Closing the clean investment gap

· 7 min read

With the passage of the Inflation Reduction Act in the US, and ‘Fit for 55‘ in Europe, it is easy to feel like we are finally turning the corner on climate change.

With sound policy frameworks in place, and economic momentum at our backs, the transition feels all but inevitable, even if the pace required does not. That is why many now assume that the finance and investment required will automatically flow. Unfortunately, nothing could be further from the truth.

Today, clean energy investment is only marginally increasing, while the financial system is locked into autopilot with hundreds of billions in new investments in fossil fuel infrastructure every year. That inertia, coupled with the impacts of a rising interest rate environment, threaten a dangerous slowdown of the clean energy revolution – unless we act.

To build a clean energy future free from dangerous climate impacts, the International Energy Agency (IEA) estimates the world must invest $4.6trn in new clean energy every year by 2030. That money is needed for more than 1,000GW of new solar and wind to clean up the power sector alongside heat pumps, EVs and just about every clean technology under the sun.

However, despite nearly every financial institution on Earth having a net-zero policy (283 to be exact), the world is currently investing less than one-third that amount (~$1.3trn) and its growth rate is marginal at best. That leaves us $3trn short and counting, which is quickly becoming a concern for leaders worldwide.

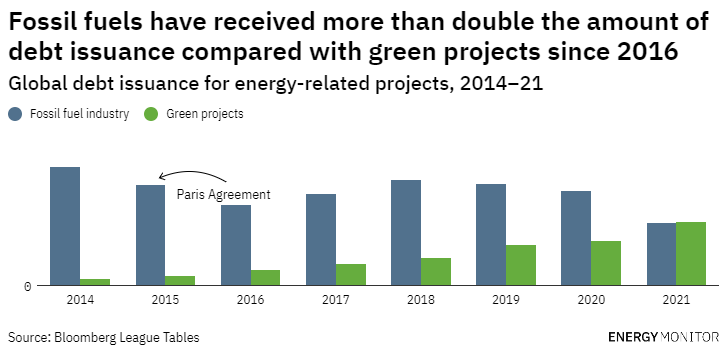

Instead, financial institutions have been pouring gasoline onto the proverbial fire with billions in investment in fossil fuels since the Paris Agreement. That reckless spending has led to a ratio of clean to dirty fossil fuel investment that has never surpassed 1:1, according to Bloomberg estimates. To meet the clean energy investment needs of nearly every climate-safe scenario, that ratio has to jump to 4:1 by 2030 – and rise to as much as 10:1 by the middle of the century.

Shifting those lending ratios is critical because finance is a leading indicator of change. Investment decisions today build the world of tomorrow. Given nearly every climate scenario frontloads investment, net zero by 2050 is the wrong mental model for the finance industry. Financial institutions need to be investing on a ten-year time horizon to 2030 – or they are investing in failure.

It doesn’t have to be this way.

While $4trn may seem like a lot of money, the reality is that global annual gross capital formation (investment, in other words) is nearly $22trn, the majority of which is determined by corporate capital expenditure plans. We have more than enough money than we require. It is not an intractable problem requiring a magic money tree. Instead, we need to aggressively shake the system we have to produce a different outcome.

At the same time, we can’t understate the challenge. We need three times the amount of all energy investment today just for clean energy – and we need to frontload it over the next decade. The sheer scale and speed of investment required should force serious climate hawks to question the notion that just getting the policy right will ensure the necessary scale of investment will flow. Instead, finance policy is all but ignored by the mainstream climate community under the misguided notion that financial markets behave rationally.

However, even if markets are behaving rationally (which at times is a big if), everything from higher transaction costs driven by distributed generation, currency risks for foreign investors, substantially higher interest rates faced by project developers in emerging markets, or the very real political economy decisions made by lenders every day about who they choose to lend to and why, conspire to stem the flow of money into the clean economy. Given the existential nature of the challenge, we would be wise to not leave the market solely to its own devices.

And then there is our collective response to inflation.

Just as Western countries are learning to love industrial policy and public investment again, they are actively undermining their new climate policies with their approach to combatting inflation. Unlike fossil fuels, clean energy is disproportionately impacted by rising interest rates. The total cost needs to effectively be paid for, and financed, up-front. For instance, as interest rates rise, the levelised cost of energy from a gas power plant might rise by 8%, but the equivalent cost of a clean energy project – a solar or wind installation – could rise as much as 47% – and that is in the rich world.

