By 2060, global production and use of plastics forecasted to triple

· 13 min read

The forecasted significant increase in worldwide production and use of plastics underscores the persistent importance of plastics in our modern economy and the challenges it poses for sustainability. Within the fossil fuel debate, the petrochemical industry managed to fly somewhat under the radar, even though in 2018, the International Energy Agency (IEA) announced that petrochemicals were set to be the largest driver of world oil demand [1]. In 2023, the IEA shared that the recent growth in global oil demand is driven by China’s petrochemical surge [2].

This article, a follow-up on “In 2014, the Plastic’s Share of Global Oil Production Was 6%. In 2050, it Will Be 20% [3],” delves into recent growth projections for plastic production, the petrochemical industry and the role of ethane crackers. the ongoing efforts to address environmental concerns, and the pivotal role of the UN Global Plastics Treaty in shaping the future of the industry. By examining these trends, we aim to provide a comprehensive overview of how the plastics landscape is expected to transform in the coming decades.

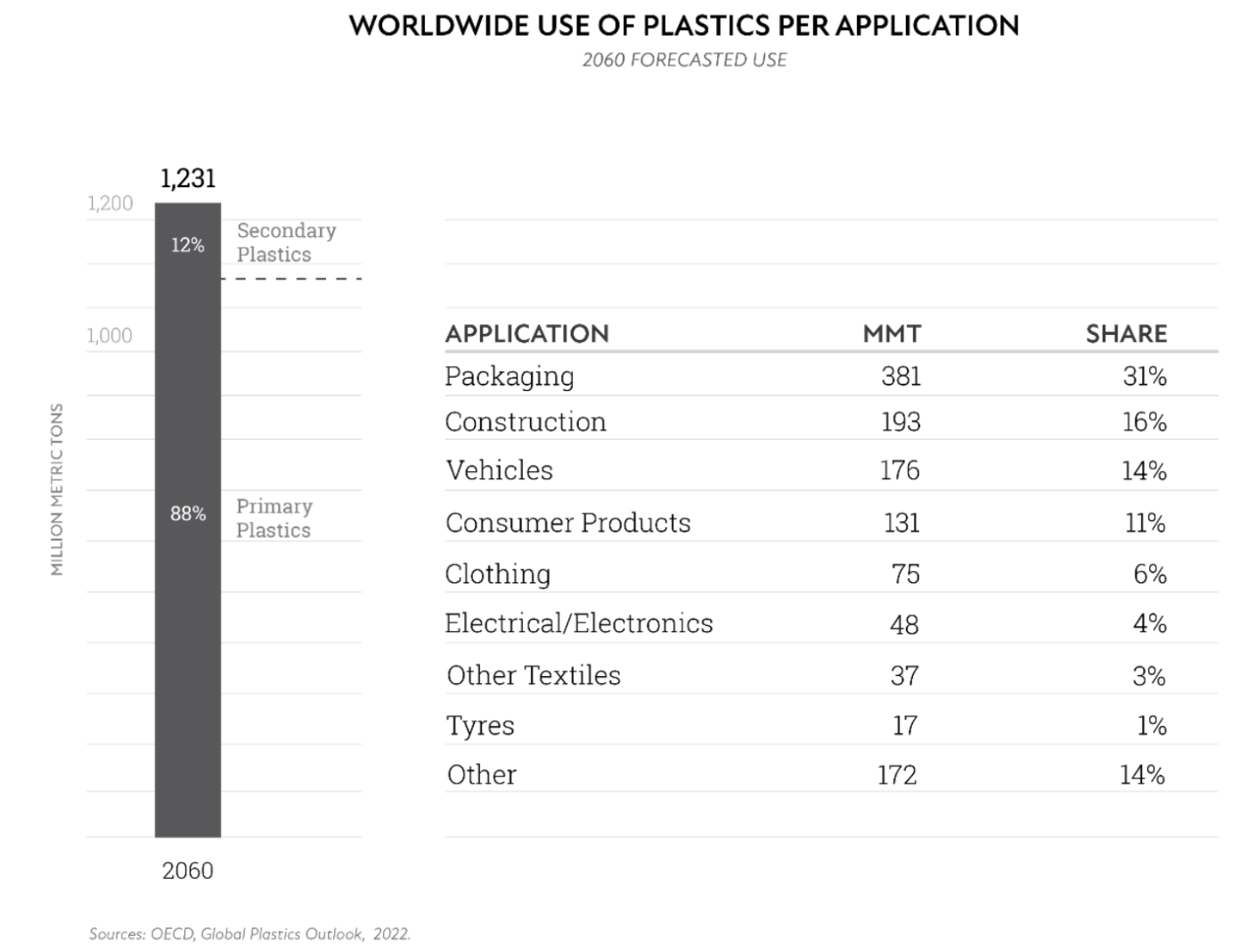

Not only does the OECD, barring new policies, expect the use of plastics to triple to 1,231 Mt by 2060, but plastic waste is also expected to increase to 1,014 Mt by 2060. By the year 2060, the use of plastics will be spread across the following applications:

Although recycled (secondary) plastics are expected to grow faster than primary plastics, they are projected to account for only 12% of total plastic production in 2060. While the OECD divides primary plastics into biobased and fossil-based, the latter's dominion (1,081 versus 6 MMT in 2060) over the former is expected to continue. In other words, more than 99% of primary plastics will still be fossil-based in 2026.

By 2060,

Three sectors will account for 60% of global plastic use: packaging, construction, and vehicles.

Sub-Saharan Africa will have seen plastic use grow by 6.5, India by 5.5, Other Asia by 3.7, and the Middle East and North Africa by 3.5.

The use of plastics will grow by a factor of 2 in OECD EU countries and the USA.

From 353 MTT in 2019 to 1,014 MTT in 2060, the projected increase in plastic waste.

Regrettably, a significant portion (50%) of plastic waste will continue to be disposed of in landfills. Although the volume of recycled plastic is expected to nearly double, it is estimated that only a fifth of all plastic waste will be recycled by 2060.

Additionally, it is expected that by 2060,

Plastic leakage will have doubled, and

The plastic build-up in aquatic environments will triple compared to 2019.

