· 7 min read

Reducing dependence on Russian gas is the order of the day. Thus, import LNG terminals will soon play an important role in Germany. The idea of building import terminals for liquefied natural gas (LNG) on the German coast is already several years old. However, political support for the construction of the planned facilities in Brunsbüttel, Wilhelmshaven and Stade was limited. Moreover, investment decisions by economic actors also dragged on for a long time, were put on hold or planning was very slow.

Now everything has to happen very quickly at once. For this reason, this article answers to the most important questions:

- Which LNG terminals are planned?

- When can the terminals go into operation?

- How high will the import capacities be?

- And what do they mean for climate protection?

Why is LNG necessary?

The invasion of Ukraine by Russia made it clear to all actors in Germany: Diversification of gas imports is urgently needed. Moreover, the great dependence on Russian gas can severely impair Germany’s security of supply in the event of a supply stoppage.

Russia stopped gas supplies to Poland and Bulgaria at the end of April. Our March 2022 analysis examines the German and EU-wide supply situation under different supply scenarios of gas from Russia. Thus, a supply gap can only be closed in the short term by reducing consumption. Mid term, new regasification capacities for liquid natural gas are needed in Europe, especially for Germany. Hence, Europe might become independent of Russian gas supplies.

Germany currently consumes about 90 billion cubic meters of natural gas per year. More than 50 per cent still came from Russia via pipelines in 2020. Moreover, the EU was still heavily dependent on Russian gas in 2021, which accounted for 45 per cent of imports. However, almost 15 per cent of EU imports last year were provided by LNG from the USA or Qatar, for example, as Figure 1 shows. A further 10 billion cubic metres came via the Mediterranean from Algeria (sources: EU Commission and Reuters).

Figure 1: Shares of natural gas import countries in Germany and the EU (source: Energy Brainpool, 2022)

To reduce German dependence, LNG is to come to Germany in the very short term via floating terminals, so-called FSRUs (Floating Storage and Regasification Units). These terminals receive the liquid natural gas cooled to about -163 degrees Celsius from an LNG tanker. Then, the still-liquid natural gas is regasified and brought ashore via a connecting pipeline. There it can be fed into the gas grid. Moreover, plans for the onshore major LNG import terminals will also be reactivated.

What are the current plans?

First of all, the onshore LNG import facilities have to be built before imports can start. Under normal conditions, a timeframe of five or more years is realistic for planning, permitting and construction. On the one hand, for the planned LNG import terminals in Brunsbüttel and Stade, commissioning is likely to take place earliest in 2024 or later, even with strong political support. The terminal in Wilhelmshaven, on the other hand, could regasify imported LNG from the US or Qatar and feed it into the German gas grid as early as winter 2023/2024.

Nevertheless, a number of FSRUs are to be at sea off the German coast sooner. So far, Germany has reserved four special ships on the world market. Moreover, the first liquefied natural gas is to be landed from a floating terminal off Wilhelmshaven as early as the turn of the year 2022/2023. In total, it can replace up to 20 percent of gas imports from Russia. Thus, the first pile driving – which is equivalent to a groundbreaking ceremony, only at sea – already took place on the fifth of May. On top of that, another ship is planned for stationing in Brunsbüttel in early 2023 (source: E&M, Tagesspiegel).

What about midterm?

According to plans of the Federal Government, two more floating terminals are to be rented near Stade, Rostock, Hamburg-Moorburg or Eemshaven in the Netherlands and operated for ten years. Therefore, a total of EUR 2.94 billion is available from the federal government’s budget for the procurement of the four terminals (source: BMWK und Tagesschau).

In addition, the Federal Government is currently working at full speed on an LNG Acceleration Act (BMWK background paper). It is intended to greatly accelerate the construction and operation of both floating and land-based terminals by shortening approval procedures and reducing environmental regulations. The LNG import terminals will only be allowed to be in operation until 2040. What is more, the plant operators can submit a permit application to convert the plants to the use of green hydrogen or other green derivatives by 2035. Then, the terminals can continue to operate after 2040 (source: DUH).

