Carbon removal, co-products, and system boundaries

· 19 min read

Some carbon dioxide removal systems produce valuable products in addition to removing carbon. This creates ambiguity about how to allocate the overall costs and greenhouse gas emissions of the integrated process to the removed carbon. There are existing financial additionality principles from the carbon offset market and impact allocation methods from the practice of life cycle assessment that can provide useful guidance. Some of this guidance has already found its way into carbon removal standards. I explore this here and suggest potential use cases for financially non-additional carbon removal including insetting and helping society achieve a robust state of net-negative emissions after net zero.

Multiple carbon dioxide removal (CDR) systems generate products—often referred to as co-products or by-products—in addition to removal of carbon dioxide from the atmosphere. Below are some common examples:

Biomass pyrolysis processes that produce carbon-removing biochar can also generate hydrogen, syngas, and bio-oil.

Some direct air capture (DAC) processes, such as the one being deployed by Avnos, capture water from the feed air in addition to carbon dioxide.

Bioenergy with carbon capture and storage (BECCS) processes produce electricity and/or heat in addition to sequestered carbon dioxide.

Certain carbon utilization processes produce long-lived products like carbon black, certain kinds of plastics, or graphite.

Some CDR processes like those being deployed by Parallel Carbon and Equatic involve co-production of green hydrogen.

Some mineralization-based carbon removal processes produce aggregates or critical metals while also removing carbon.

CDR activities that involve forestry, soils, mangroves, and seaweed can offer ecosystem services in addition to usually short-duration carbon removal.

There are other instances where carbon removal operations could be appended to existing industrial operations. Once coupled, the full systems produce both carbon removal and other products, making them functionally equivalent to stand-alone CDR processes that generate co-products. Below are some examples of how this can occur:

