It's time for a bad bank

PexelsPexels

PexelsPexels· 6 min read

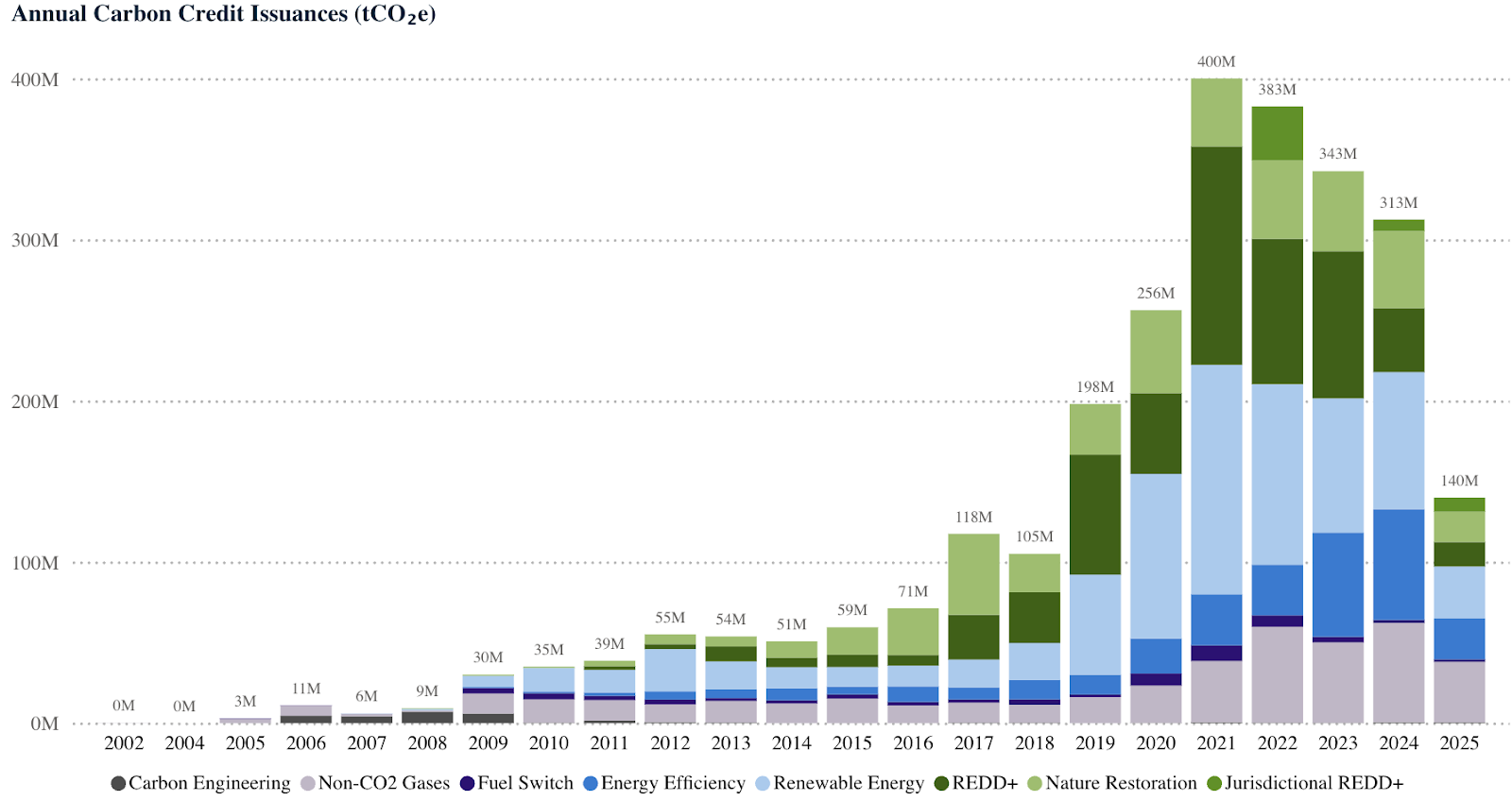

Since the beginning of the voluntary carbon market (VCM), we’ve seen a consistent trend: the volume of credits issued has always exceeded the volume retired by buyers. I still remember the early histograms presented in the pioneering reports by Ecosystem Marketplace, first launched at Carbon Expo in Cologne. Year after year, those charts showed the same pattern — issuance climbing steadily, while retirements lagged behind, leaving a growing pool of unsold credits. Billions of carbon credits have been issued under rules and assumptions that no longer hold.

Source: Historical annual carbon credits issuance source MSCI

Many of these legacy credits — issued before the Paris Agreement, using outdated baselines or obsolete methodologies — are still circulating. They’re cheap, questionable, and increasingly incompatible with today’s integrity standards. This overhang is becoming a problem. It distorts prices, scares away buyers, and undermines the trust needed to unlock climate finance.

