The sweet spots of low-carbon hydrogen

· 6 min read

Low-carbon hydrogen is emerging as a key player in the drive toward a sustainable energy future. Critical industries such as fertilizer production, chemicals/refineries, steel, and cement manufacturing are finding low-carbon hydrogen to be economically, energetically, and technically feasible, offering substantial benefits over other hydrogen use cases like transport, heating, and natural gas substitution in pipelines.

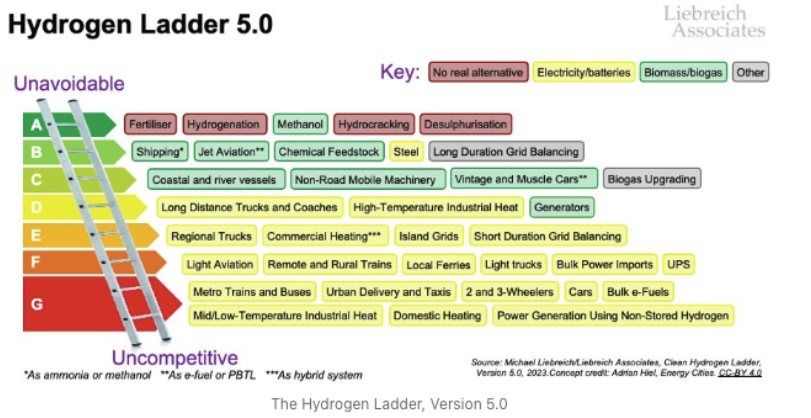

The global transition to a low-carbon economy has brought hydrogen into the spotlight as a versatile and clean energy carrier. However, we are now a little further in time and as with all new technologies we can now see much clearly where and how it makes sense to apply low carbon hydrogen. Many and diverse applications have been proposed and researched with a lot of attention generated. Sometimes it seems that Hydrogen is a solution for a lot of decarbonization pathways but that is not the case. This is being summarized beautifully by Michael Liebreich in his Hydrogen ladder which currently has its fifth version. So any policies and subsidies to stimulate hydrogen economy development should be aimed at the unavoidable and sweet spots that do exist, in particular the potential to decarbonize hard-to-abate sectors like heavy industry. Recent projects highlight the sweet spots where low-carbon hydrogen not only makes sense but thrives economically, energetically, and technically.

A prime example is Lithuania's largest fertilizer producer, Achema, which secured a €122 million government grant to transition from grey hydrogen to green hydrogen. This shift will significantly reduce carbon emissions by leveraging renewable energy for hydrogen production via electrolysis. This initiative exemplifies the synergy between government support, renewable energy availability, and industrial application, making it a prime sweet spot for low-carbon hydrogen. This goes for all other users of grey hydrogen as well in the rest of Europe and beyond.

The economic landscape for low-carbon hydrogen is rapidly evolving. As the cost of renewable energy continues to decline, green hydrogen production becomes increasingly competitive. However, not everywhere and we should always prioritize the direct use of this increasingly cheap and abundant renewable energy. Government incentives, such as the EU's funding for green hydrogen projects and subsidies under the Inflation Reduction Act in the US, further enhance its economic appeal. These incentives reduce financial barriers, making large-scale hydrogen projects economically feasible for target industries like fertilizers, chemicals, steel, and cement.

Energetic efficiency is crucial for the viability of hydrogen projects. Technologies like proton exchange membrane (PEM) electrolysis and alkaline electrolysis have made significant strides in improving the efficiency of hydrogen production. Industrial sectors with high energy demands, such as steel and cement manufacturing, can harness these technologies to reduce emissions while maintaining productivity. The integration of hydrogen storage solutions also helps balance supply and demand, ensuring stable energy output.

But again, here it is important to note that alternatives do exist that use renewable energy and electricity directly like for instance arc lighting steel production. The advance of battery technologies is also a factor to consider which may reduce the application and business case further for hydrogen production and storage. As you inevitably lose 30-60% of energy producing and converting hydrogen, which is avoided for the most part when using renewable energy directly in combination with battery storage.

Advancements in hydrogen production, storage, and distribution technologies are pivotal. Innovative solutions, such as solid oxide electrolysis cells (SOEC) and advancements in hydrogen fuel cells, are enhancing the technical feasibility of low-carbon hydrogen. These technologies are being integrated into various industrial processes, demonstrating their versatility and reliability.

So where are these Hydrogen sweet spots? Industries such as fertilizers, chemicals/refineries, steel, and cement are ideal candidates for low-carbon hydrogen for several reasons:

High Carbon Intensity: These industries are among the most carbon-intensive, making them prime targets for decarbonization. Low-carbon hydrogen can replace fossil-based hydrogen (grey hydrogen) used in chemical processes, significantly reducing emissions.

Continuous Operations: Unlike transport and heating, which have variable demand, industrial processes often run continuously, ensuring a steady demand for hydrogen. This consistency improves the economic feasibility of hydrogen projects.

Existing Infrastructure: Many industrial sites already use hydrogen in their processes, meaning the transition to green or blue hydrogen requires less infrastructure overhaul compared to sectors like heating or transportation.

High Temperature Requirements: Industries like steel and cement require high-temperature processes that are challenging to electrify. Hydrogen provides a clean alternative that can achieve the necessary temperatures without carbon emissions.

While low-carbon hydrogen has potential in transport, heating, and natural gas substitution in pipelines, these applications face much greater challenges in terms of efficiency, economic viability and technical application:

Transport: The infrastructure for hydrogen refueling stations is limited, and battery electric vehicles (BEVs) currently offer a more mature and cost-effective solution for most passenger and light-duty vehicles.

Heating: Hydrogen's low energy density compared to natural gas makes it less efficient for heating applications. Electrification and heat pumps provide more efficient and scalable solutions.

Natural Gas Substitution: Blending hydrogen into natural gas pipelines poses technical challenges, such as material compatibility and energy content adjustments, making it less straightforward than direct industrial applications.

Long range transport: not to be confused with the direct use of hydrogen and derivatives as fuel for transportation. I mean here the transportation of Hydrogen in it’s gaseous or liquid form, or as ammonia. It is envisioned that much hydrogen will be produced outside the EU and transported here to be used in the industry. However, the gap between green hydrogen produced and transported (upto 1500 euro per ton) and the current price point (around 350 euro per ton) makes it very hard to compete. Even taking into account a very low renewable energy price it will still be very difficult to bring this price down as much of the economics are in the installations and technologies, not the electricity price.

The transition to low-carbon hydrogen is becoming a reality and has undergone a reality check. Many applications have been explored and have been see as perhaps not the most efficient and economic. However important applications do exist in particularly in carbon-intensive industries like fertilizer production, chemicals/refineries, steel, and cement. These sectors offer sweet spots where low-carbon hydrogen is economically viable, energetically efficient, and technically feasible. Projects in Lithuania and other global examples highlight the momentum towards a sustainable hydrogen future. By focusing on these key industries, both in terms of policy and subsidies, we can make significant strides toward decarbonization and a sustainable energy landscape.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

Arvea Marieni

Climate Change · Carbon Market

Jeremy Bentham

Energy · Climate Change

Filip Koprčina

Energy Transition · Sustainable Investment

Forbes

Renewables · Nature

Financial Times

Oil & Gas · Energy

The Guardian

Net Zero · Oil & Gas