Environmental and health impacts will have severely worsened, not just because of plastic leakage and greenhouse gas emissions but also because of resource scarcity, land use, toxicity, acidification, eutrophication, ecotoxicity, resource scarcity, and land use.

Biobased plastics are expected to represent a meagre 0.5% of total plastics use.

The delegates attending COP29 are confronted with a formidable and complex challenge due to the alarming projections of plastic production and waste by 2060. The anticipated tripling of both plastic usage and waste, along with the enduring reliance on fossil-based plastics, indicates a worsening of an existing environmental crisis that necessitates urgent and resolute measures. The recycling of plastics is necessary, but more is needed. It is crucial to halt the irresponsible use of plastics. Moreover, it is essential to eradicate the extensive reliance on oil and gas for the production of plastics. However, the dismal outlook for bio-based plastics offers scant prospects for accomplishing this goal. These projections' severe environmental and health consequences emphasize the urgent need to address this issue comprehensively. Only through coordinated global efforts and innovative policy frameworks can we mitigate the growing threat of plastic pollution and protect our ecosystems and future generations.

The petrochemical industry is a segment of the chemical industry that produces chemicals by utilizing raw materials obtained from fossil fuels, including crude oil and natural gas. These chemicals, commonly referred to as petrochemicals, function as the foundation for a broad array of items integral to our daily lives, and plastics are a significant product of this industry.

The petrochemical industry occupies a crucial role in the strategies of fossil fuel corporations as they endeavour to adjust to the low-carbon economy. The demand for conventional fossil fuels, including coal, oil, and natural gas, is anticipated to experience substantial alterations due to numerous factors, such as technological advancements and policy changes. With the growing prominence of renewable energy sources and electric vehicles, leading to a reduction in the demand for conventional fossil fuels, oil and gas companies are increasingly exploring the production of petrochemicals, particularly plastics [5], as a means of maintaining profitability in a rapidly evolving energy landscape [6].

For example, the demand for coal is projected to decrease substantially by 2050. Estimates indicate a decline ranging from 25% (as per the EIA Reference) to as much as 93% (as per the Equinor Bridges and BP scenarios) compared to 2022 levels [7]. As for oil, the notion of "peak oil" is becoming more convincing, wherein oil demand reaches its zenith before subsequently decreasing. The International Energy Agency (IEA) posits that global oil demand may reach its pinnacle around 2029 or 2030 [8].