And believe it or not — carbon credits don’t expire. In principle, if you find a buyer, you can still sell a credit that’s 20 years old.

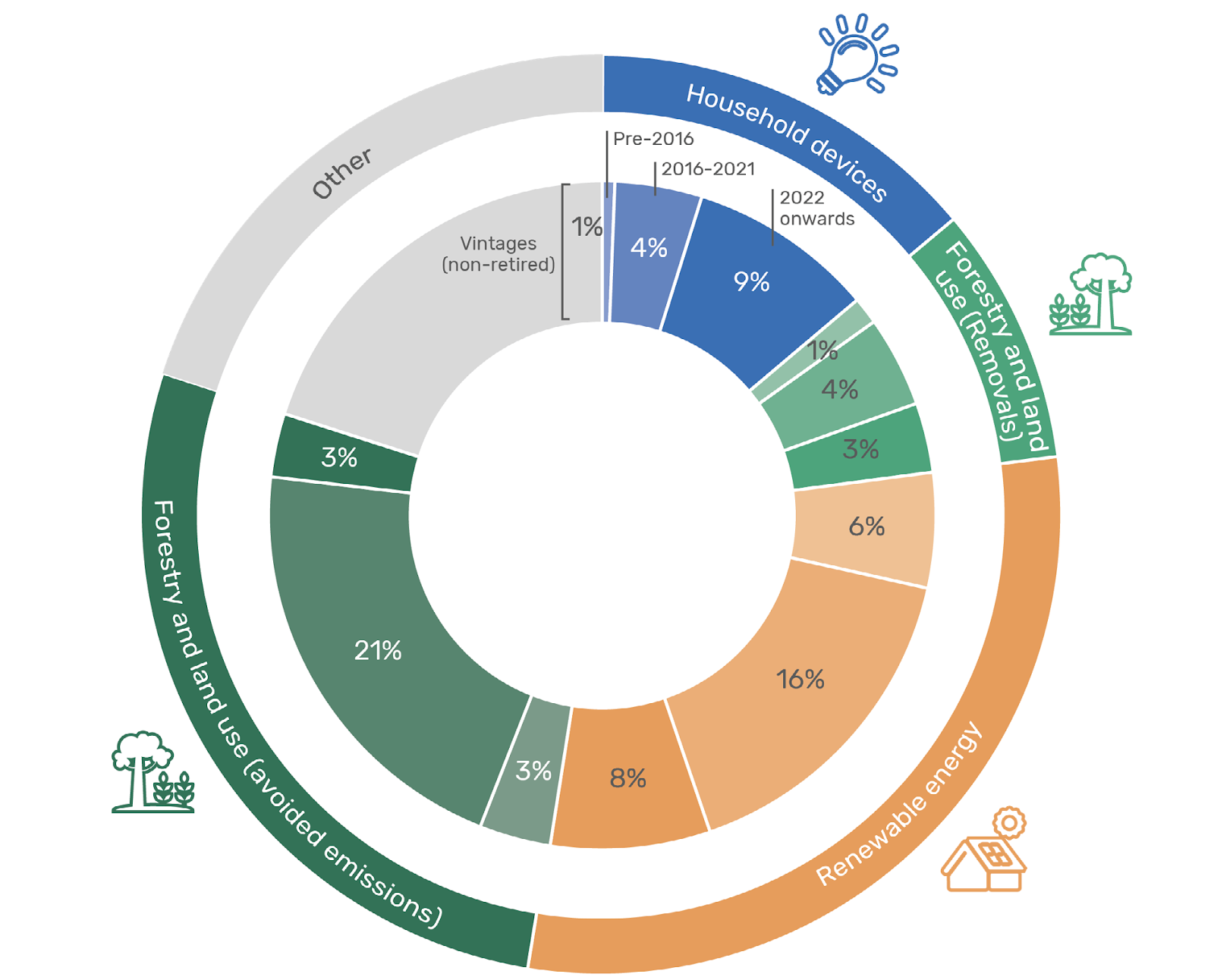

According to the latest World Bank data, the global pool of unretired credits from independent crediting mechanisms has reached almost 1 billion tons. Over two-thirds of this volume comes from pre-2022 vintages — meaning the reductions or removals occurred before 2022. Most of these credits originate from forestry and land use (36%) and renewable energy (30%) projects — the same categories that historically dominated issuance. But many of these credits are now stranded. They’re not aligned with net-zero frameworks. They’re not eligible under new quality requirements or evolving claims standards. And they’re no longer finding buyers.

