Assessing the state of the voluntary carbon market in 2022

· 9 min read

It has been a landmark year for carbon management. High-quality carbon reduction, utilization, and removal is more important than ever – particularly with respect to removals. In their latest Climate Change Mitigation report, the IPCC describes carbon removal as “essential” to meeting our climate goals. Meanwhile, U.S. federal support for carbon management has increased alongside corporate climate commitments. Yet there is still significant work to do. The IPCC estimates that 10 Gt of carbon removal is required annually by 2050 – today, we are at just 0.003 Gt. In considering these goalposts, it is important to standardize the monitoring of available supply and demand in carbon markets through databases like the U.C. Berkeley’s Voluntary Registry Offsets Database (VROD).

The VROD aggregates carbon management projects from the four largest voluntary offset project registries: American Carbon Registry (ACR), Climate Action Reserve (CAR), Gold Standard (GS), and Verra (VCS). Together, they total over 1.5bn tons issued across 5,000+ projects. In our inaugural 2021 Commentary on the Release of the Voluntary Registry Offsets Database, we underscored the importance of quality criteria, the need for carbon removal development, and the challenges of accurate tracking so as to avoid over-crediting. These challenges have only worsened over time with new mechanisms like blockchain-enabled retirements.

Over the past year, substantive changes to the voluntary carbon market prompted new questions about the offset market and its ability to deliver carbon reductions and removals. In assessing the new data, we find that:

In this blog post, we provide an overview of offsets and the voluntary carbon market and a summary of each of these findings regarding the state of the voluntary carbon market in 2022. For more substantive information on the findings, see our full report on the 2022 Release of the Voluntary Registry Offsets Database.

There are two overlapping carbon markets: voluntary, where individuals and entities can purchase carbon offsets by choice in support of their climate commitments; and compliance, with credits that can be used by entities that are required by national governments or regulatory bodies to account for their carbon emissions. We focus here on the voluntary carbon market.

Offsets – defined by the UN Race to Zero as “credits that reduce GHG emissions or increase GHG removals in order to compensate for GHG emissions” – are the common currency in the voluntary carbon market. Corporations or individuals most commonly use carbon credits to “offset” or “cancel out” emissions from their operations. By buying and retiring an offset ton, an offset purchaser seeks to undo the impact of a ton emitted or planned. The purpose of offsets is to avoid, reduce, or remove GHG emissions.[1] Unfortunately, these goals are not commonly met by projects in today’s voluntary carbon market.

No true regulations exist on the voluntary carbon market. In most cases, retiring parties can purchase offset tons and account for the carbon offset without oversight. Responsibility for the quality of those offsets often come from public scrutiny[2] or internal bars set on quality, such as by companies such as Microsoft or Shopify.[3] A lack of oversight in this area is why we partnered with Microsoft to develop the Criteria for High-Quality Carbon Removal and provide a broadly applicable set of benchmarks to encourage market standardization moving forwards. While new developments like new, standardized offset programs and the proposed SEC draft ruling may drive transparency, at this point in time they have not significantly improved carbon markets.

On March 21st, the U.S. Securities and Exchange Commission (SEC) approved a proposed rule[4] that would require all registrants, including foreign-based firms, to disclose in their annual financial statements the climate-related risks that:

The passage of this proposal is historic. If it is adopted, it will be the first time the SEC is requiring its registrants to report on the climate risks associated with their business operations and management.

For more on recent U.S. policy and carbon management, see the blog “U.S. Federal Support Increases for Carbon Removal.”

As carbon markets continue to mature, it is increasingly important to assess the types of carbon credits entering and retiring from the registries to determine whether the market is performing as it should. Berkeley’s Voluntary Registry Offsets Database (VROD) offers a robust database from which to draw insight.

