Carbon markets: Which role does biomass play?

· 6 min read

Although compliance and voluntary carbon markets vary in scope, mechanisms, and participants, biomass occupies a unique space in both. In compliance, carbon markets such as the European Union ETS, participants are obliged to monitor and report their emissions and ultimately pay for them. Using biomass in industrial facilities can reduce financial burdens. Regulators set rules around biomass use and sustainability criteria to comply with. Nature-based solutions, including forestry and other biomass-related activities, generate a large part of voluntary carbon credits. However, these projects are under intense scrutiny due to issues regarding transparency and associated climate claims. Novel carbon removal solutions with biomass as feedstock show promising development, and renewed regulatory oversight could restore trust.

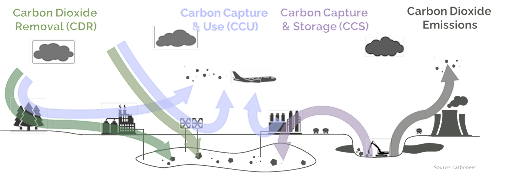

Assessing the relevance of carbon markets for biomass and vice versa requires understanding different types of emissions and how they account for them. The sources of CO2 emissions and their final sink can be categorized into four main pathways (Figure 1).

Unabated greenhouse emissions from fossil sources add emissions to the atmosphere (grey and black)

Abated emissions from fossil sources through Carbon Capture and Storage (CCS) with long-term storage might not add additional GHG emissions to the atmosphere (purple)

Negative emissions through nature-based or technological Carbon Dioxide Removal (CDR) solutions taking CO2 out of the atmosphere and storing it durably (green)

Utilisation of CO2 through Carbon Capture and Utilisation (CCU) technologies, where the ultimate source of the CO2 (atmospheric or fossil) and the final product into which the CO2-molecules have been transformed determine the climate impact (blue)

To establish these solutions' emission reduction potentials, a detailed analysis of the technological pathways, supply-chain emissions, and substitution effects is required.

Figure 1: Different pathways of CO2: fossil emission, CCS, CCU, and carbon dioxide removal. Source: carboneer

Compliance and voluntary carbon markets both incentivise gas emission reduction or carbon removal—however, each from a different angle. Compliance carbon markets aim to fulfill national or regional emission targets. By putting a price tag on emissions, they incentivise compliant actors to reduce their emissions cost-efficiently. The mechanics of voluntary markets aim at financially supporting projects that either reduce emissions or provide negative emissions through CDR. Private actors can purchase carbon credits from project developers for their corporate carbon offset or neutralisation purposes.

The EU ETS is among the largest and most mature compliance markets. Since its inception in 2005, the EU ETS has been a cornerstone of EU climate policy, covering 35-40% of the region’s emissions. Extensive industrial facilities, such as steel mills, chemical plants, cement kilns, power plants, and aviation and maritime transport operators, must monitor and report their annual emissions. For each ton of CO2-eq emitted, the compliant entity must surrender an emission allowance. The price of this allowance is determined at the market. Currently, many industrial facilities still receive free allowances. To prevent carbon leakage while phasing out this free allocation, the Carbon Border Adjustment Mechanism (CBAM) requires importers of certain goods from non-EU countries to report the embedded greenhouse gas emissions in imports and, from 2026 onwards, also to pay the same carbon price as EU-based industry. Most EU emissions from buildings and road transport are not yet subject to a carbon price. This changes with the new EU ETS 2 covering another 35-40% of the EU’s GHG emissions. Since 2024, suppliers of liquid, gaseous, or solid fuels are required to monitor and report emissions released by their fuels at the end-user. Pricing in the EU ETS 2 starts in 2027.