On the other hand, natural gas, a seriously misleading term that arguably contributes to greenwashing [9], is just as “fossil” as coal and oil yet hold the key components ethane and propane for the production of plastics, is considered by many as a “bridge fuel” in the transition from coal to cleaner energy sources [10]. Nonetheless, natural gas is anticipated to be the most rapidly growing fossil fuel until 2030, with global demand reaching its zenith by 2035 due to its function as a transitional fuel in the energy transformation. Following 2035, a gradual decrease in demand is predicted to persist until 2050 [10].

At the same time, the fossil fuel industry is betting on the continued demand for plastics to drive future oil and gas consumption [12] [13].

According to the latest information, the worldwide petrochemical industry comprises 3,243 active complexes, with an additional 706 complexes in the planning and announcement stages. This indicates a strong and growing demand for petrochemical products, as evidenced by the robust pipeline of new projects [14].

The global petrochemicals market size was estimated to be approximately USD 619.28 billion in 2023, and it is anticipated to grow at a compound annual growth rate (CAGR) of 7.0% from 2023 to 2030, reaching a value of around USD 1,002.45 billion by 2030 [15]. Additionally, a separate projection suggests that the market may reach USD 1,104.53 billion by 2031, growing at a CAGR of 7.28% from 2023 to 2031. [16]

The Asia-Pacific region is anticipated to exert considerable influence over the market, stimulated by swift industrialization, accommodating regulatory frameworks, and substantial capital investments in the manufacturing realm. In particular, China, as a key stakeholder, is expected to account for nearly half of the global petrochemical demand and to emerge as a leader in capacity enhancements [17][18].

North America benefits from abundant shale gas resources, which provide a cost-effective feedstock for petrochemical production. This has led to a significant expansion in production capacity. Lastly, the petrochemical market in Europe is anticipated to grow at a CAGR of 5.6% over the forecast period, supported by the recovery of the manufacturing sector and additions to oil and gas production capacity [19].

In the petrochemical sector, ethane crackers hold a vital position, primarily due to their capacity to convert ethane, a component of natural gas, into ethylene. Ethylene, as a fundamental building block, is utilized in the production of a diverse array of chemical products, including plastics, resins, and various synthetic materials. Consequently, ethane crackers are indispensable for the manufacturing process of these products.

Ethane cracking, a process known as steam cracking, decomposes ethane into ethylene by subjecting it to high temperatures, causing the molecular bonds to disintegrate and form ethylene [20]. Ethylene, the most widely produced petrochemical, serves as a precursor for various products, such as plastics (e.g., polyethylene), resins, adhesives, and synthetic fibers [21].

Constructing an ethane cracker facility entails a substantial investment, which typically ranges between $4.5 and $5 billion. These projects result in the creation of thousands of employment opportunities during the construction phase and several hundred long-term positions upon commencement of operations. For instance, the Shell ethane cracker facility in Pennsylvania is anticipated to yield nearly $3.7 billion in annual economic activity, while also offering substantial tax revenue and employment benefits to the surrounding area [22].

The operation of ethane crackers generates both economic benefits and environmental drawbacks. On the one hand, they provide employment opportunities and contribute to corporate profits. However, on the other hand, they pose environmental and health risks due to the pollutants they emit. Specifically, they emit nitrogen oxides, sulfur dioxide, volatile organic compounds, and particulate matter into the air, which contribute to ground-level ozone and pose respiratory health risks, as well as the potential for cancer [23]. Additionally, the energy-intensive nature of the steam cracking process leads to significant carbon dioxide emissions, exacerbating the issue of climate change. [24]

The availability of cheap natural gas, particularly from shale formations, has made ethane crackers economically attractive in regions like the United States. This has revitalized the petrochemical industry by providing a cost-effective feedstock, making U.S. petrochemical manufacturers globally competitive. [25]

The economic viability of plastic production has been substantially enhanced by the low cost of fracked gas. Petrochemical companies have taken advantage of the abundant and inexpensive supply of ethane to increase their profit margins, leading to substantial investments in new petrochemical plants and the expansion of existing facilities, particularly in the United States and Europe. [26][27]

The expansion of the fracking industry has not only catered to domestic markets but has also led to a substantial increase in ethane exports. The United States has emerged as a major exporter of ethane, transporting it to regions such as Europe, where it is utilized as a fuel source for plastic production. This global trade in fracked gas has played a pivotal role in the expansion of the plastics industry in regions with stringent environmental regulations, such as the European Union.