Pure removal projects made up only 3% of all projects issuing credits over 2021 and 2022 YTD, while projects that tend to include a mix of removals and reductions represented 13%. No credits were issued in 2021 for durable removals, the only type of offset that can effectively cancel the impacts of carbon dioxide released into the atmosphere in a functional reversal of emitting carbon dioxide. Carbon storage options with high risk of reversal, while important in the short term, must operate as a bridge to longer-term storage options even if high in quality. Overall, the carbon offset market would benefit from the addition of more options with low-risk, durable storage.

![Figure 1: 2021 and Q1 2022 carbon offsetting project types, number of projects[5]](https://illuminem.b-cdn.net/articlebody/cfd9b1454f8f7fad5f00f727a575c77929035d94.png)

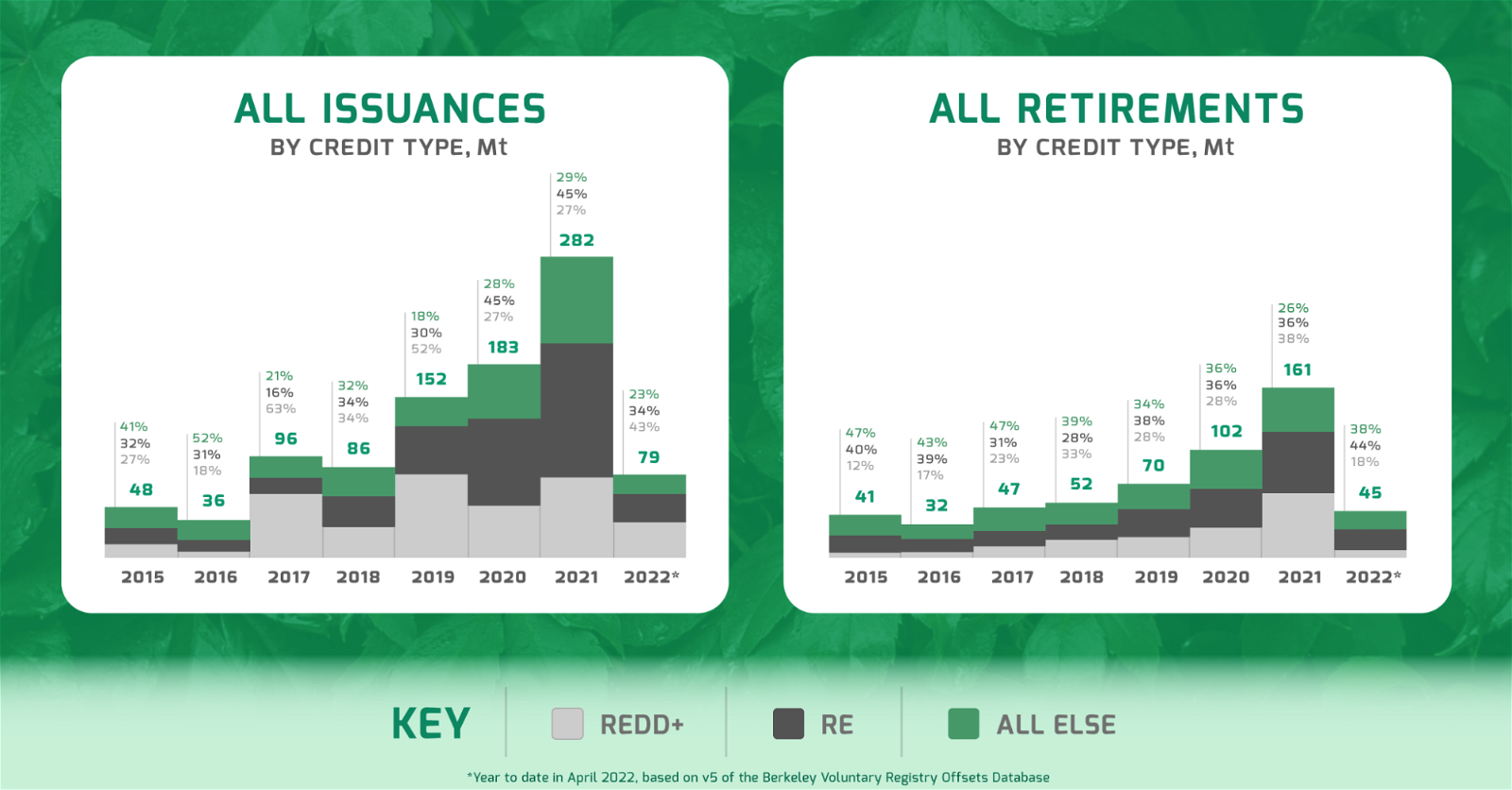

Our most recent analysis of the VROD shows that the most prevalent project types in both issuances and retirements are renewable energy (RE) and Reducing Emissions from Deforestation and (forest) Degradation (REDD+), which bear a range of risks related to offset quality.

In 2021, avoided deforestation (also listed as REDD+) and grid-scale RE, accounted for the majority of both issuances (77%) and retirements (79%). Many RE credits are non-additional – in other words, many of these projects may have or would have happened even without the help of finance from carbon offset sales[6]. As renewable power generation becomes more and more cost competitive with coal and gas, this risk will increase[7]. Meanwhile, the effects of REDD+ projects can be difficult to assess due to uncertainty in project baselines and potential leakage, which may lead to risks of overcrediting; REDD+ projects also risk causing negative impacts on local communities[8]. These challenges mean that many renewable energy and REDD+ projects do not deliver real abatement or deliver less abatement than credited in terms of avoided, reduced, or removed emissions.

Our findings here on quality risks with the most prevalent project types on today’s market echo findings of other efforts to track quality issues in carbon offset markets. Studies have found very high rates of over-crediting by all major offset programs that have developed offset protocols with credits available on the VCM, including the UN’s Clean Development Mechanism[9], California’s offset program[10]Badgley, G., Freeman, J., Hamman, J. J., Haya, B., Trugman, A. T., Anderegg, W. R. L., & Cullenward, D. (2021). Systematic over‐crediting in California’s forest carbon offsets program. Global … Continue reading, and a range of project types developed by the voluntary market registries, including soil carbon, improved cookstoves, and improved forest management[11].

