Planning a post-oil relationship with the Middle East

· 9 min read

Europe and the United States are formulating a plan to engage the MENA (Middle East & North Africa) region in the energy transition, turning oil producers into renewable energy providers.

“Today’s fossil fuel producers can become tomorrow’s clean energy champions to accelerate a net-zero transition. The MENA region is central to that shift”, tweeted the U.S. Climate Envoy John Kerry on Thursday, at the end of his visit to the United Arab Emirates, Saudi Arabia, and Egypt.

Kerry’s efforts have a twofold objective. In the great new game of the clean energy and eco-transition, Europe has a technological edge and a geopolitical vision. The US needs to stop playing “catch up” to remain a leader, economically and politically.

Producing clean energy from the desert to power the European grid would provide a roadmap for peace and sustainable development in the “enlarged Mediterranean”.

The plan is ambitious and fraught with geopolitical obstacles. Yet, technological progress has made it viable, while markets are driving the shift to renewable energy.

In a world threatened by the collapse of natural ecosystems and unrestrained climate change, markets make such plans highly relevant for anyone in a position of influence.

Italy is well placed to profit from stability in the region. Yet, Rome remains an observer, while others take to the green energy field.

The question that will make or break the European Green Deal is where and how we will generate and distribute the clean energy that will be needed by 2050. To put things into perspective, in 2018 the total electricity generated in the EU was 2800 TWhour. The total energy consumed by the 27, however, was four times that amount.

To reach that consumption benchmark while getting rid of EU dependency on fossil fuels (to achieve climate neutrality) will require direct electrification, sector coupling, and green hydrogen. In sum, we need to scale up renewables, particularly wind and solar, to decarbonise the energy mix.

Yet, there are limits to what we can do in Europe. Across the continent, onshore and offshore wind-generated electricity production hit the 458 TWhour mark in 2020, contributing 16% to our energy mix. Currently, Europe has 25GW offshore and 195GW onshore wind power installed. According to the EU Offshore Wind Strategy published last year, wind will deliver 25% of the bloc’s power demands by 2030 and 50% in 2050. But land is precious, and the energy transition must be achieved together with the protection of ecosystems and biodiversity.

That is why an “old” plan to produce clean energy from the Sahara Desert (solar) and other renewables sources in the region (wind), has now been revived and is gaining momentum with German industrial and diplomatic backing. In its latest version, the plan includes green hydrogen production in the Gulf.

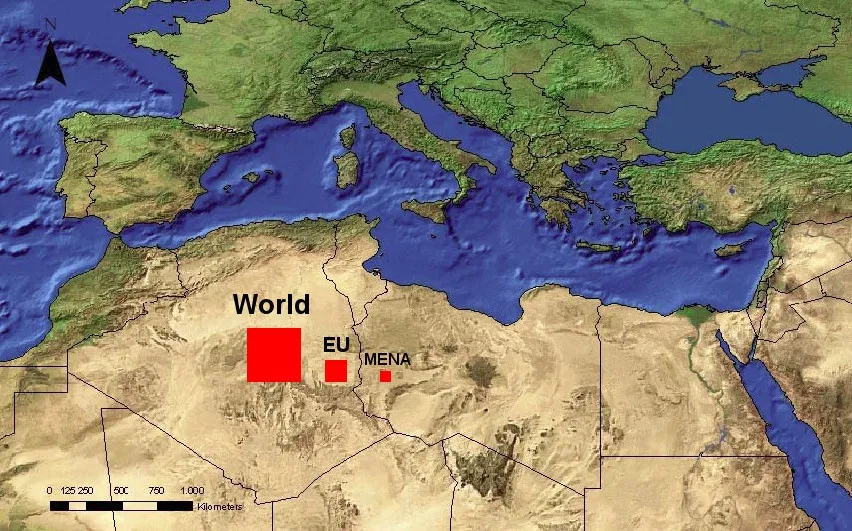

It all starts from the bottom line: 1.2% of the Sahara Desert is sufficient to cover all the energy demand of the world at competitive costs with solar power.

The vision of a green hydrogen economy is also reawakening the vision of desert power. Hydrogen would allow renewable power to dock on Europe’s Mediterranean shores in a different form: green molecules. The cheap, renewably generated electricity could be used to produce green hydrogen onsite. Existing gas pipelines on the seabed could be used for transport. Ammonia or power fuels could be shipped by tanker to any place in the world. That is a paradigm-change in electricity production with the incremental reuse of existing infrastructure.

Two minutes of sunlight are enough to power the world for one year. And it doesn’t cost much.

The science behind the vision is solid. Every two minutes, the energy reaching the earth from the sun is equivalent to humanity’s annual energy needs. According to the World Energy Consumption & Statistics 2020, global energy consumption in 2015 (coal, oil, hydroelectric, nuclear and renewable) was 13,000 Million Ton Oil Equivalent (13,000 MTOE), which correspond to 17,3 Terawatts annual consumption.

With today’s technology and moderate conversion efficiency, producing 17,4 TWhour would require us to cover an area of the Earth 335 kilometers by 335 kilometres with solar panels. Approximately 111,369 square kilometres is enough to power the world, which is equivalent to 1.2% of the Sahara Desert. That energy would be clean and would come at a competitive cost. There is no way coal, oil, geothermal or nuclear can compete with this in the longer term.

To harness renewable energy from the desert would also solve the conundrum posed by conflicting land use, limiting the negative impacts of large-scale solar plants on ecosystems and biodiversity, even considering the increase of temperature induced by solar farms.