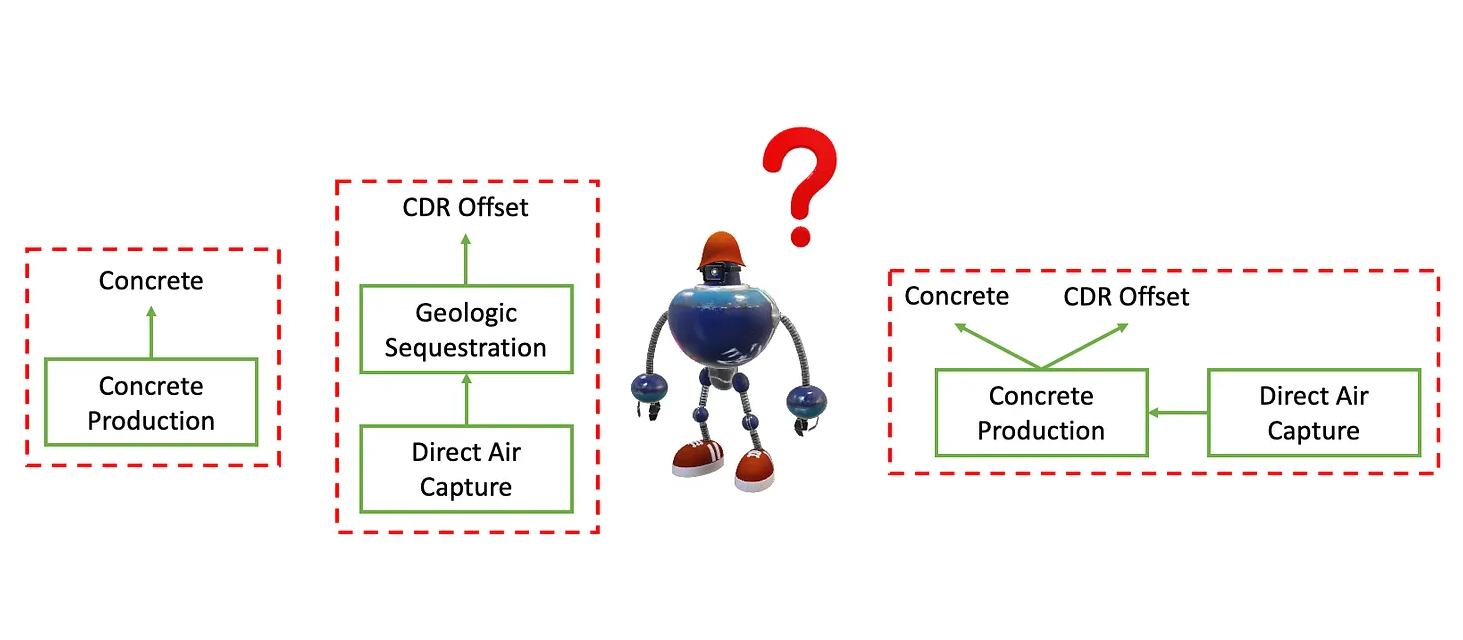

CO2 captured via DAC can be mixed into concrete as suggested in the image above. Overall, this process produces long-lasting carbon removal in the concrete in addition to the concrete itself. Heirloom is using this method for early storage of CO2 captured via DAC.

CO2 streams produced by biogas facilities contain biogenic carbon that was initially captured from the atmosphere through a biological means. If this CO2 is reasonably sequestered, the overall process can remove carbon while also producing biomethane, heat, electricity, or other products generated by the facilities. This principle also applies to CO2 produced during fermentation at ethanol facilities.

Related to the example of mineralization-based CDR, CDR processes involving mine tailings may “bolt on” to active mines. Related technologies may utilize industrial alkaline wastes, such as steel slag, for carbon removal.

Two key issues arise when CDR processes have co-products.

The first is understanding the net economic cost or benefit of the coupled operation and how this interacts with the ability to price and sell removal offsets. Usually, co-product sales will only counteract system costs by a small margin. In some cases, however, it could be possible that the co-products from new CDR systems generate revenues or savings that are higher than system costs, leading to the sale of carbon removal offsets not being strictly required for the project to move forward on an economic basis. Such a situation could lead to a lack of financial additionality, which is a commonly required feature of carbon offsets as discussed below. This concept is complicated further when there are multiple parties owning different parts of the process—which can occur when CDR systems are appended to existing operations—and when a project could just become financially additional with carbon removal offset prices lower than prevailing market rates.

The second key issue involves determining the right approach to emissions allocation and establishing proper system/activity boundaries for the life cycle assessment (LCA). All CDR processes generate greenhouse gas (GHG) emissions through their operations and supply chains that must be offset by some amount of the processes’ removal to mint removal offsets for sale. For CDR processes with co-products, it is not always apparent how to allocate emissions among generated carbon removals and co-products, and this determination could have significant impacts on the system’s carbon removal efficiency and therefore minimum removal selling prices or even the ability to sell carbon removal offsets. There is also debate surrounding whether a CDR process that appends to an existing industrial operation but does not completely offset the facility’s current emissions should be able to carve out removals for external sale.

These considerations are inconsequential for stand-alone CDR systems or when there are negligible volumes or values of co-products. However, for CDR systems with significant co-product generation, working through these issues is critical.

If there are firm market rates for carbon removal offsets and co-products, then cost allocation can be irrelevant. For example, if a CDR system were to produce one ton of green hydrogen for each net ton of carbon removal generated via direct air capture and geologic sequestration, then the revenue from the sale of each pair might be something like $3,800 if prices are fixed by the market at $3,000/t for the hydrogen and $800/t for the DAC offset. Whether the company internally allocates more of the combined system cost to one product or the other will not affect the profitability of the overall enterprise.

A core issue arises when the revenue from the co-product(s) could lead to profitability without the use of carbon finance, which in this case means the sale of carbon removal offsets. This could lead to a lack of financial additionality. The concept of additionality broadly derives from the Core Carbon Principles published by the Integrity Council for the Voluntary Carbon Market (ICVCM) that proclaim, “The greenhouse gas (GHG) emission reductions or removals from the mitigation activity shall be additional, i.e., they would not have occurred in the absence of the incentive created by carbon credit revenues.”

