this increased demand is met with the deployment of more renewables, renewables will get cheaper, electricity generation will get cheaper, electric vehicles will become cheaper and more desirable... and the feedback repeats – provided that this new electricity demand is met with more deployment of renewables.

This research can act as a catalyst for governments to reassess their NDCs at COP26. This is especially true for nations looking to enact a “green recovery” programme or expects significant future energy demand growth and, therefore, are already considering new investment in energy infrastructure (Hepburn et al., 2020). We need a better understanding among national policymakers on what drives these renewable cost reduction trends and how a Paris-style collaboration on investment in renewables and storage for national targets could benefit all countries. COP26 offers a ripe opportunity for a Glasgow Accord on action. Renewables are clear “runners” in the technology race, and early investment will allow countries to capture more of the prosperity this green industrial revolution offers (Farmer et al., 2019).

After the turmoil and horrible cost of the Covid-19 pandemic, we cannot afford business-as-usual – it is too risky and too expensive. When coupled with storage, expanded transmission networks, and smart grids, renewable energy potentially provides a solution to the energy trilemma that a fossil fuel-based system simply cannot replicate – an energy system that is affordable, secure, and sustainable.

This article is a summary of the "A new perspective on decarbonising the global energy system" report of the Smith School of Enterprise and the Environment, the University of Oxford, co-authored by Matthew Ives, Luca Righetti, Johanna Schiele, Kris De Meyer, Lucy Hubble-Rose, Fei Teng, Lucas Kruitwagen, Leah Tillmann-Morris, Tianpeng Wang, Rupert Way & Cameron Hepburn

To read the full report please click here.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Carbon Market · Carbon

illuminem briefings

Climate Change · Effects

illuminem briefings

Effects · Climate Change

Time News

Climate Change · Adaptation

GB News

Net Zero · Public Governance

The Guardian

Pollution · Carbon