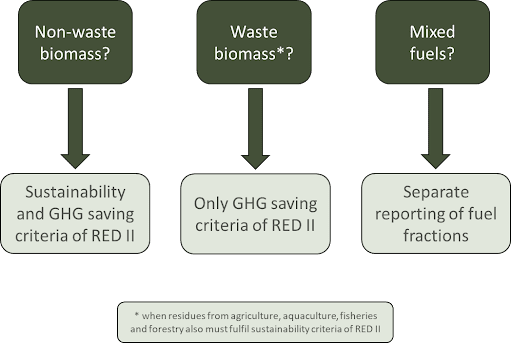

Carbon in biomass ultimately comes from the atmosphere itself. Only CO2 stored in the biomass is released back into the atmosphere when combusted. However, factors such as land-use emissions due to biomass harvesting or emissions along the value chain must be considered for a comprehensive life cycle assessment. According to current regulations, emissions from biomass and biofuels in the EU ETS 1, CBAM, and EU ETS 2 can generally be counted as zero, thus reducing the number of allowances purchased by compliant entities and reducing their costs (Figure 2). Depending on the type of biomass and its utilisation, compliance with the Renewable Energy Directive for sustainability or GHG-saving criteria needs to be achieved.

Figure 2: Criteria for biomass utilisation in the EU ETS 1. Source: carboneer

Forests, mangroves, biochar kilns and waste-to-energy plants with CCS all have in common that they are examples of biomass-based projects on the voluntary carbon market. Private entities purchase carbon credits from project developers to offset or neutralise their (hard-to-abate) emissions. These projects either reduce greenhouse gas emissions or remove CO2 from the atmosphere and must follow specific carbon standards and methodologies for project set-up and emission calculation. Third-party verification of the projects’ climate effects is needed to create trust and transparency in voluntary markets where regulatory oversight is only rudimentary.

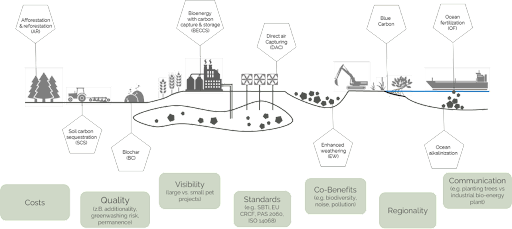

While various voluntary carbon market methodologies and carbon projects exist, biomass-based projects are ubiquitous and remarkably diverse. Many biomass voluntary market projects potentially create negative emissions (to stay within the emission targets of the Paris Agreement, estimates for the required global carbon removal capacity range from 5-10 Gt/year or 5-20% of today’s total emissions). While trees might store atmospheric carbon for decades, technological solutions, such as pyrolysis with biochar or bioenergy with CCS, remove carbon for hundreds or thousands of years. Project developers and buyers of carbon credits on the voluntary carbon market need to navigate complexities arising from cost considerations, project types and quality, and applicable methodologies and standards (Figure 3).

Figure 3: Carbon removal solutions and considerations for voluntary carbon market projects. Source: carboneer

To reduce the lack of credibility that has plagued the voluntary market and associated climate claims of credit buyers, the European Union is currently developing its own methodologies under the Carbon Removal Certification Framework. As corporates are increasingly under pressure to develop credible climate action, carbon removal solutions utilising biomass have a role to play. Several announcements of large-scale credit purchases by corporates from biochar and bioenergy with CCS project developers underscore that point.

CO2 is not CO2: The ultimate origin of the molecule matters. Compliance and voluntary carbon markets assess greenhouse gas emissions from different perspectives and objectives. Due to the vast array of biomass applications, rules on eligibility and carbon accounting in compliance markets and voluntary carbon markets differ. Biomass use in the ETS can reduce costs for industries and allow for decarbonisation at the same time. Biomass enables carbon removal solutions, but stakeholders need to navigate the murky waters of voluntary markets. Finally, interactions between the EU ETS and the voluntary carbon market might be restored against the backdrop of industrial carbon management policies, the need to scale carbon removal, and the provision of market stability in the ETS. Complexities abound when biomass meets carbon markets.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Carbon Market · Carbon

illuminem briefings

Climate Change · Effects

illuminem briefings

Effects · Climate Change

Time News

Climate Change · Adaptation

GB News

Net Zero · Public Governance

The Guardian

Pollution · Carbon