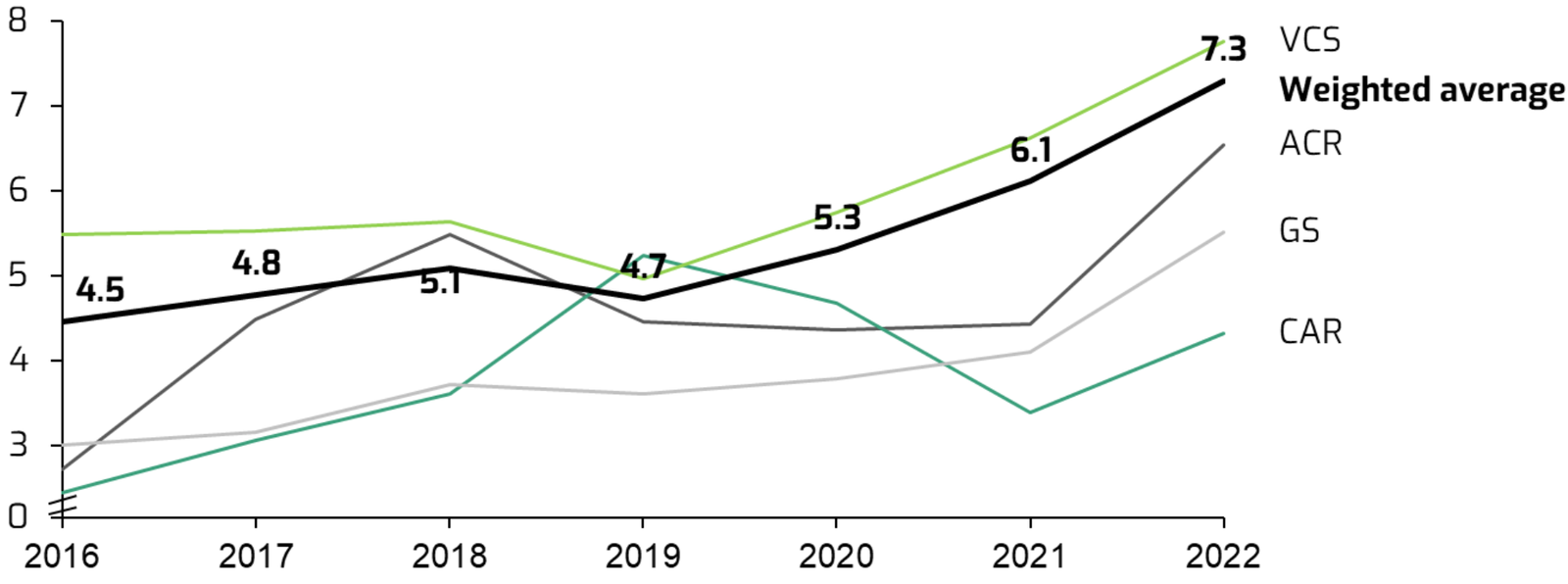

The average vintage age rose to 6.1 yrs in 2021 compared to 4.7 yrs in 2019 and 5.3 years in 2020. Retirement of older credits, including avoided deforestation projects older than ten years and renewable energy projects as old as fifteen years, drove this trend. Older projects often come from less mature protocols, can have weaker additionality claims given offset financing did not arrive until years later, and drive less immediate climate impact than new offset projects.

In 2021 suppliers issued nearly 300 Mt of carbon offsets, while retirers retired 161 M. This signal indicates that supply is growing faster than demand. This is complicated somewhat by non-retirement purchasing. Some buyers purchase credits for future use or reselling rather than for immediate retirement; as of April 2022, about half of 2020 purchases on the VCS remained unretired. Though not indicative of any quality issues on carbon offsets, it is important to note that retirement volumes are not the only demand signal to pay attention to.

