Implications of the outperformance of active sustainable investing

· 12 min read

Although many US states such as Florida[i] and Texas[ii] have been recently passing legislation preventing their pension systems from considering environmental, social, and corporate governance (ESG) factors, active sustainable investors have been financially outperforming over the long-term and earning higher returns for their clients while managing tens of billions more dollars on the back of such financial success.

Other states such as Indiana[iii], Kentucky[iv], and North Dakota[v] considered similar legislation, but are understandably passing on adopting new “anti-ESG” rules out of concern that such laws could reduce the financial returns experienced by beneficiaries.

Florida, however, has persisted[vi], even though evidence suggests such “anti-ESG”/”anti-woke” rules are likely to negatively impact financial returns.

To further illustrate this point of pension funds potentially experiencing lower financial returns due to “anti-ESG” legislation, the Sustainable Finance Institute endeavored to look at how sustainability-focused funds have been performing for their beneficiary clients.

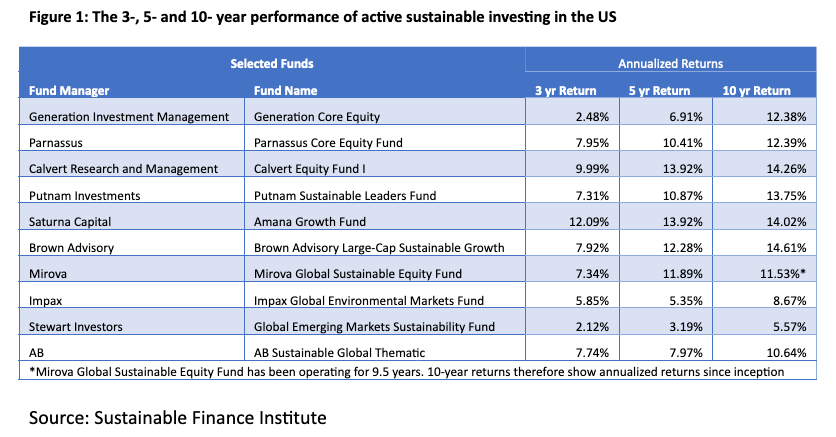

The study focused on active sustainable investors, who aim to maximize financial returns for their clients while prioritizing sustainability. For our analysis, we selected active fund managers with over $10 billion in assets under management, more than 10 years of operation, and accessibility to US investors.

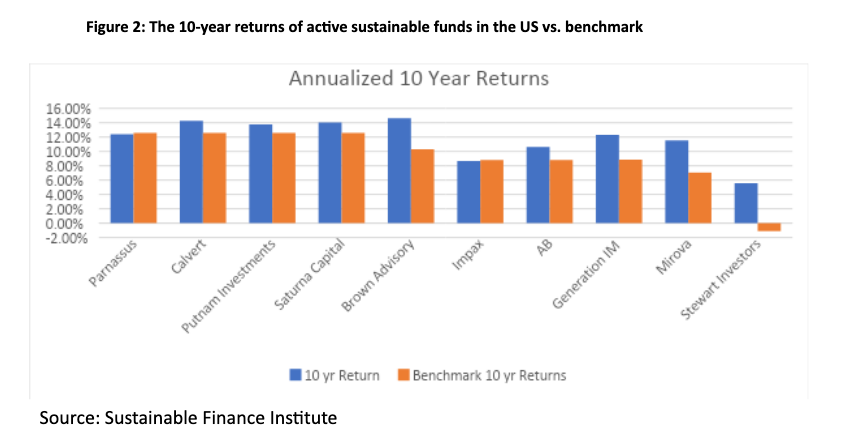

We found 10 such funds as listed below and analyzed their returns against their chosen benchmarks up through Dec 31st, 2022 (Figure 1).

Looking at 10-year annualized returns, eight of the ten funds outperformed their benchmark by a margin of 100 bp or more. Four of the eight funds, the largest sustainable funds managed by Generation Investment Management, Stewart Investors, Brown Advisory, and Mirova, beat their benchmark by more than 3%. On average, sustainability-focused funds earned 2.48% more than then their benchmark. Only two funds barely underperformed, yielding returns within 30 bp of the benchmark. Over 10 years, none of the funds significantly underperformed demonstrating some of the benefits and resilience of ESG-focused investing.