Source: Breakdown of unretired credits from independent crediting mechanisms by project type and credit vintage, as April 2025 - Source: World Bank

We’ve seen this before — in finance. After the 2008 crisis, banks needed to remove toxic assets from their balance sheets. The solution was the creation of “bad banks”: structures to isolate and retire problematic assets so the healthy part of the market could recover. Can the carbon market do the same?

A carbon bad bank would not cancel everything. It would not punish developers or deny the value of early efforts. But it would create a mechanism to identify, isolate, and retire credits that no longer belong in the active market. A ring-fence. A clean-up. A signal that quality now matters more than ever.

The idea that a credit issued in 2012 — or earlier — can still be used for a 2030 net-zero claim is simply not credible.

Renewable Energy Certificates — whether Guarantees of Origin (GOs) in Europe, RECs in the U.S., or I-RECs internationally — are subject to expiration rules. They must typically be used within the same calendar year the megawatt-hour is generated, or they lose eligibility for most corporate disclosures and compliance programs. Compliance carbon markets also enforce banking limits and vintage restrictions. The VCM needs to catch up. A reasonable threshold — for example, limiting the use of credits older than 10 years — would bring much-needed discipline and signal that climate action must be current, not historical.

I often ask myself: why is it still possible to hold, sell, and retire credits issued 15 years ago? The unsettling truth is that we’re still seeing retirements from vintages older than 2010. The fact that these volumes are sitting in registries — unsold but technically “valid” — gives the illusion of an oversupplied market. But that’s wrong. If we applied the integrity filters introduced in the last three years, the market would actually be undersupplied. There’s no real glut — only legacy noise.

A carbon bad bank could take many forms: a dedicated SPV, a coordinated retirement facility funded by donors or buyer alliances, or a tagging mechanism inside registries to flag non-eligible stock. What matters is the outcome — removing the overhang, rebuilding integrity, and restoring a credible baseline for future carbon finance.

Some actors are already laying the groundwork for credit reclassification — even if no one has yet launched a full-scale “carbon bad bank.” The intense scrutiny on quality and integrity over the past few years has changed the landscape. It exposed weaknesses, but more importantly, it gave the market what it had long been missing: standards, ratings, methodologies, and governance mechanisms that allow us to finally separate what is credible from what is obsolete. ICVCM is assessing entire credit categories under its Core Carbon Principles, creating a system-wide filter for environmental and procedural integrity. At the same time, rating agencies like BeZero, Sylvera, Calyx, and Renoster are building credit- and methodology-level risk assessments that offer project-level visibility — helping identify which credits still have future claim value and which should be reclassified or phased out.

What we need now is clear: to systematically scrutinize the nearly 1 billion unretired credits still in the market, including those from projects no longer issuing new volumes. By applying the tools developed over the last three years — vintage controls, quality benchmarks, category-level and credit-level ratings — we can determine which credits remain usable under today’s integrity expectations, and which are effectively stranded assets. All of this data already exists within the carbon standards registries — and considering that just two standards account for over 90% of all certified credits issued in the VCM, this should not be rocket science.

This isn’t about blame or perfection. It’s about restoring price discovery, rebuilding trust, and creating a transparent baseline that allows carbon finance to scale with credibility.

If we don’t isolate low-integrity legacy stock, it will continue to drag down the entire market — including the very projects we need to scale. Prices will stay low. Trust will stay broken. And the promise of carbon finance will remain unfulfilled.

Every time I speak with people about the bad bank concept, I get the same reaction: “It’s a good idea.” But the moment you dig deeper, you find resistance. Many actors would rather avoid the conversation — because it means admitting that something went wrong. That these credits are heading toward becoming stranded assets anyway, and that eventually no one will be able to buy them. The strategy, for now, seems to be: leave them untouched, and hope the market forgets.

That approach won’t work. The voluntary carbon market has played a meaningful role in channeling climate finance and supporting mitigation projects across the globe. But 15 years in this space is a lifetime — and it’s time to admit that not all credits are created equal. Many older credits were valid under the standards of their time, but today’s expectations around quality, integrity, and recency have rightly moved forward. We can recognize the progress the market has enabled — while also accepting that it now needs to evolve.

The real mistake is the carry-over — the fact that these old credits can still be bought and used today. We need to reclassify them. And we need to make sure that obsolete ones are no longer available in the market. The biggest risk is that non-expert buyers — often SMEs or new entrants — still purchase them, believing they’re certified, credible, and compliant. They’re not.

A carbon bad bank won’t solve every problem.

But it’s the next logical step.

This article is also published on Climate Playbook. illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Carbon Regulations · Carbon Market

illuminem briefings

Carbon Regulations · Carbon Market

illuminem briefings

Carbon Capture & Storage · Carbon

Utility Dive

Carbon · Power & Utilities

Sustainable Views

Carbon Regulations · Carbon

Carbon Herald

Carbon Market · Carbon Regulations