Russia-Ukraine conflict adds impetus to Asia’s energy transition

· 5 min read

Russia’s invasion of Ukraine spells further turmoil for global energy markets already reeling from extreme price volatility over the past two years. Oil prices have now surpassed US$100 per barrel for the first time since 2014, while other commodities like liquefied natural gas (LNG)—which has recently seen record low prices followed by record highs—are set to experience continued volatility.

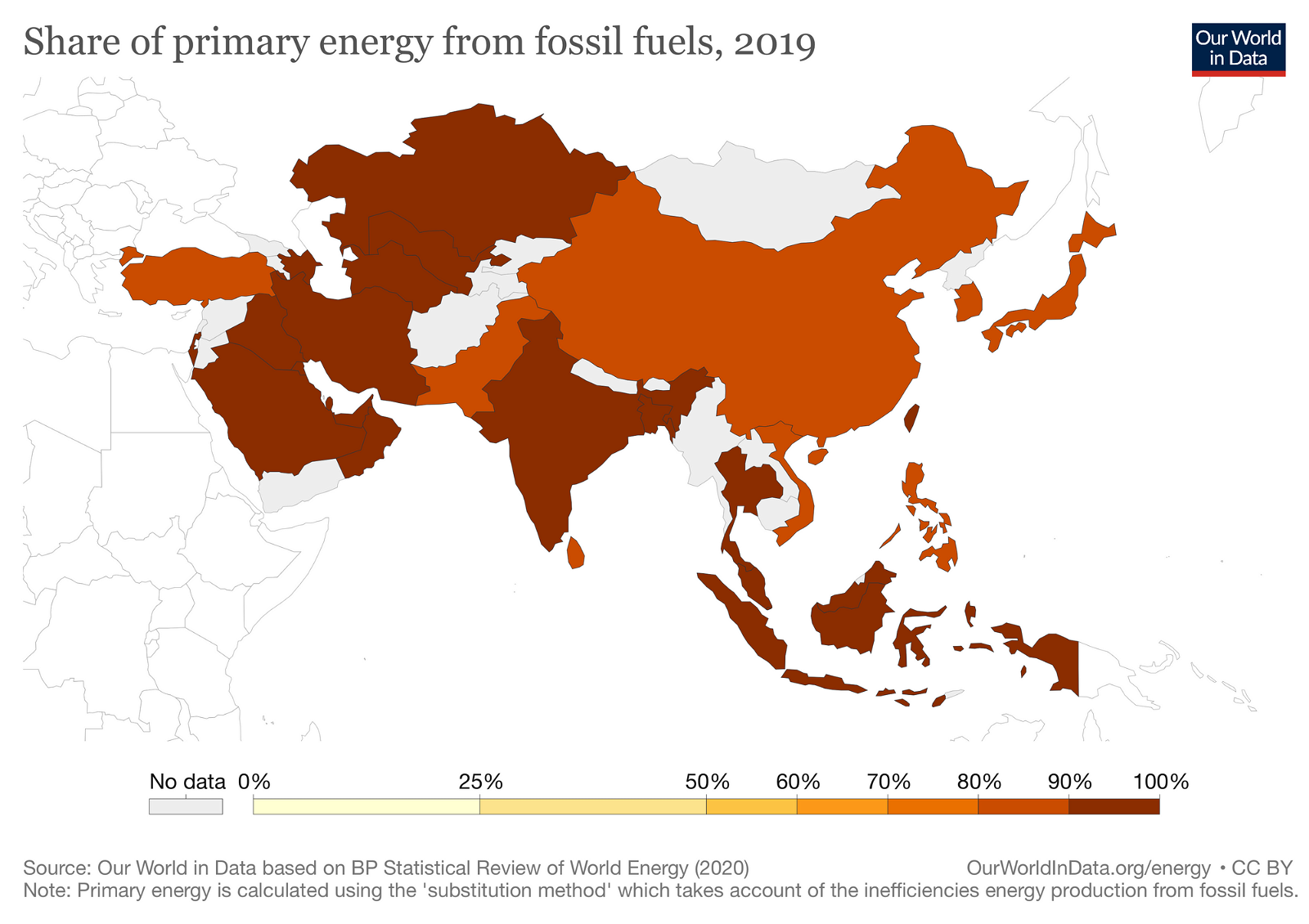

For Asian economies dependent on imported fossil fuels, volatile prices since 2020 have caused fuel shortages, exorbitant government subsidy burdens, inflation, food scarcity, and political instability. The Russian invasion of Ukraine is likely to exacerbate commodity price volatility, which undermines Asian countries’ economic growth and obstructs the region’s arduous recovery from the COVID-19 pandemic.