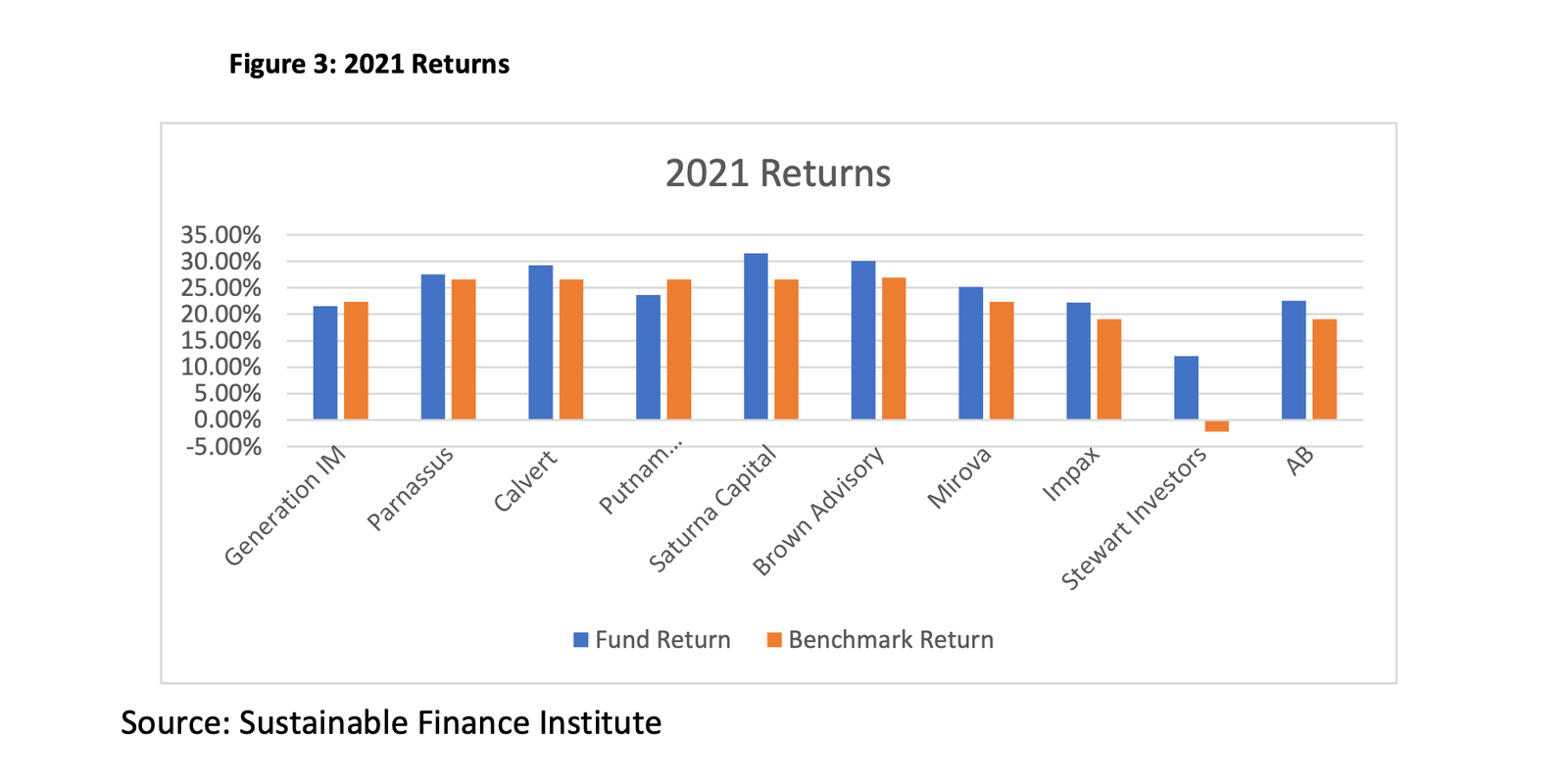

Following the worst of the COVID pandemic and related supply chain constraints, and amid heightened geopolitical tensions, 2022 was a year of turmoil for most investors. The S&P 500 fell 18%, making it the worst year for markets since 2008. This shock hit fund managers across most global markets, including sustainability-focused investors. 8 out of 10 funds underperformed relative to their benchmark.

While 2022 may have been a bad year, the investors in our study consistently beat benchmarks in both 2020 and 2021. For example, eight of these ten funds in 2021 beat their benchmarks with an average of 3.17% higher return across all funds analyzed.

Looking at these funds’ performance through different time periods helps frame how these funds can benefit pension fund beneficiaries and other long-term focused investors.

Active sustainable investors seek to protect investors from risks incurred by badly run companies (e.g., recent governance scandals tend to wipe out 50 percent of shareholder value) while seizing the many opportunities emerging from ongoing innovation as well as potential shifts in consumer preference and in the global economy. We endeavored to study such funds and found financial outperformance against the benchmark after fees over the long term.