To some, this stipulation may seem nit-picky. Why should it matter if a removal would have occurred anyway if there is still carbon being removed from the atmosphere and there is a buyer willing to pay for it? One answer is that there would be an opportunity cost of such a financially non-additional removal transaction. If a CDR process with co-products is profitable without the sale of removal offsets—which could be the case if the internal rate of return of the project without carbon finance is well above a reasonable average cost of capital for a project of that risk level—it is likely to proceed on an economic basis regardless of the sale of removals. Therefore, any funds that could be spent on removals for such a process would be better spent on a financially additional process that would not have occurred without those revenues as this generates more removal overall.

Said in another way, removals from already-profitable processes are “locked in” and are likely to occur anyway, so offset buyers hoping to make an incremental impact to compensate for their own emissions should fund processes that were not going to occur anyway. This logic could apply to tax credits as well. For example, if there were a DAC process costing only $100/t that could sustainably take advantage of 45Q in the U.S. at $180/t, then it is likely that such a project would not be financially additional while receiving the tax credit.

From a market perspective, allowing the sale of financially non-additional offsets could also lead to distortions in the removal offset market. Projects that are profitable without removal sales could afford to sell removal offsets for exceptionally low prices to undercut other sellers, which could lead to a bifurcation of removal prices. If buyers were to flock toward the cheap, non-additional, but still durable removal offsets, then it could deprive other important CDR pathways of much-needed early funds, ultimately limiting the scalability of the entire industry.

Other than the general requirement for additionality set by the ICVCM, this issue has already received coverage in existing carbon removal verification protocols. Section 2.5.3.1 of Isometric’s general standard notes that an evaluation of a CDR project’s full financials including subsidies and tax credits with and without carbon finance is required to prove financial additionality and therefore mint offsets. Section 6.4 of Isometric’s DAC-specific protocol specifically states that financial additionality would be negatively impacted or even eliminated by the “sale of co-products that make the business viable without carbon finance.”

Sylvera has argued that additionality exists on a spectrum and that revenues from co-products can reduce the additionality of CDR offsets. Puro’s Biochar Methodology states, “The CO2 Removal Supplier shall be able to demonstrate additionality, meaning that the project must convincingly demonstrate that the CO2 removals are a result of carbon finance” while also including a review of project financials to assess this. Similar financial additionality requirements are found in Puro’s carbonated materials and terrestrial biomass storage methodologies.

Buyers could of course still choose to engage in private transactions with financially non-additional offset sellers, but CDR protocols appear to be converging on financial additionality as a requirement for now.

The requirement for financial additionality could potentially lead to unwanted outcomes. One key argument against financial additionality is that it punishes processes that are more economically competitive and could lead them to artificially make their processes less efficient or more costly to then qualify for removal offset sales. Protocol developers or verifiers may not always be able to detect or prevent this.

Separately, there are issues related to the threshold at which a removal becomes financially additional. What if a project is not profitable with co-products alone but only requires removal revenues of $1/t CO2 to become profitable? Should the protocol developer or verifier then force the project to sell offsets for only $1/t to not deprive financially additional removal methods of more funds? If not, is there a different threshold, or is this a binary decision? One would hope such cases would be rare, but they might not be. Technology developers, protocol developers, verifiers, investors, and buyers will need to make reasonable judgment calls here to avoid unintended consequences, mitigate rent-seeking and duplicitous behavior, and ensure the healthy growth of the CDR market.

Regardless of where the industry eventually converges on this issue, financially non-additional processes are still worth exploring and scaling up. If they are profitable and help mitigate climate change or accomplish some other societal objective, this is a positive development. Additionality requirements are also primarily related to the sale of removal offsets to external parties. Financially non-additional removals could still potentially be used for insetting, which involves applying them against the supply chain of their co-product(s). In a process that produces removals and green hydrogen, for example, financially non-additional removals could be counted against the process emissions involved with manufacturing the green hydrogen or even the downstream emissions in the supply chain where the hydrogen is used. This would essentially allow the removals to be used as negative scope 3 emissions.

Relatedly, sale of removal offsets based on production of CO2-derived plastics is challenging due to the difficulty of monitoring the fate of stored carbon for widely dispersed materials. However, the use of captured CO2 in these pathways still can provide some benefit over petroleum-based plastics regardless of end-of-life treatment. If the CO2-utilizing plastic does not break down, then there may be some amount of removal from the use of atmospheric or biogenic CO2 locked in the material, but if it does, then it would only be returning biogenic or atmospheric CO2 to the atmosphere rather than fossil CO2. In either case, there is a benefit, either emissions removal or reduction, that can be quantified based on how much atmospheric or biogenic CO2 is utilized in the material. Applying an insetting-based credit to the overall life cycle emissions of that plastic determined using the amount of CO2 utilization in the material would be a more responsible and manageable approach than trying to sell difficult-to-verify removal-based offsets to third parties.

