· 5 min read

The voluntary carbon markets are booming, predominantly driven by expectations that carbon offsetting demand from corporate buyers is set to increase as a result of corporate net zero commitments.

To meet demand, it is clear that the supply of carbon projects will need to scale. As such, carbon project developers are actively looking for ways to finance their carbon project pipelines. The number of participants in this market has increased, with the emergence of actors such as carbon trading desks, carbon streaming and carbon-focused investment funds taking a more active role, and taking earlier exposure in the carbon project development curve.

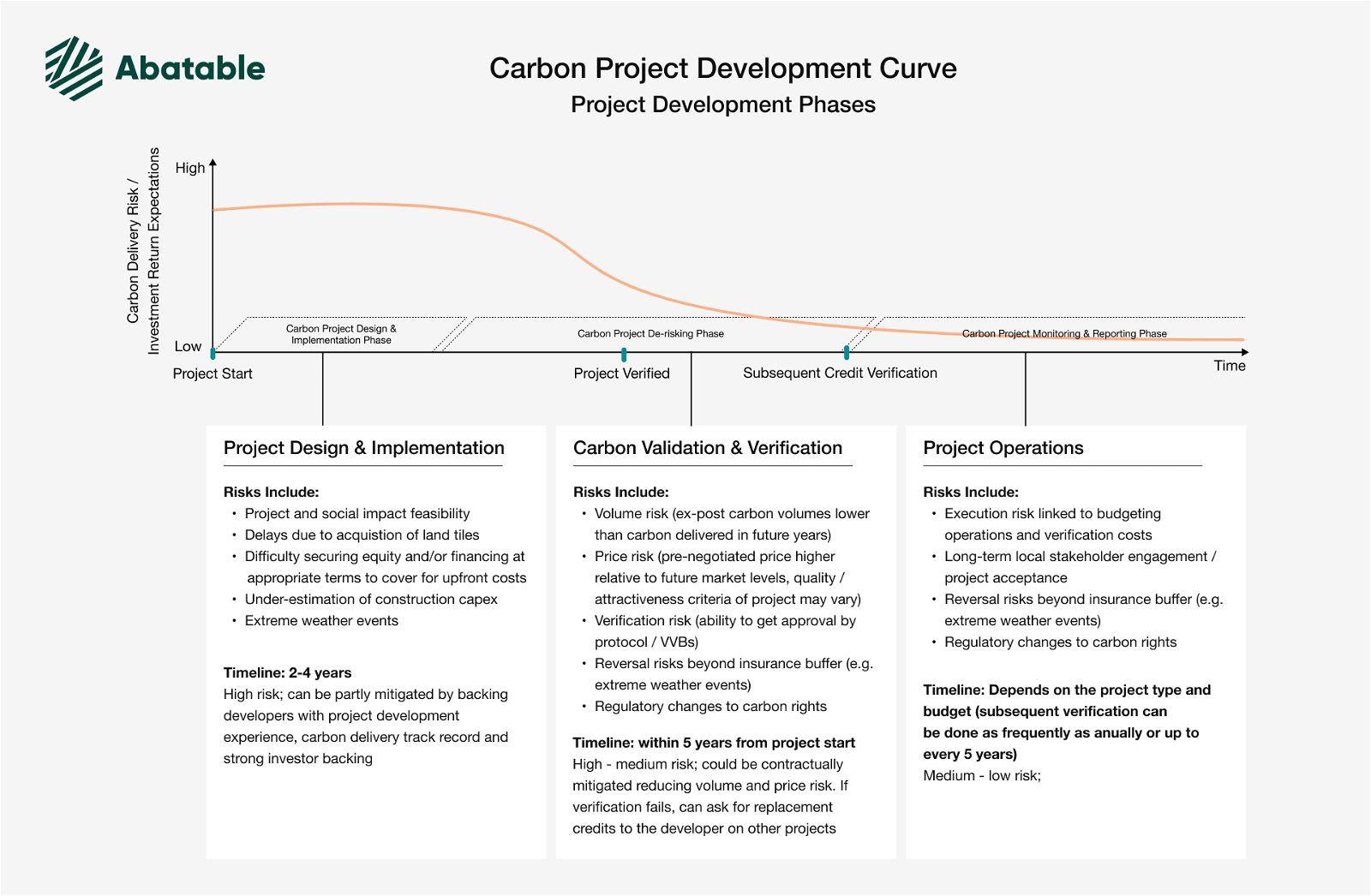

Abatable has developed a greater understanding of the so-called “Carbon Project Development Curve” which maps the investment risks and return expectations of a carbon project along its project lifetime.