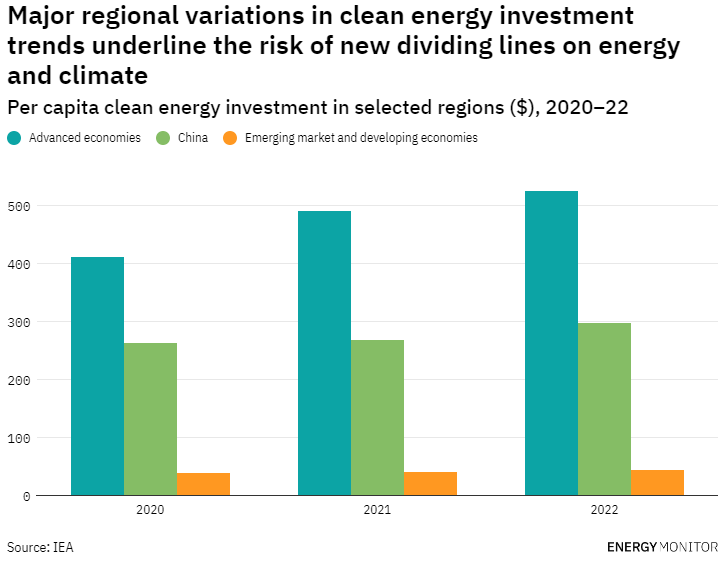

Global financial institutions have all but excluded poor countries from the investment required to develop their economies with clean energy. That is reflected in part by the exorbitant cost of capital in emerging economies, which can be as much as twice what it is in the OECD. It is reflected even more by the fact that money hardly flows at all in some parts of the world. According to the IEA, total clean energy investment per capita in emerging economies is less than 15% of their rich world counterparts. If future emissions flows will be determined by what we build in emerging Asia and sub-Saharan Africa, we are investing in disaster.

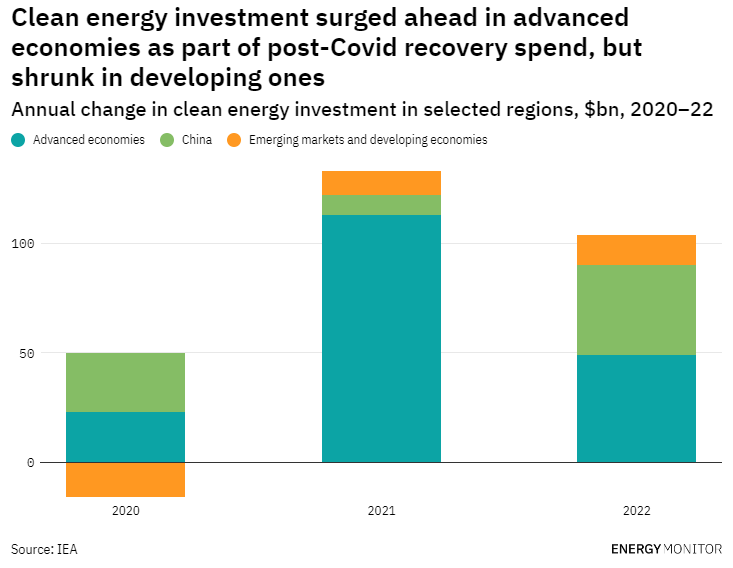

However, those figures are from the low-interest rate world we are now leaving. In that world, financiers hungry for yield had been sending money and investment into emerging markets, albeit at relatively exorbitant rates, but at least the money was flowing. Now there is a financial exodus as money and investment retreat to safer investments in the Western world where they can generate adequate returns with much less risk. If we thought the situation was bad, it is about to get much worse.

All of this means we need to intervene because markets left to their own devices cannot, and will not, respond at the speed and scale required.

The problem with what passes for our policy response – a near maniacal obsession with de-risking private capital – is that it is not working. We are routinely told that public dollars should leverage 10–20 times their amount in private markets, but according to the World Resources Institute, for every dollar multilateral lenders invested in climate finance in 2020, they reported just $0.29 in co-financing from private sources. Worse, the total amount they are providing has slowed to a trickle this year. Rather than getting bang for our international public buck, we are getting a whimper.

We must make better use of scarce international public dollars to close the investment gap in emerging markets where money is needed most, because while the track record is shockingly bad, it is true that public dollars used wisely can unlock a lot of private investment. However, for that to happen, we must reform the moribund institutions charged with deploying these dollars to take on more risk, even if it threatens their AAA credit rating. If they can’t or won’t, donor nations must fire multilateral development bank leaders holding us back and install new ones who are committed to deploying 100% of their portfolios to clean energy while leaning into riskier deals and more innovative financing structures.

It is not just emerging markets that need an intervention, however. It would be dangerously naïve to believe Western countries are on track without intervention. Central bankers and treasuries the world over must recognise that the impact of rising interest rates is not neutral. It favours fossil fuels and is therefore an inherent subsidy. In order to align their operations with the clear public policy emerging from the US to the EU, they should heed growing calls to offer lower interest rates for clean energy. There are versions of targeted clean lending programmes like the Section 1706 programme at the Department of Energy, which might be the most powerful clean finance policy the Biden administration has at its disposal.

However, it is not just about favourable interest rates. We have lived through waves of chaotic market disruption that have seen incumbent fossil fuel producers come time and again to the government trough for bailouts. Public financiers and governments have handed over money without ever taking a clean energy transition pound of flesh. That must change. Whether it is the nationalisation of Uniper in Europe or emergency bond – and eventually equity – buying from the Federal Reserve, not another dollar should touch a corporate balance sheet that doesn’t come without ownership strings attached.

Ultimately, none of these are silver bullets to close the clean investment gap, but taken as the beginning of a collective alternative to begging the private sector to invest through incompetent public institutions, they are preferable. If we want the clean energy future promised by the Paris Agreement, the financial system needs an intervention today.

This article is also published by Energy Monitor. Illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Oil & Gas · Energy

Filip Koprčina

Energy Transition · Sustainable Investment

Jonathan Lishawa

AI · Energy

Financial Times

Power & Utilities · Power Grid

Hydrogen Insight

Hydropower · Energy

Euronews

Power Grid · Power & Utilities