AI’s energy impact, Chinese tariffs and ESG investment performance

· 4 min read

ESG ratings, mainly used for selecting investments and building portfolios, are derived from a set of key performance indicators (KPIs) to gauge corporate activity. But these KPIs, seen in isolation, don’t tell us anything about sustainability. It’s only when we know the KPIs' relationship to larger goals — for instance looking at corporate emissions in the context of the world carbon budget — that we can really talk about sustainability. There is a difference between ESG (usage of KPIs) and sustainability (acting in line with our world’s limitations).

In the last few days I’ve had many discussions about this, often from the perspective of ESG investment and its performance. The mood often seems to be more disappointed than euphoric. But perhaps that is just a sign that people are taking a harsh look at what has actually been achieved, and what still must be done.

From a real-world perspective, we have to accept that we are living with “limited room” (e.g. in terms of how much more punishment the earth can take). This isn’t news and many corporates are already acting accordingly. But looking at the problem from another perspective, does ESG investment-product design reflect what is really needed to create a sustainable future?

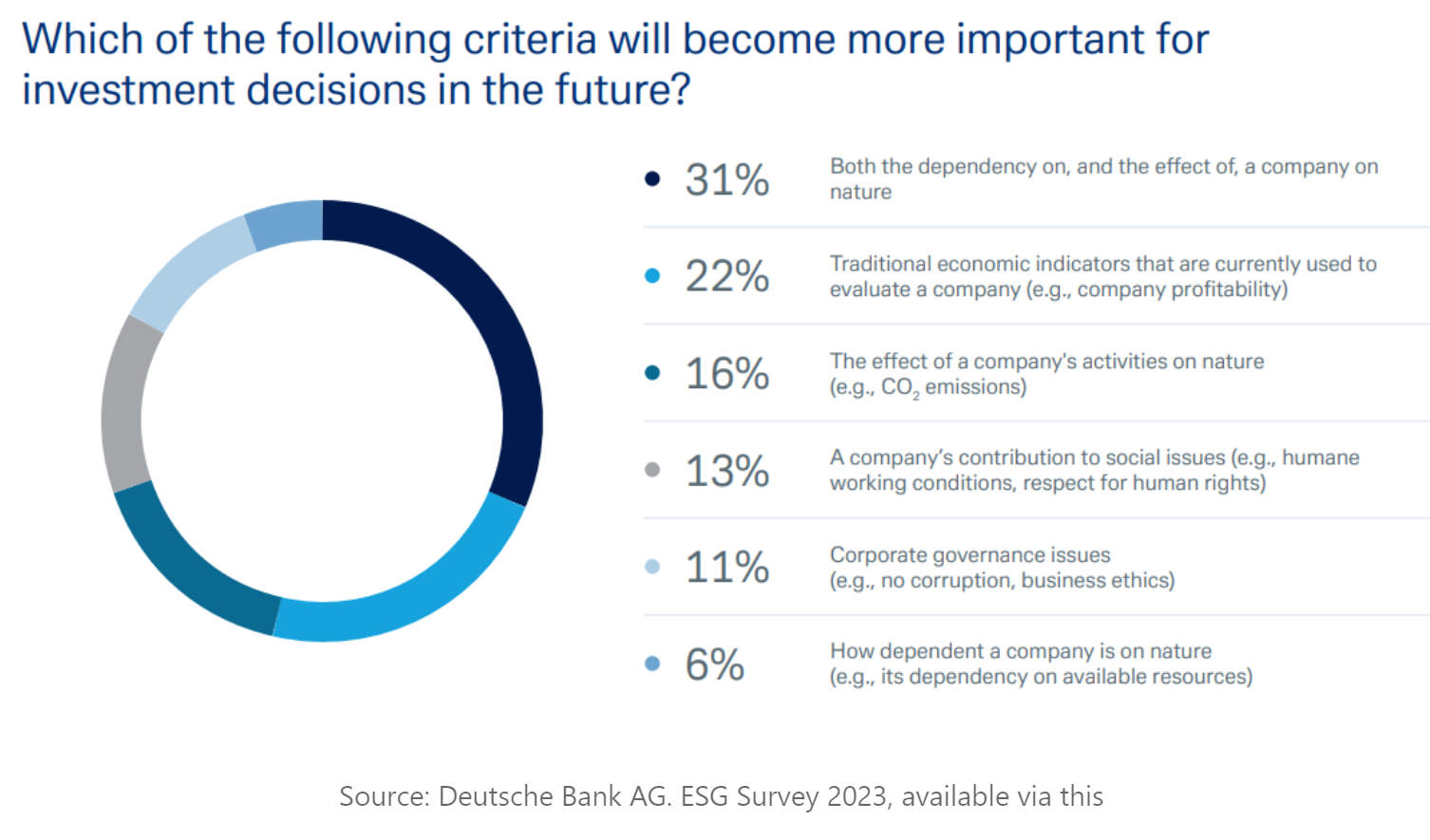

Regulation determines how ESG investment products can be built, with ratings guiding what can be included. But I wish I had greater confidence that current products really capture all of the sustainability requirements of the market.

ESG investment performance is important, even if you’re not an investor – it will affect levels of investment into the sustainability transformation — and strong performance can help to build general enthusiasm for sustainability. But analysing ESG performance isn’t just about sorting winners from losers: it also helps to show the importance of the details, like what’s included in the various ESG indices, and the impact of different comparison periods. It’s also important not to let relative performance measures distract from the bigger structural changes underway.

In May, President Biden proposed new tariffs on China’s “strategic” industries, including a 100% tariff on imports of Chinese EVs and a 50% tariff on solar cells. These new tariffs have been presented as a pre-emptive strike to protect U.S. industry from allegedly unfair competition. The expected impact, as the chart below shows, is a noticeable decrease in Chinese EV exports to the U.S. – with these exports rerouted elsewhere. But the immediate impact on the U.S. economy is likely to be small, with Chinese EVs having only limited presence in the U.S. auto market, unlike in Europe.

