Carbon management in Germany (I/II): from zero to climate and industrial necessity

· 6 min read

This is part one of a two-part series on carbon capture, use and storage (CCUS) in Germany. You can find part two here.

In this article, we look at the implications of a climate neutral Germany in 2045 on the demand for carbon management and carbon capture use and storage (CCUS). The topic has long been neglected in public debates but experiences a recent revival. CCUS can serve the dual purpose of (i) supporting the decarbonization of industrial facilities, and (ii) supplying especially the chemical sectors with CO2 as a resource for the production of primary products.

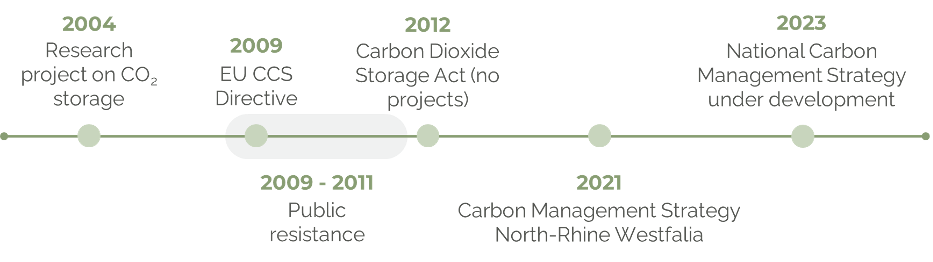

While research on large-scale underground CO2 storage started in 2004 at the Ketzin pilot site close to Berlin, industrial carbon management activities (carbon capture, utilization and storage - CCUS) are virtually absent in Germany to the present. The European Union’s Carbon Capture and Storage Directive from 2009 provided its Member States with a framework to implement corresponding national legislation. The German Carbon Dioxide Storage Act (Kohlendioxid-Speicherungsgesetz – KSpG) came into force in August 2012 (cf. figure 1) but failed to establish favourable conditions for CCUS applications.

The storage discussion at that time in Germany was closely linked to the continuation of coal power generation and met strong public resistance. The expansion of renewable energy generation was at the center of potential mitigation pathways and CCUS applications were considered risky, especially with regards to cost and safety criteria. Giving in to the general scepticism, the KSpG only allowed for applications with storage capacities below 1.3 million tons of CO2, and most states prohibited underground CO2 storage. No single storage project has been developed until the legal deadline for project submissions by the end of 2016. Currently, it is therefore not possible to store CO2 underground in Germany and only a limited amount of capture and utilization projects are operative.

Carbon management has reemerged in the political arena in Germany only recently. The northwestern industrial state of North Rhine-Westphalia published its Carbon Management Strategy in 2021 and the National Carbon Management Strategy is currently being developed by the Federal Ministry for Economic Affairs and Climate Action (BMWK). We covered the national German Carbon Management Strategy in detail in this article.

Figure 1. Timeline and relevant events on carbon management in Germany

Source: carboneer

With tightening climate targets at the EU and German levels, it is becoming increasingly clear that climate neutrality by mid-century or even 2045 will not be achieved without large-scale capture, utilization and long-term storage of CO2.

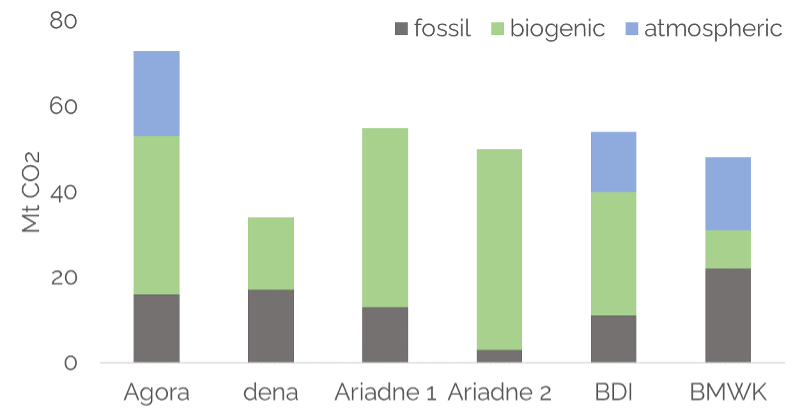

While CCUS experienced a slow uptake in German policymaking, academic research unanimously concludes that carbon management, including carbon capture, utilization and storage, as well as atmospheric carbon removal are necessary to reach climate targets. Since the electricity sector can be largely decarbonised through the expansion of renewables, the focus of carbon management in Germany lies in the industrial sector. Especially process-related emissions are hard to abate and might only be reduced through carbon capture solutions. Figure 2 shows the projections of five research projects on the sources of CO2 that will be captured in 2045, at the time when Germany seeks to achieve climate neutrality.

Figure 2. CO2-capture according to application and source in 2045 (2050 for BMWK)

Source: carboneer; data sources: Agora: Prognos, Öko-Institut, Wuppertal-Institut (2021), BDI: BCG (2021), dena: Deutsche Energie-Agentur (2021), BMWK: Fraunhofer ISI et al. (2022), Ariadne: Luderer, Kost and Sörgel (2021)

Building up the capacity to capture between 35 and 70 Mt of CO2 from different industries, or 5-10% of current German GHG emissions, requires targeted and substantial investments over the coming two decades. Investments will only materialize if determined policymaking creates an enabling investment environment and delivers clear rules and guidelines on topics such as:

While we will take a deep dive into different industrial sectors’ CCUS conditions and dynamics in upcoming articles of this series, we already want to draw your attention to some insights from our latest analysis. The technical potential across German industries predestined for CCS applications (steel, cement, lime, chemicals, waste incineration) amounts to 40-50 Mt CO2. Here we consider process-related emissions only, as other emissions can and must be decarbonised through other solutions, such as renewable energy, electrification, or green hydrogen.

On the other side, the demand for carbon in the chemical industry in Germany in 2045 is estimated to be approximately 50 Mt CO2. This already points to a new paradigm and an industrial ecosystem, where CO2 will not necessarily be sequestered and stored underground in northern Germany, under the North Sea or even being exported to Norway, Denmark, or the Netherlands. Quite the opposite, CO2 might become a scarce raw material in the industrial carbon cycle pushing the demand for CCU applications. Furthermore, the updated regulation on the EU Emission Trading System allows regulated entities to use CCUS instead of surrendering emission allowances. Undoubtedly, this option further increases the demand for CCUS applications.

Consideration of policy interactions and emerging new industrial paradigms are crucial for successful carbon management at the national and EU level. Topics that require further analysis are amongst others:

The next article in this series on carbon management in Germany will deal with the current industrial emissions, the CCS potential in those industries and cost estimates for capture, transport, and storage. In the meantime, feel free to reach out with feedback and questions, which we are happy to discuss.

This article is based on a study by carboneer for the Trade Commissioner Service of the Canadian Embassy to Germany. illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

Wil Burns

Carbon Capture & Storage · Carbon Removal

illuminem briefings

Carbon Capture & Storage · Biodiversity

illuminem briefings

Carbon Capture & Storage · Agriculture

CBC News

Carbon Capture & Storage · Public Governance

Inside Climate News

Carbon Capture & Storage · Oil & Gas

Offshore Energy

Carbon Capture & Storage · Carbon