The three main Carbon Project Development phases

- Project design & implementation: carbon project developers often use small equity investments or grants to finance carbon project feasibility studies. Early stage development involves taking a binary risk in assessing carbon potential of projects, with high uncertainty of carbon outcomes generated from the project. Project scale potential, strong project development experience, particularly the developer’s carbon delivery track record over time, and strong investor backing work as de-risking factors from a carbon project development standpoint.

- Project validation & verification: carbon project developers can de-risk their projects significantly as they get closer to the first carbon verification event, working with validators for the first time to assess eligibility of carbon projects under specific carbon methodologies and protocols. The carbon delivery risk drops substantially once the project has been verified and approved by a carbon standard. with more predictable carbon outcomes validated over the lifetime of the project. However, the project may still be subject to implementation and delivery risks, for example, if the project is subject to extreme climatic events and carbon volumes end up being lower than anticipated.

- Project operations: As the project continues its carbon operations, it monitors and reports upon its activities by verifying and issuing verified carbon units. At this point, earlier implementation risk is reduced, and to a lesser extent, the project is still subject to risks of carbon delivery underperformance. The risk buffer, typically around 10-20% of the overall net GHG emission reductions, acts as an insurance buffer in the event of reversal events. However the project may be still exposed to extreme climatic risks, which lead to underperformance beyond the risk buffer reserve. Regulatory risks are also significant, particularly in the context of changes which arise as a result of the project needing to require corresponding adjustments under the new Article 6 jurisdictional framework.