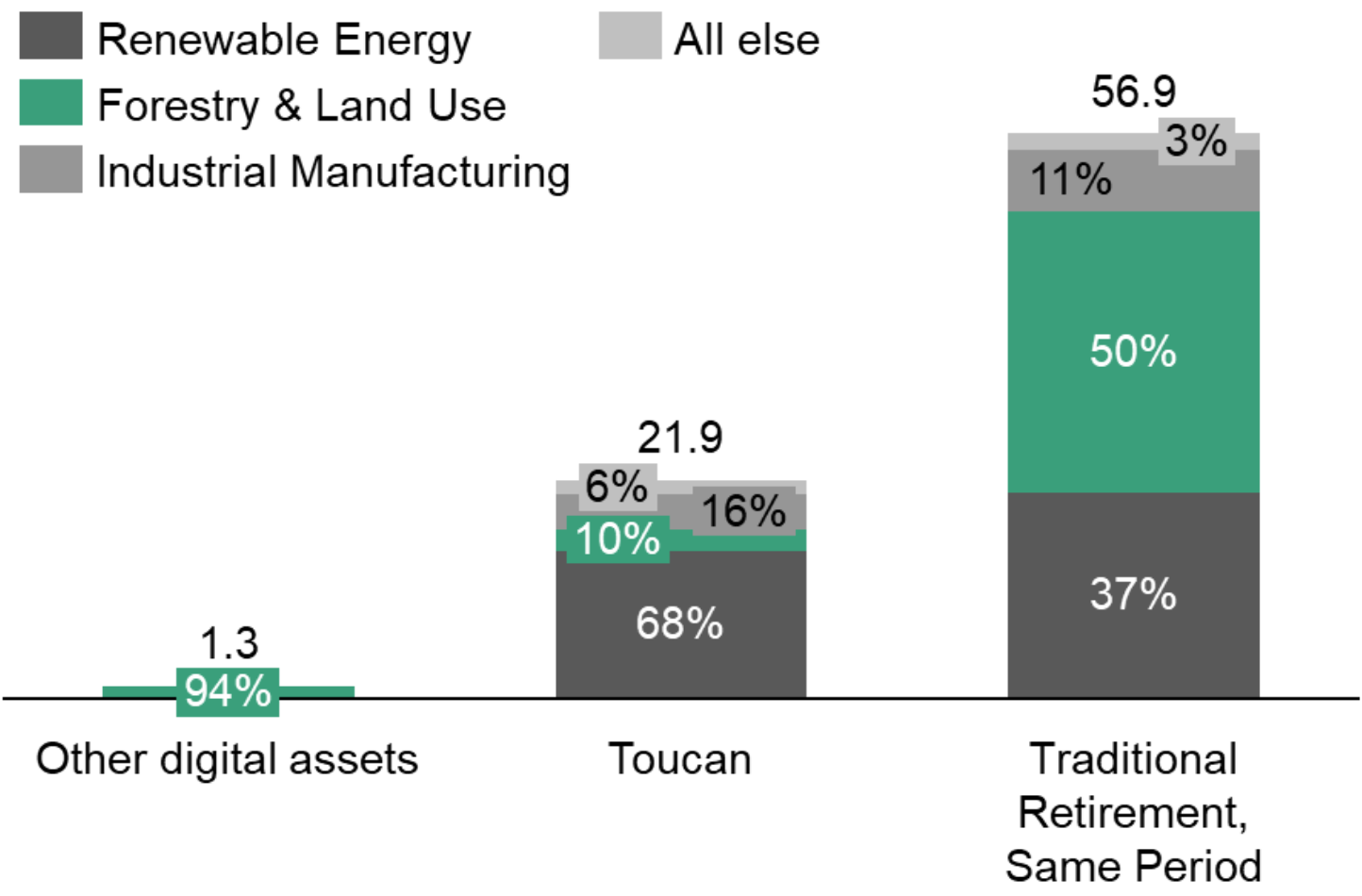

This new retirement type has driven significant retirement volume (representing ~40% of all retirements in Q4 of 2021). As some recent articles have noted, Blockchain’s retirement of old credits has not improved market quality[12]. For example, blockchain retirements in Toucan have largely featured older credits (mean retirement vintage of 2012) and composed primarily of renewable energy and forestry (~78%). In some instances, blockchain has enabled mass retirements of industrial manufacturing credits (such as large retirements from defunct version of the HFC-23 protocol which has been found to generate perverse incentives)[13].

The overall message is clear: the voluntary carbon market largely consists of projects of questionable quality with few removal options available. That trend has not yet reversed, but rather are made worse through blockchain programs as they currently exist.

Overall, these trends represent cause for concern as the offset market develops and matures. If the carbon offset credits lose widespread trust due to quality concerns, carbon markets cannot fulfill their key function: to drive capital to credible carbon reduction or carbon removal efforts. An offset market based on poor quality credits will erode the VCM’s long-term ability to turn voluntary purchasing into an engine for effective carbon management. In 2022 and across the next decade, actors on the voluntary carbon market must take actions to develop, issue, and retire high-quality carbon offsets and reverse the quality issues we see in the market today.

Instead, actors in the voluntary carbon market must work together to create a robust carbon market. We see the following actions as key to supporting a robust voluntary carbon market:

As 2030 and 2050 approach, we must adapt protocols and registries on the VCM to provide a platform that grows removal categories. Furthermore, credit retirers must seek to retire removals with greater long-term durability and quality. They should also retire younger projects (e.g., <5 years vintage) to increase additionality and overall quality carbon offsetting projects.

This article is also published on Carbon Direct. Future Thought Leaders is a democratic space presenting the thoughts and opinions of rising Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.

illuminem briefings

Effects · Climate Change

illuminem briefings

Public Governance · Climate Change

illuminem briefings

Public Governance · Climate Change

The Economist

Nature · Environmental Sustainability

UNDP

Adaptation · Climate Change

Offshore Energy

Carbon Capture & Storage · Carbon