The petrochemical industry, which comprises entities involved in the production of chemicals derived from petroleum and natural gas, invests substantial resources in lobbying efforts to influence policy and regulatory decisions. These lobbying activities are focused on shaping legislation, obtaining favorable regulations, and furthering industry interests. Lobbying initiatives are directed towards regulations governing plastic production and waste management, with the intention of influencing policy decisions that may affect the industry's operations and financial performance. [28]

The oil and gas industry, encompassing petrochemical businesses, allocated a sum of $133,002,094 for lobbying endeavors in the United States during the year 2023. [29] Corporations that participated in the United Nations' global plastics treaty negotiations, such as ExxonMobil, Chevron, and Dow, invested over $85 million in lobbying and political donations during the 2022 United States election cycle. [30]

Since the adoption of the Paris Agreement in 2016, the five major oil and gas companies have collectively allocated $220 million towards lobbying efforts in the United States and the European Union. Their primary objective is to exert a considerable degree of influence on the climate policies that are formulated at the United Nations Framework Convention on Climate Change (UNFCCC). [31]

The presence of lobbyists from the fossil fuel, petrochemical, and plastics sectors at COP events has been a subject of considerable worry and examination. Notably, the count of such lobbyists attending these conferences has been growing, prompting worries about potential conflicts of interest and the impact of these industries on climate negotiations.

Given the record attendance at COP28 and the ongoing importance of climate negotiations to these industries, it is likely that the number of lobbyists from the petrochemical and plastics sectors will remain high at COP29. The figure could be similar to or even exceed the 2,456 lobbyists recorded at COP28. [32]

Given Azerbaijan's substantial dependence on fossil fuels and its intent to augment gas production, coupled with the historical pattern of increasing attendance by fossil fuel lobbyists at COP conferences, it is reasonable to anticipate a substantial number of lobbyists at COP29. Such numbers could potentially equal or surpass the record figures observed at COP28, influenced by Azerbaijan's strategic significance in the global energy market and its dedication to preserving and expanding its fossil fuel industry. [33][34]

The projections of a three-fold increase in global plastic production and utilization by 2060, as outlined in this article, present a bleak and sobering outlook for our environmental future. Despite progress in recycling and the promotion of bio-based plastics, the continued reliance on fossil-based plastics highlights a deeply ingrained and systemic inertia within the petrochemical sector. This inertia not only contributes to environmental degradation but also accentuates socio-economic disparities, particularly in regions with rapidly increasing plastic consumption rates such as Sub-Saharan Africa and India.

The current waste management practices are insufficient to handle the anticipated increase in plastic waste, a significant portion of which is destined for landfills. The expected doubling of plastic leakage and tripling of plastic accumulation in aquatic environments point to an impending ecological disaster, with far-reaching consequences for marine biodiversity and human health. Moreover, the environmental impact is further exacerbated by the toxic emissions from ethane crackers and other petrochemical facilities, which underscores the need for a radical shift in both production and consumption patterns.

The fossil fuel industry's strategic pivot towards petrochemicals and plastics, as a means of ensuring future profitability in the face of declining demand for traditional fossil fuels, demonstrates its capacity for adaptability. Nevertheless, this transition also highlights a concerning prioritization of economic gains over ecological and public health considerations. The industry's considerable lobbying efforts, aimed at influencing policy and regulatory frameworks, exemplify a deep entrenchment of vested interests that frequently impede the passage of progressive environmental legislation and undermine global efforts to combat climate change.

As the global community grapples with the complex challenges posed by climate change and resource scarcity, the projections presented herein serve as a clarion call for transformative action. Continuing with current practices is no longer a viable option. Instead, a coordinated and concerted global effort is necessary to develop innovative solutions, implement stringent regulatory measures, and establish robust international treaties, such as the UN Global Plastics Treaty. These measures should focus on significantly reducing plastic production, promoting sustainable alternatives, and ensuring comprehensive waste management systems.