This outperformance for active sustainable investing has been seen as well over longer time periods. Going back to 2008, in our first book on the subject, Sustainable Investing: The Art of Long Term Performance, we looked at all of the 850 funds then publicly available globally using sustainability as a primary consideration and found outperformance over 1-, 3- and 5- years for funds similarly taking a positive approach[vii]. In 2013, our Value Driver Model study for the Global Compact and PRI[viii] found significant outperformance for the previous 3 years for companies transforming towards sustainability in terms of increased market share from evolving towards offering more sustainable products and services, better risk management, and increased productivity from energy efficiency savings and human capital optimization strategies. In 2018, a Brown University study found comprehensive outperformance for active sustainable investing in the US as opposed to passive approaches which did not outperform.

And so our studies have demonstrated over 3-, 5-, 10- and 20- years that active sustainable investing outperforms financially more often than not at a time when most active managers underperform their benchmarks after fees. This fully refutes arguments that “ESG” leads to lower financial returns and makes active sustainable investing the strategy of choice for investors, making this a key opportunity for all active fund managers to consider to drive maximized financial performance while helping achieve societal improvement.

Opponents of these practices argue that including ESG factors in investment decision-making is a violation of fiduciary duty, arguing that investment decisions should be made solely on a company's potential returns rather than including extraneous factors. This argument hangs on the fact that including ESG factors will result in lower returns. In reality, ESG considerations can lead to improved financial performance.

Other evidence of such improved financial outcomes includes NYU Stern’s Center for Sustainable Business which hosts a freely accessible body of academic case studies[ix] of corporate strategies which specifically lead to better financial returns while also improving environmental and social impacts. It is hard to see how any interpretation of fiduciary duty can be forced to ignore improving societal outcomes when there is clear evidence of better financial performance over time when pursuing such specific strategies.

To illustrate, let's consider the Brown Advisory Sustainable Growth Fund, which aims to invest in a concentrated portfolio of companies with internal sustainability strategies that generate tangible business benefits, such as revenue growth, cost improvement, or enhanced franchise value. The fund looks for companies whose products have a competitive advantage due to sustainability drivers, such as resource-efficient design or manufacturing, and that offer solutions to long-term sustainability challenges[x].

Over the last ten years, the Brown Advisory Large Cap Sustainable Growth Strategy has generated an average annual return of 15%. At the same time, they seek to generate positive outcomes ranging from emission reductions to improved health outcomes.

Further, fund managers who perform shareholder engagement with public companies, such as Norfolk Southern, are looking to help avoid the sort of disasters that have affected so many lives in small towns such as East Palestine, Ohio.

Shareholder engagement is an important check and balance on the financial system which ensures corporations hear from leading investors to ensure their practices meet a minimum acceptable standard of safety for communities and employees alike, especially when governments at times remove safety protocols which can lead to less safe conditions for the average American family.

This ties to how companies are governed when left on their own, which can result in situations as seen recently at companies such as Boeing or Southwest Airlines. Both saw dramatic share price declines due to safety concerns or a lack of minimum operational competence while trying to be too efficient on behalf of maximizing returns for shareholders.

Investors focused on governance can help establish minimum standards on how companies perform, which can preserve shareholder value for investors. Without such checks and balances in place and with ongoing pressure on removing regulations in the US, more disasters like train derailments and other incidents creating significant pollution could damage more communities, lowering property value and affecting lives and families.

Governance is also essential when it comes to non-US investing. Asia already makes up half of the global economy by many measures. Would you ever really want to consider trusting your money to invest in a developing economy’s public companies without knowing how those companies are being governed? Without consideration of corporate governance, such investments would be a clear breach of fiduciary duty. Are “anti-ESG” bills being put forward in states such as Florida and Texas suggesting that their pension funds should ignore Asia altogether? The fiduciary duty would seem to require consideration of global market opportunities and whether you can trust and, therefore, whether your money is being invested in well-run companies in the process, making it hard to understand how “anti-ESG” legislation can be allowed to stand up under reasonable scrutiny, regardless of the outperformance evidence seen in the managers analyzed above.

As a result of the outperformance being seen over time and the possibility of “anti-ESG” legislation accelerating or getting stronger, this also creates concerns about US competitiveness, not only for the states in question but for the US more generally. If not, leading on issues such as climate change, the EU has made clear that they intend on establishing tariffs such as those in the Carbon Border Adjustment Mechanism of December 2022[xi]. Such tariffs, if increased over time (and the EU ETS carbon price is already over 100 euros per metric ton of carbon) could make selling domestic goods overseas more expensive, making them less competitive over time.

All is not always wine and roses for the sustainable investing industry in the US. There are legitimate concerns that need to be addressed when it comes to greenwashing, as well as the true impact of sustainable investing. It is important to understand, first of all, that there isn’t one thing called “ESG Investing,” but rather seven distinct investment strategies investors use when considering sustainability issues.