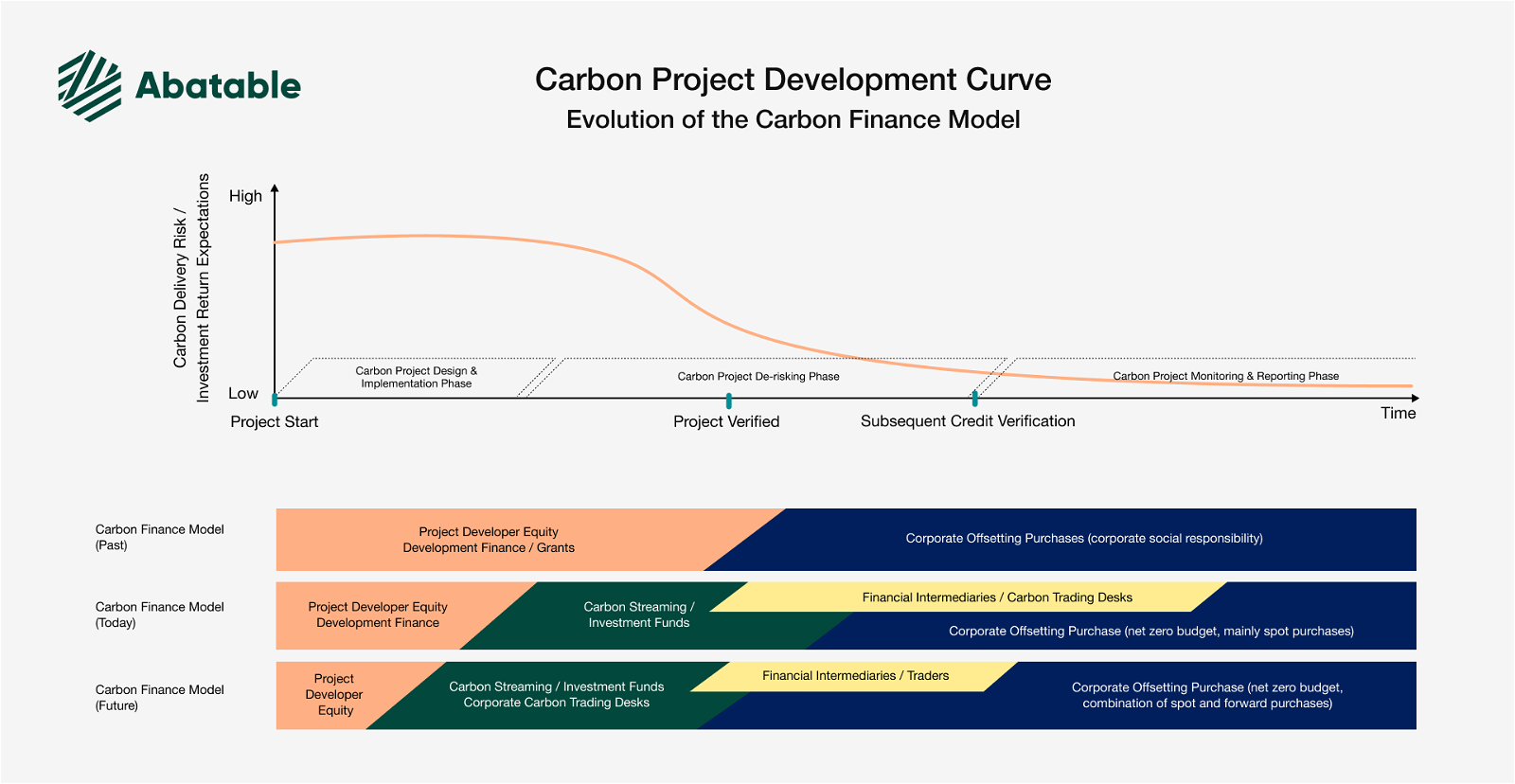

The financial landscape has evolved substantially along the carbon project development curve over the last few years.

The finance model of Carbon Project Development

- The carbon finance model historically relied on carbon project developers using equity investments, development finance and conservation grants to finance early stage carbon project design and implementation. Projects had to go through the verification stage and beyond to be marketed and sold to the few corporate buyers who used their corporate social responsibility budgets to purchase verified carbon units (often considered a form of donation, with no “net zero” carbon accounting expectations).

- With the resurgence of interest in carbon markets, financial intermediation has started to re-emerge, particularly in the late stage project implementation phase. Carbon streaming and investment funds, as well as financial intermediaries and some carbon trading desks have started to offer structured finance solutions to developers, investing capital and taking a higher level of risk, often in the form of project verification and implementation risk. These structured solutions facilitate developers who now can use less equity at later stages of development and allows developers to unlock capital which can be re-invested to finance earlier stage pipeline development. The landscape has also seen a change of strategy from the corporate buyer standpoint, with corporate buyers now focused on securing larger carbon volumes for the purpose of carbon accounting offsetting as part of their net zero plans. However, corporate buyers continue to prefer to purchase existing inventory of verified carbon units through spot purchases, with a general resistance to take on verification and price risks.

- With the rise in interest from new financial players, project developers may face fewer challenges in securing project finance at earlier stages of carbon project development. The Abatable team observes carbon streaming, investment funds and corporate trading desks moving earlier in the development project lifecycle, taking an increasing level of carbon delivery risk and verification risk. In exchange, they expect a higher, “equity-like” level of investment return. Financial intermediaries and environmental traders are likely to see their roles reduced as some corporates react to the shortage in supply of carbon credits in the market by securing long-term agreements directly from carbon funds or developers. Some corporates are starting to get more sophisticated in their carbon procurement approaches and are now exploring locking in supply at pre-agreed prices through forward off-take agreements. Others are looking to participate in early stage carbon development investments as a way to secure all future supply of carbon credits generated over the lifetime of the investment, as well as improve the additionality narrative by providing catalytic capital to get a project started and scaled from inception.

This article is also published by Abatable as part of an ongoing series of reports and analysis of the voluntary carbon market and its stakeholders. Energy Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.