Natural gas and coal are often pitched as more reliable fuels for power generation than renewables. As a result, many Asian countries continue to support new fossil fuel infrastructure—power plants, pipelines, import terminals, etc. But the crisis demonstrates that ramping up fossil fuel imports will only make Asian economies more vulnerable to disruptions in global commodity markets.

Instead, countries can advance alternative technologies to bolster energy security. Distributed generation sources, energy storage technologies, microgrid systems, and electric transit technologies, among many other alternatives, can help countries improve self-sufficiency to create a more secure energy system—one free from geopolitical interference that contributes to both long-term climate and financial stability.

First, global energy prices will likely remain high and volatile for the near term. Prices were already widely expected to remain elevated in 2022, due primarily to the global economic rebound.

LNG prices, for example, were already susceptible to upward pressure due to interregional competition for cargoes between Asia and Europe, low European storage levels, limited piped exports from Russia to Europe, and harsh weather throughout the 2021-22 winter buying season. In October 2021, Asian LNG prices reached their highest level ever, at US$56 per million British thermal units (MMBtus).

The Russian invasion now adds upward pressure to LNG prices. Due to the risks of Russian piped gas to Europe, European countries seek to boost LNG purchases, further tightening the global market. This has knock-on effects on prices in Asia, which bounced to US$37/MMBtu. Some experts anticipate that LNG prices over winter 2022 could be even higher than record prices last year.

The second implication of the crisis is that continued commodity price volatility will continue to wreak havoc on national efforts to recover from the COVID-19 pandemic. Specifically, high-priced imports are raising consumer power prices and stoking fears about future fuel shortages in the region. As a result of exorbitant LNG prices, proposed and existing gas assets in Asia may go underutilized and risk becoming stranded assets.

In Bangladesh, the government increased subsidies following sky-high LNG prices in 2021, but the burden became too much to bear. In January, regulators proposed large hikes in gas and power tariffs, sparking protests. Amidst the upturn in commodity prices caused by the Russia-Ukraine crisis, state-run oil and gas companies are already incurring losses due to high import prices. The government will continue to face a choice between increasing subsidies, hiking tariffs further, or going without fuel altogether.

In the Philippines, oil prices have increased for nine straight weeks, and the government has warned that volatility in global commodity prices will continue to drive up the price of local goods. The peso has depreciated relative to the US dollar due to higher cost, foreign currency-denominated imports. Meanwhile, high daily COVID cases in the country along with inflation fears threaten to further undermine economic activity.

The third implication of the conflict is that fossil fuel companies are likely to argue that the world needs more fossil fuel infrastructure, not less. In the wake of the invasion, Japan’s JERA announced a partnership with ExxonMobil to build a new LNG import facility in Vietnam, Australia said it would target emerging LNG importers in Asia, and Pakistan’s Prime Minister travelled to Moscow to discuss a pipeline in Pakistan that would carry re-gasified LNG from the country’s southern coast to northern provinces.

First, energy insecurity and volatility are part and parcel of global fossil fuel markets. Myriad factors can affect commodity prices, including geopolitical conflicts, pandemics, outages at export infrastructure, and even ships getting stuck in major shipping routes. Such unexpected occurrences can affect prices for billions of consumers in importing countries and potentially trigger nationwide energy shortages.

Therefore, the continued buildout of LNG and other fossil fuel import infrastructure in Asia will only reinforce vulnerabilities related to energy security and economic growth. Although fossil fuels are often seen as reliable, secure fuels for power generation, the opposite is true: supply of imported fuels is constantly at the mercy of unpredictable disruptions.

The second lesson is that low-cost, domestic renewables represent a crucial hedge against the volatility of globally traded fossil fuels because renewables like wind and solar do not require fuel inputs. Instead, renewable energy costs are typically quoted in one, all-in-life-cycle price, allowing energy sector planners to assess future power prices more accurately for end-users and the economy.

And unlike the constantly fluctuating cost of fossil fuels, renewables have demonstrated consistently lower costs over time. It is difficult to predict fossil fuel prices months in advance, but renewables provide long-term economic and financial stability. Instead of increasing exposure to geopolitically unstable fossil fuel markets, it would be wise for Asian countries to maximize energy security and self-sufficiency by minimizing dependence on imported fossil fuels.

This article is also published on IEEFA. Energy Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

Filip Koprčina

Energy · Sustainable Finance

illuminem briefings

Power & Utilities · Nuclear

illuminem briefings

Oil & Gas · Energy

The Wall Street Journal

Renewables · Energy

Euractiv

Nuclear · Power & Utilities

Euronews

Oil & Gas · Energy