One should, however, ask the following question: “What is the mathematical probability of the plastic industry becoming biobased instead of fossil-based, given that by 2060, more than 99% of plastic production will be fossil-based and no policies change?”

The answer is that the probability of biobased dominance is 0.5% (or 1 in 200). Let that sink in.

illuminem Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

[1] https://www.iea.org/news/petrochemicals-set-to-be-the-largest-driver-of-world-oil-demand-latest-iea-analysis-finds

[2] https://www.iea.org/commentaries/china-s-petrochemical-surge-is-driving-global-oil-demand-growth

[3] https://illuminem.com/illuminemvoices/in-2014-the-plastics-share-of-global-oil-production-was-6-in-2050-it-will-be-20

[4] OECD, Global Plastics Outlook, 2022

[5] https://www.cnbc.com/2022/01/29/how-the-fossil-fuel-industry-is-pushing-plastics-on-the-world-.html

[6] https://www.reuters.com/article/business/environment/rising-use-of-plastics-to-drive-oil-demand-to-2050-iea-idUSKCN1ME2QC/

[7] https://www.rff.org/publications/reports/global-energy-outlook-2024/

[8] https://www.bbc.com/future/article/20230726-an-experts-guide-to-peak-oil-and-what-it-really-means

[9] https://www.thedrum.com/news/2023/04/19/why-natural-gas-the-latest-greenwashing-term-facing-advertising-clampdown

[10] https://www.unep.org/news-and-stories/story/natural-gas-really-bridge-fuel-world-needs

[11] McKinsey & Company, Global Gas Outlook to 2050, February 26, 2021.

[12] https://earthjustice.org/feature/petrochemicals-explainer

[13] https://www.nationalgeographic.com/environment/article/europe-plastics-industry-about-to-boom-us-fracking-driving-it

[14] https://www.offshore-technology.com/data-insights/top-ten-active-petrochemical-complexes-global/

[15] https://www.grandviewresearch.com/industry-analysis/petrochemical-market

[16] https://straitsresearch.com/report/petrochemicals-market

[17] https://moderndiplomacy.eu/2024/07/01/china-and-the-gulf-arab-states-petrochemicals-partners/

[18] https://www.grandviewresearch.com/industry-analysis/petrochemical-market

[19] https://straitsresearch.com/report/petrochemicals-market

[20] https://www.jgc-indonesia.com/en/news/324/understanding-ethane-cracker-industrial-facility-to-process-ethane

[21] https://archive.alleghenyfront.org/story/frequently-asked-questions-about-ethane-crackers.html

[22] https://www.rmu.edu/about/news/rmu-study-shell-ethane-cracker-will-add-nearly-4-billion-each-year-pennsylvania-economy

[23] https://www.climaterealityproject.org/blog/ethane-cracker-plants-what-are-they

[24] https://en.wikipedia.org/wiki/Steam_cracking

[25] https://www.hosemaster.com/understanding-naphtha-ethane-cracking-processes/

[26] https://www.foodandwaterwatch.org/2023/06/22/plastic-fossil-fuels-lifecycle/

[27] https://zerowasteeurope.eu/2020/10/no-time-to-waste-plastic-production-and-fossil-gas/

[28] https://biologicaldiversity.org/w/news/press-releases/companies-lobbying-for-weak-un-plastic-treaty-spend-big-on-us-politics-2023-11-17/

[29] https://www.opensecrets.org/federal-lobbying/industries/summary?cycle=2023&id=e01

[30] https://biologicaldiversity.org/w/news/press-releases/companies-lobbying-for-weak-un-plastic-treaty-spend-big-on-us-politics-2023-11-17/

[31] https://corporateeurope.org/en/2023/06/new-figures-show-big-oil-gas-flooding-un-climate-talks-paris-agreement

[32] https://www.bbc.com/news/science-environment-67607289

[33] https://www.reuters.com/sustainability/climate-energy/cop29-climate-summit-host-azerbaijan-defends-oil-gas-investments-2024-04-26/

[34] https://minenergy.gov.az/en/statistika

illuminem briefings

Effects · Climate Change

illuminem briefings

Public Governance · Climate Change

illuminem briefings

Public Governance · Climate Change

The Economist

Nature · Environmental Sustainability

UNDP

Adaptation · Climate Change

Offshore Energy

Carbon Capture & Storage · Carbon