Another potential use case for financially non-additional removals is helping society eventually address overshoot and abate legacy emissions after we hit net zero. While some literature investigates the allocation of responsibility for addressing past emissions, putting such results into practice may be politically onerous, especially when considering intergenerational and international equity issues. Financially non-additional removals that occur without anyone explicitly paying for them could play a vital role in reducing the need for the allocation of responsibility of past emissions to specific parties and allowing for more negative emissions after society reaches net zero. A substantial amount of such removals could be a key aspect of society’s journey toward climate restoration.

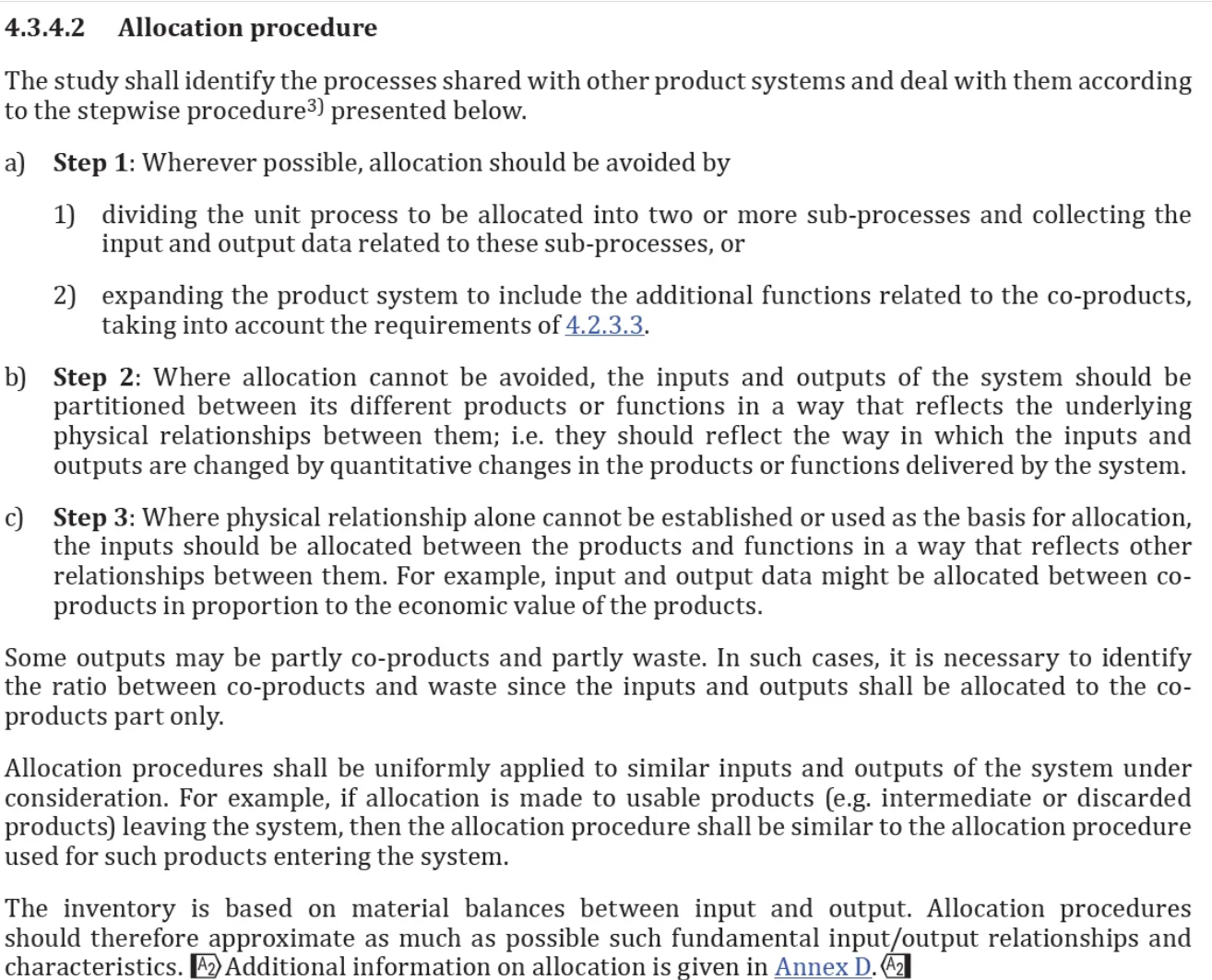

Emissions allocation can be performed according to the impact allocation hierarchy described in section 4.3.4.2 of ISO 14044, shown below.

ISO 14044

This hierarchy first recommends that emissions from multi-functional product systems are divided among co-products cleanly when it is possible to separate out dedicated sub-processes.

If this is not possible, then the total emissions from producing the co-products separately can be compared with the emissions from producing them through an integrated process. LCA scholars refer to this as “system boundary expansion” as it involves expanding the system boundary of the assessment to cover multiple processes of interest including both the conventional production pathways for all co-products and the usually new multi-functional process being evaluated.

A variation on this approach involves subtracting the emissions from conventional production of one of the co-products from the total emissions of the integrated system to attain an isolated value. This is known as system boundary expansion with substitution. For example, assume:

A system produces 1 ton of product A and 2 tons of product B;

In doing so, it emits 10 tons of CO2; and

Conventional production of product B emits 3 tons of CO2 per ton.

In this case, ((10 t CO2) − (2 t prod. B) * (3 t CO2/t prod. B)) / (1 t prod. A) = (4 t CO2/t prod. A) would be allocated to product A. Users of this method must exercise caution as it can yield emissions results below zero that are not indicative of carbon removal but rather emissions reduction relative to a baseline.

If these approaches are unworkable for one reason or another, impacts can be allocated based on physical relationships, such as mass or energy content, or non-physical relationships, such as economic value.