However, the tariffs will have long-term consequences. They could deepen a divide between U.S. and European attitudes to Chinese exports. (European attitudes have tended to be more conciliatory, given German industry’s exports to China). They could also encourage changes in trade structure and direction: will many Chinese exports simply be routed via final stage manufacturing activities in Mexico? (Trade patterns for vehicles are already changing, often in unexpected ways. Earlier this year, Ethiopia became the first country in the world to announce a total ban on imports of internal combustion engines.)

Structural change has also included some odd recent takeovers, for example by tech firms of renewable energy providers. A trigger has been the rapid ascent of artificial intelligence (AI) and its energy demands. According to Boston Consulting Group, data centres could account for as much as 7.5% of U.S. electricity consumption by 2030 (see graphic below).

We can already see the results of this in a number of deals between tech firms and energy providers. It also seems to be encouraging traditional energy firms to explore new possibilities (e.g. nuclear) and may already be having implications for expected future energy prices, encouraging new energy construction or bringing unused facilities back on stream.

The likely shift in the geographic distribution of data centres from traditional tech hubs to regions with better power availability and/or access to renewable energy (or nuclear power), will have multiple implications for local economies (e.g. real estate and necessary infrastructure investment). There are likely to be other knock-on technological effects, for example in the development of better cooling solutions (i.e. liquid cooling) to manage the heat produced by dense server stacks in data centres.

There could be transition problems, however. Energy-using data centres will, as discussed, spur investment into energy projects, advanced cooling technologies, and grid modernization efforts. But while we wait for the results, it may be difficult to meet growing demand for power in certain regions – perhaps triggering regulatory changes, with implications for distribution and pricing. So a very interesting investment area, but not completely straightforward.

This article is also published on the author's blog. illuminem Voices is a democratic space presenting the thoughts and opinions of leading Sustainability & Energy writers, their opinions do not necessarily represent those of illuminem.

Wil Burns

Carbon Removal · Carbon Capture & Storage

illuminem briefings

Climate Change · Effects

David McEwen

Climate Change · ESG

Time News

Climate Change · Adaptation

The Guardian

Effects · Climate Change

Politico

Public Governance · Climate Change