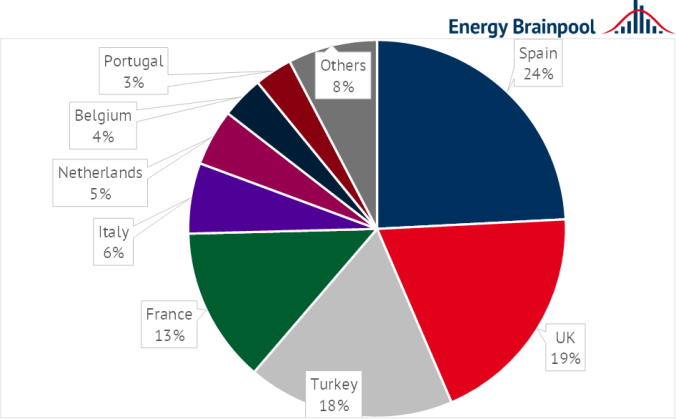

Capacities of already existing terminals in Europe

LNG import terminals have existed in many European countries for a number of years, 37 in total, 26 of which are located in EU member states. Between 20 and 30 more import terminals are currently being planned. The capacity of the continent’s existing regasification terminals is just under 250 billion cubic meters per year (source: Chemie Technik).

Capacities are particularly high in Spain, with 60 bcm, as the Iberian Peninsula is only very partially connected to the gas network of Central Europe. However, the UK, Turkey and France also have significant LNG import capacities as Figure 3 makes clear. Countries such as Lithuania and Poland each have terminals of only four and five billion cubic meters, respectively, but are able to source much of their gas requirements through them.

What capacities should the terminals in Germany have?

The planned terminals in Germany are expected to have considerable capacity. The four floating LNG terminals are to be gradually expanded to a capacity of 33 billion cubic meters per year by summer 2024. This is based on the BMWK in its second energy security progress report. By winter 2022/2023, it could already be possible to obtain 7.5 billion cubic meters of LNG for the German market.

With the completion of the terminals in Brunsbüttel and Wilhelmshaven, between 45 and 50 billion cubic meters of LNG could be supplied to Germany from 2026. Each has around 8 billion cubic meters of regasification capacity. This would catapult Germany into second or third place among Europe’s largest LNG importers. The potential imports would then also be roughly equivalent to the import of natural gas from Russia in recent years. Dependency on Russian natural gas could be reduced to just 10 percent from as early as 2024 through further energy efficiency and conservation measures (source: BMWK).

Diversification with a long-term perspective

However, the chartering of the FSRUs, as well as the construction of the new LNG terminals, also raises questions. New fossil fuel infrastructure is being developed and partly financed by the German government. This could create overcapacity and cement existing energy consumption patterns. Moreover, the triangle of objectives between sustainability, security of supply and economic efficiency is important. Especially, in an extreme situation of a war this has be taken into account .

Therefore, according to the Federal Ministry of Economic Affairs and Climate Protection, infrastructures and land-based terminals in Germany should be planned and built in a way that they are suitable for the import of green hydrogen or other derivatives such as green ammonia (source: BMWK). Uniper’s planned terminal in Wilhelmshaven is either to be built with a landing terminal for green ammonia or at least to allow conversion to green imported products (source: Recharge). Similarly, RWE and Gasunie plan to build the Brunsbüttel terminal a special way. Thus, the terminal can be easily converted to green ammonia imports afterwards. Simultaneously, a terminal for green ammonia is already to be built here next to the LNG import terminal. Green hydrogen can then be produced from the green ammonia in a further process step (source: RWE).

What does this mean for climate protection?

Germany will continue to be dependent on energy imports from abroad in the future. For instance, green ammonia or hydrogen will have to be imported from other countries. Especially for the decarbonization of industrial processes and parts of the transport sector. The war in Ukraine has thrown old certainties overboard. The shift away from Russian gas can be reduced in the medium term through LNG import terminals. However, the expansion of these infrastructures must also be designed to achieve medium- and long-term climate targets.

This article is also published by Energy BrainBlog. Illuminem Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.