These solutions for addressing multifunctional product systems still involve some uncertainty and debate, which potentially provides those in the CDR industry with some leeway to set standards in the most productive ways possible. However, these impact allocation methods overall are common and sensible, and it is not clear that CDR systems with co-products should be an exception and use a radically different approach.

Imagine a “bolt-on” system that simply injects CO2 captured via DAC into a concrete mixer for permanent sequestration via carbonation but that does not lead to any other changes in the concrete’s formulation or production. This system could be described by the image at the top of this post. The first allocation approach involving subdivision could be applied in this case. All emissions from the concrete system would be allocated to produced concrete, and all emissions from the DAC system up through the pipe added to inject the captured CO2 into the mixer would be allocated to the removed carbon.

Alternatively, imagine a system that produces both green hydrogen and CO2 removed via ocean-based CDR. A system boundary expansion with substitution approach could be applied. The average emissions from production of green hydrogen could be subtracted from the overall emissions of operating the system, leaving the remaining emissions to be allocated to the removal operation.

The Best Practices for Life Cycle Assessment (LCA) of Direct Air Capture with Storage (DACS) published by the U.S. Department of Energy specifically recommend adhering to the above section from ISO 14044 when assessing emissions of DAC systems with co-products. All allocation methods and calculations must always be clear and transparent to enable reviewers to evaluate the effect of different approaches and gain a more holistic understanding of the potential emissions benefits of a given process.

Puro’s Biochar Methodology contains the following guidance for emissions allocation among biochar co-products.

This protocol calls for allocation of process emissions between the biochar, which enables CDR, and its co-products if the co-products have significant economic value or represent a large share of the initial biomass energy content. Justification of the approach is required, and, presumably, Puro would recommend revision of any approaches that are deemed unreasonable. If the co-products are insignificant, then all emissions must be conservatively allocated to the CDR part of the process.