The cost for such an investment would near five trillion dollars. This is a one-time investment that does not consider economies of scale or savings. This amount corresponds to less than 10% of the world’s global Gross Domestic Product. The economic rationale is strengthened by the upward trend of carbon prices in Europe (ETS) and upcoming global carbon tax systems.

To put this amount into perspective, the cost of a 1 GWe (Gigawatt electric) nuclear plant is around three billion dollars. The maths are simple: to generate 17,3 TWhour of nuclear power would cost fifty-two trillion dollars, that is ten times the cost of the solar energy equivalent.

Recent studies suggest that the 1.5℃ is technically feasible at relatively low-cost for the overall economy. The “Research Report on Global Energy Interconnection (GEI) for addressing Climate Change” comprehensively analyses the energy system and mitigation technology of GEI in 2℃ and 1.5℃ scenarios. The results are remarkable. By 2050, the global intercontinental power trading volume will amount to 800TWh; the cross-region power flow will be 660GW; clean energy will account for 86% in primary energy; the cumulative global CO2 emissions will be kept under 510 billion tons; and the discharge of sulfur dioxide, nitric oxide and PM2.5 will drop by 86%, 98% and 93% respectively.

The point is how quickly will economies and societies move to the electrification of their infrastructure. The GEI report suggests that keeping the global temperature rise below the 2°C benchmark requires investment in electrification to the tune of 0.2% and 1.0% of global GDP, each year, until 2050. The range highlights that economies of scale can lower the macroeconomic cost. Most importantly, these numbers do not account for the costs of inaction.

In essence, decarbonisation and electrification go hand-in-hand and the shortest route to the objective goes through the MENA region.

The upcoming energy structure requires different national security perspectives. The current fossil-based system is hierarchical, with the interests of producers, importers, and energy transit countries potentially colliding.

As renewables are more equally distributed and more infrastructure-reliant, foreign energy “dependency” is reduced. Renewable energy supply pushes for the further interconnecting of the higher voltage systems across countries and continents.

“All countries visited”, reads the State Department’s press release closing Kerry’s visit to the three MENA countries, responded “enthusiastically” to the visit. The discussions highlighted the importance of a successful COP26. The Italian G20 is also in the background.

Riyadh has laid out concrete plans for achieving the announced target of 50% electricity generation from renewable sources by 2030 and for scaling up hydrogen and carbon capture technologies.

Nothing new under the sun, it is appropriate to say.

These issues have been on the table of European chancelleries for some time. At the Energy Transition Dialogue 2021 held in Berlin last March, the Saudi Minister for Energy, speaking on a panel with John Kerry and the EU Commissioner for energy among others, had already addressed the key points of the country’s transformation from a major oil producer to a major exporter of clean energy and hydrogen. The German industrial system is ready to provide credit and investment.

As for Egypt, earlier this year, Cairo signed an agreement with Siemens to scope out a 1.65 GWp green hydrogen production project.

Even more importantly, the land of the pharaohs is part of the EuroAfrica Interconnector, a project to bridge Africa and Europe via HVDC transmission lines and submarine cables, with a transmission capacity of 2GW in both directions, between Greece, Cyprus and Egypt. The Republic of Cyprus has issued the final building permit for the Egypt-Cyprus interconnection system in August 2020.

The new energy highway will start in Damietta, on the Egyptian coast, and will be a new landmark for Mediterranean energy geopolitics. Until now, there are only two energy interconnectors between Europe and Africa. Both connect Morocco to Spain. A third with 700 MW capacity will be commissioned by 2026, according to a Memorandum of Understanding signed between Red Eléctrica de España (REE) and its Moroccan counterpart in 2019. The EU has an interconnection target of at least 10% by 2020 and 15% by 2030.

However, not everyone moves at the same speed. A senior Brussels technocrat recently commented on Rome’s recovery plan, telling me that Italy today has more gas in its belly – and in its energy matrix – than it should have in 10 years’ time. Yet, Rome seems to be resting on its fossil laurels.

A long planned project to build an interconnection between Sicily and Tunisia (200 km) is sitting in a drawer while the UK-based company Xlinks is planning to build 10.5 GW of wind and solar capacity in Morocco and sell the generated power in the UK through a 3,800 km submarine cable. The Saudi ACWA Power Renewable Energy Holding, and the Chinese Silk Road Fund are partners in the British-led Xlinks project.

After decades of inaction, the world is speeding up measures to tackle the existential threat of climate change. The moment is right for the MENA region to contribute with their enormous clean energy potential, stepping up their generation and transmission capacity. The race for a clean development model powered by renewables and hydrogen has just started.

The political will to act also rests on solid economic foundations. Since 2010, the price of solar energy has dropped: by 82% for photovoltaic solar and 49% for Concentrated Solar Power (CSP). Wind and solar power are today the least-expensive option for bulk electricity for two-thirds of the global population, 71% of global GDP, and 85% of global power generation. A new financial and legal system for the post-fossil economy is emerging to regulate international trade and markets. The transition offers excellent business opportunities and promises the creation of sustainable jobs within advanced, future-facing industries.

Climate neutral is very good business in a world of sinking oil assets. For oil-dependent economies, this is an existential race against time with both economic and geopolitical significance.

This article is also published on BrusselsMorning. Energy Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

Filip Koprčina

Energy · Sustainable Finance

illuminem briefings

Power & Utilities · Nuclear

illuminem briefings

Oil & Gas · Energy

The Wall Street Journal

Renewables · Energy

Euractiv

Nuclear · Power & Utilities

Euronews

Oil & Gas · Energy