The hydrogen dilemma in Italy’s energy transition

· 6 min read

The role of molecular hydrogen (H2) as an energy vector has been advocated for decades, but its use has never materialised due to technical and economic hurdles[1]. Under calls for a reshaping of energy production, hydrogen is undergoing a revival.

Upon the release of the Hydrogen Strategy by the European Commission (EC) in 2020, the sustainable production of H2 has become an investment priority within the Next Generation Europe plan. Accordingly, Italy recently set a National Plan for Recovery and Resilience (PNRR), in which €3.2 billion is allocated for the research, testing, production and use of H2.

The Italian government is giving hydrogen a central role in its plans for an ecologic transition, and has set ambitious targets for the development and application of this energy vector by 2030. However, we worry that these plans are too optimistic, and that they may subtract resources from other technologies that currently have a better potential to reduce CO2 emission. Instead, we need to take a realistic look at the possible role of hydrogen in the Italian economy by 2030, and we believe that similar considerations may be applied to other industrialised countries.

Molecular hydrogen is currently produced at a massive scale, and used primarily for the synthesis of ammonia needed for fertilisers, in oil refinery processes and for the synthesis of methanol. It is derived from natural gas, and the energy needed to make it comes from fossil fuels. This hydrogen is called grey or brown. Researchers, companies and governments are now focusing on the only option leading to zero CO2 emissions, namely green hydrogen. In this case the feedstock is freshwater, which is split into hydrogen and oxygen by means of electrolysers powered by renewable electricity. At present, the price of green hydrogen is at least three times higher than its grey counterpart, and the electrolyser technology is not sufficiently developed to produce millions of tonnes of H2 annually.

Green hydrogen is projected to become market-competitive in about a decade, but even under this scenario, it is important to assess how much electricity, land and water it will require. Here we focus on Italy and, for the sake of simplicity, we assume that the energy to produce green hydrogen will only come from photovoltaics (PV), the predominant renewable technology.

The most rational step towards a sustainable hydrogen economy would be the greening of grey hydrogen currently produced in petrochemical plants. In Italy this amounts to 480 kton/y.

Another often mentioned target would be the greening of the steel industry (the prototypical hard-to-abate sector). In Italy, the only blast furnace steel factory where hydrogen could replace coal is in Taranto, with a capacity of about 6 Mton/y. Producing 1 ton of green steel requires 50 kg of H2, which would translate into a demand of about 300 kton/y of green hydrogen.

Next would come the hydrogen for the energy sector (e.g., transport, heating). The Italian government targets a penetration in final energy uses of 2% by 2030 (and up to 20% by 2050). Based on national statistical energy data, this corresponds to further 850 kton/y of green hydrogen.

Let us sum up. In order to enable just the three above-mentioned uses, which are among those envisioned by the government strategy on hydrogen, 1.6 Mton/y of green hydrogen are needed. This (see the ‘methodological note’) requires 85 TWh/y of electricity, corresponding to about 30% of the Italian production in 2019. Generating it exclusively from PV would mean the installation of 75 GW (and over 10 GW of electrolyser capacity), along with an adequate storage capacity which would require a dedicated assessment.

The surface requirement of 600-750 km2 (almost twice the surface of the Garda Lake) would not be a problem. It corresponds to less than 1% of unused or abandoned land in Italy. Freshwater consumption would not be a limiting factor either. The nearly 30 million cubic meters needed would correspond to 0.4% of total industrial water use in Italy.

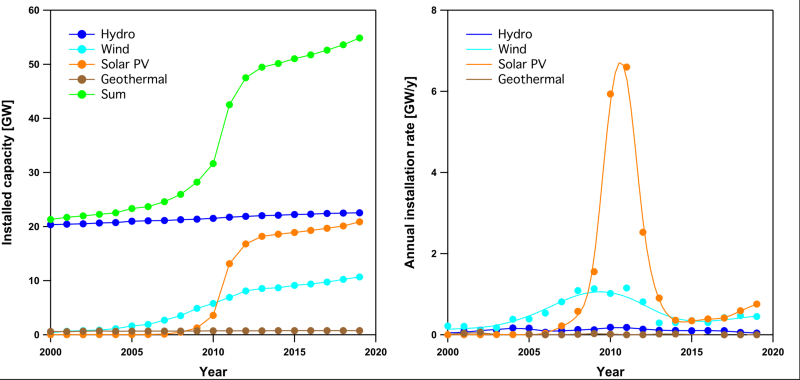

The real issue is the rate of renewable electricity deployment. In the decade 2006-2016, almost 20 GW of PV have been installed in Italy, with a record of about 7 GW in 2011 (Figure 1). Thus, the addition of 75 extra GW in less than 10 years is a huge feat that requires strong political commitment. Moreover, the three above uses of hydrogen for Italy would require almost 11 GW of electrolyzer capacity by 2030. Considering that 40 GW is the target for the whole EU in 2030, this appears to be very optimistic.

Meanwhile, irrespective of any plans for green hydrogen, a substantial increase of renewable electricity production is needed to decarbonise the Italian electricity system, now strongly based on natural gas. The current share of renewable electricity production in Italy (about 40%, 120 TWh/y) must be increased to around 70% (i.e., over 200 TWh/y) by 2030 to reach the EU targets. Interestingly, this means generating at least 80 TWh/y of green electricity, i.e., an amount comparable to what assessed for the three green hydrogen targets discussed above. The overall sum, 165 TWh/y, is over 50% of the current national electricity consumption and it is unrealistic to produce ex-novo such a huge output in less than a decade.

Hydrogen, in other words, poses a dilemma for the future of the energy system, in Italy and in other countries. Until we have large surpluses of renewable electricity, which will hardly happen before 2030, using electricity to make hydrogen and then use it for powering cars or heating buildings is in stark contrast with the target of increasing the energy efficiency of EU by 32.5% within 2030. More mature and efficient direct electric technologies are available, such as battery vehicles and heat pumps.

While research on hydrogen and deployment of renewables must continue, time has come – not only for Italy but for the whole European Union – for political decisions on priorities for the next decade, and a clear choice must be made between betting on direct electrification or on hydrogen production[2].

The calculations presented in the article are based on the following assumptions, derived from the literature:

The energy consumption of large size electrolyzers is between 55 and 60 kWh per kg of hydrogen produced;

Modern Proton Exchange Membrane (PEM) and Alkalyne (AEL) electrolyzers have an average hydrogen production of about 150 ton/y per MW of stack power installed;

Photovoltaic (PV) panels cover 8-10 m2 per installed kW;

PV facilities in Italy operate at full capacity at 13% of time across the year due to intrinsic production fluctuation;

It takes 9 litres of freshwater to produce 1 kg of hydrogen, twice as much if water demineralization and heat management are considered

This article is also published on Nature. Energy Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Energy Transition · Green Hydrogen

illuminem briefings

Hydrogen · Energy

Diego Balverde

Battery · Hydrogen

Interesting Engineering

Hydrogen · Aviation

Deutsche Welle

Green Hydrogen · Hydrogen

BioEnergy Times

Green Hydrogen · Hydrogen