If other protocol developers adopt similar emissions allocation approaches, then CDR systems with co-products would not necessarily have to remove more carbon dioxide than they generate to mint CDR offsets if most of the emissions are fairly allocated to the co-products. This may seem a bit counterintuitive, but it is the current logic that allows CDR providers like Heirloom to sell carbon removal offsets based on its partnership with CarbonCure even though the produced concrete likely emits far more than what is removed from the atmosphere. Emissions from concrete manufacturing are allocated to the produced concrete whereas Heirloom is presumably only allocating incremental capture and transportation emissions to its removal tons.

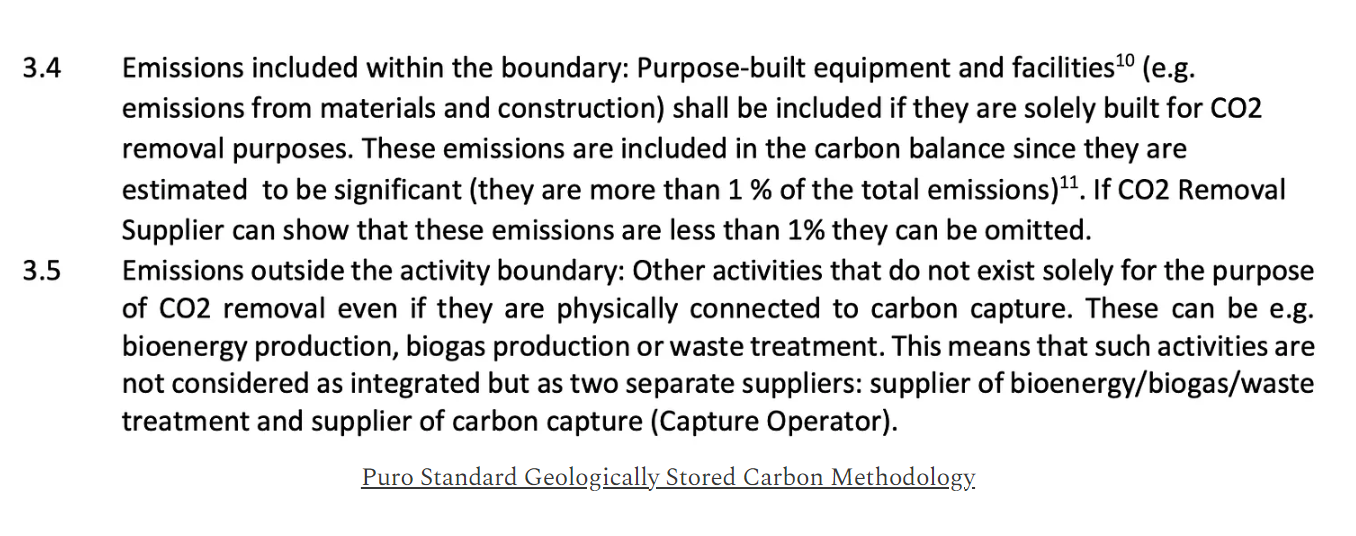

Puro also addresses LCA system boundaries in its methodology for geologically stored carbon. This guidance excludes underlying industrial operations to which CDR systems are applied from the assessed activity boundary, which is essentially system boundary expansion with substitution, as described in the below excerpt.

In this standard, Puro also recommends compliance with ISO LCA principles, which would allow for emissions allocation between CDR and co-products as described above. As with financial additionality, there currently appears to be some degree of consensus on the proper approach.

In a fairly recent commentary, CarbonPlan contends that capture and sequestration of biogenic CO2 captured from ethanol facilities would not be carbon removal as the overall operation would not be carbon negative when taking the ethanol facilities’ fossil emissions into account. The authors argue this is the case as “carbon storage is contingent upon the continued production of ethanol,” which currently would emit more than what is sequestered from the operation. The upshot of this argument is that in cases where CDR systems are appended to existing, emissions-heavy operations, any generated removals should be applied against the emissions from corresponding outputs—which in this case would be ethanol—rather than sold for external use.

This argument and resulting recommendations could be inconsistent with existing emissions allocation approaches and potentially severely hamper the development of several important types of carbon removal. If widely adopted, this logic would inhibit most CDR pathways that make use of wastes, including waste heat and waste biomass, from selling removal offsets, as these wastes are generally produced by facilities that emit far more than corresponding CDR operations can remove. There are reasonable concerns about how such systems would be compatible with a net-zero society if they are always emitting more than they are removing, but these underlying processes are likely to continue regardless of CDR and will likely be subject to the same expectation and pressure to decarbonize as the rest of society.