Let’s look at the impact outcome potential for what we call the Seven Tribes of Sustainable Investing.

Negative screening represents the origins of the field of what used to be called Socially Responsible Investing. We believe it is okay, of course, for any investor, whether an individual, a family, or a large asset owner such as a pension fund, university endowment, or foundation not to invest in every single company or investment opportunity that might come their way. Most investors put money into specific opportunities that they think will make money for themselves and their beneficiaries. Pension funds need to maximize financial returns within the asset allocation and annual return expectations they set for themselves and their beneficiaries. Divestment as a primary strategy often does not create meaningful change. One person or organization sells shares, another buys them and there has been no evidence that there is likely to be a lack of potential buyers of any asset that has financial value or potential value. Calls to “ban ESG” are just one more negative screen, in effect, and are similarly not the best way to optimize financial performance for investors as a result.

Negative screening started with calls for divestment during the apartheid, for example, which was an easier ask as South African business was a very small component of corporate supply chains versus divestment from fossil fuel production which use is embedded in the supply chains of all large public companies. Some calls for divestment from sectors are more complex than others as a result. Here is likely where the “anti-ESG” focus has come from, as there would be a logical concern that if enough investors didn’t want to own specific assets, it could increase the cost of capital or otherwise create a stigma on such assets, but sustainable investing is more than just divestment.

Positive or “best in class” approaches are the polar opposite of negative screening. Rather than investing in an index and subtracting out a few perceived bad actors (which tends not to perform all that well financially, positive approaches look for specific opportunities, especially perhaps for solving climate change. Norges Bank, for example, one of the world’s largest asset owners, lost money divesting away from tobacco and weapons they reported a few years ago[xii]).

Such opportunities include companies providing solutions that can help make industries more efficient, or as is increasingly seen in this age of COVID, healthcare has become a key focus for investors interested in companies aiming to help solve social challenges that relate to health. VC is also increasingly being tilted toward companies seeking to solve sustainability challenges, with over $100B invested in recent years and no slowdown seen in climate-focused fund activity[xiii]. As was seen in our recent study, these are all active investment strategies, where impact and the potential to maximize financial performance while seeking positive opportunities can be more challenging.

Impact investing is again different, now seeing over $1.1 trillion in investment, largely in solutions for those less well-off such as by improving access to healthcare, financial services, housing, education, and similar largely private market investments[xiv].

Thematic investing is also essential, with Bloomberg New Energy Finance calling for more trillions per year to solve climate change[xv]. Much of this funding will come in the form of renewable energy project finance, including derisking strategies as has been largely deployed to date. Many case studies, for example solving the SDGs using finance, can be found in our InvestNYC white paper published in 2021[xvi].

Integration is where greenwashing concerns have largely come into play. Concerns about the quality of ESG data are well documented[xvii]. ESG-focused ETFs may be unlikely to qualify for the SEC’s climate disclosure proposed categorizations of focus or impact, potentially making them less attractive over time for investors seeking positive impact and better financial returns[xviii], further clarifying that there are many different strategies and outcomes from sustainable investing that makes categorizing ESG Investing as one single thing inappropriate.

Shareholder engagement creates an essential and otherwise missing check and balance on the financial system. Some pension funds invest in indexes and then engage with the companies they own to seek better outcomes. CalPERS, for example, previously reported financial outperformance that was attributed to shareholder engagement efforts targeted at improving poorer performers on governance[xix].

Minimum standards represent one more methodology to “lift the tide of all boats.” For example, if one visits a restaurant in Manhattan, there is a letter in the window telling you whether the food is safe to eat, yet investment has not had this “seal of approval” in place historically. Increasingly, asset owners such as the Yale Endowment[xx], NYS Common[xxi], and Norges Bank[xxii] have been putting such minimum standards in place, which in Asia for example, could be quite useful for investors and society if put in place comprehensively.

As a result of all the very different strategies described above, we recently wrote about the 10 common misunderstandings when it comes to ESG, which could be useful for readers to further reference and clarify unnecessary confusion[xxiii]. Opportunities clearly exist to target both financial outperformance and sustainability and impact improvement. The overarching goal should be for a majority of investors to fully consider sustainability issues across all asset classes so that these become embedded into financial decision-making. Progress is being made, but more is necessary. The outperformance of active sustainable investing is an encouraging sign that the future of active investment across asset classes is sustainable.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

March 16, 2023: This article has been edited to reflect updated numbers from Generation Investment Management.

illuminem briefings

Cities · Sustainable Investment

Filip Koprčina

Energy Transition · Sustainable Investment

illuminem briefings

AI · Sustainable Investment

Eco Business

Sustainable Investment · Adaptation

The Guardian

Electric Vehicles · Sustainable Investment

Axios

Nuclear · Sustainable Investment