This logic could be especially concerning if extended to entire industries necessary for CDR to operate. DAC “is contingent upon the continued production” of steel, for instance, but it would be completely unreasonable to expect that DAC must collectively remove more than the steel industry generates overall to generate true removals for sale. This could be a straw man, but it does seem to be the case that attempts to expand the system boundary beyond any incremental operations required for removal specifically could result in such an absurd conclusion. If we start expanding the system boundary beyond the CDR operation itself then it could become unclear where to stop, which could undermine wide swathes of the fledgling market.

Related to system boundaries, there are legitimate concerns about leakage, also known as emissions displacement. This could occur if a removal operation increases emissions outside of its own customary system boundary. This concern is addressed by Isometric’s general standard, which notes, “Projects should demonstrate a robust assessment of potential increases in GHG emissions outside the defined project boundary that occurs as a result of the Project activity. Where the potential for such Leakage is identified, it must be quantified and deducted from the CO2 Removals in accordance with the relevant Protocol.”

A common example of leakage would be increased demand for dirty electricity if the energy requirements from a new CDR facility are not met with additional and temporally and geographically matched low-carbon power. Another potential example could be an increased need for cement in carbonated concrete mixes. While this may not necessarily be common or even realistic, if CDR were to induce a need for more high-emissions cement usage to maintain the performance level of the underlying concrete, corresponding emissions should be allocated to the marginal CDR activity and not the underlying concrete. For new, stand-alone CDR processes with co-products, a type of leakage could occur if process emissions were to be unreasonably allocated to co-products in a way that makes them more emissions intensive than their conventional counterparts.

This logic extends to the risk that CDR revenues keep emitting facilities open for longer than they would have been otherwise. If a DAC facility pays for waste heat from a coal plant that would have otherwise shuttered without those revenues, it should bear the responsibility for the continued emissions from the plant that would not have occurred otherwise. Considerations of leakage complicate net emissions impact analysis in related cases such as enhanced oil recovery using captured CO2.

Accounting for these factors is difficult and creates gray zones vulnerable to manipulation. The industry must try its best, however, to arrive at an honest accounting of true, marginal, salable removals generated from CDR activities.

Financial additionality and emissions allocation go hand-in-hand. Once a fair emissions allocation approach is applied to determine the marginal amount of carbon removal from a CDR process with co-products, financial additionality becomes the test to determine whether any removals can be minted for sale as offsets.

If the industry wants to allow CDR systems that append to existing operations, it should apply the same emissions allocation rules used by self-standing CDR systems with co-products. These systems are functionally equivalent in that they produce both CDR and a co-product; financial additionality of removals is ultimately the relevant test. It is irrelevant whether the CDR project developer owns the emitting infrastructure or not. What matters is whether emissions are allocated fairly among the CDR and the co-product and whether the CDR is financially additional or not.

To continue generating removal offsets, CDR operations will require periodic re-evaluations. These should reassess both financial additionality and co-product emissions. Isometric’s DAC protocol notes that factors such as changing co-product revenues and costs of capital could affect this determination for projects on an ongoing basis. Changing baseline emissions for co-products could also affect the emissions allocated to removal tons when using system boundary expansion. All ecosystem actors should remain aware of the risks generated by changes in these kinds of factors over time.

Ultimately, principles like financial additionality and emissions allocation are just humanmade constructs that we use to describe certain systems and incentivize certain behaviors. They, and any requirements we construct around them, are subject to change as we collectively decide on our goals and find better ways to achieve them. Creating a common understanding of these concepts and then working from this shared foundation will help us shape increasingly useful systems for managing the CDR market as it matures.

This article is also published on the author's website. illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Carbon Regulations · Carbon Market

illuminem briefings

Carbon Market · Carbon Regulations

illuminem briefings

Carbon Capture & Storage · Biodiversity

World Economic Forum

Carbon Capture & Storage · Carbon

MIT Sloan Management Review

Carbon Market · Corporate Governance

ESG News

Carbon Market · Carbon