· 4 min read

Fulfilling the promise of the Paris Agreement will require the adoption of more ambitious emission reduction initiatives, as well as increased private and public commitments to be developing carbon offsetting projects as a way to neutralise the roughly 30% hard-to-abate emissions globally [1]. It is increasingly clear that well-designed voluntary carbon markets can help achieve this goal.

Carbon project developers play a central role in the voluntary carbon market (VCM). They source and initiate carbon offsetting projects around the world; they bring implementation partners and finance together, they work with carbon credit standards and verification bodies, they bear financial risks of carbon projects and work with a network of distributors and retailers to deliver auditable carbon offsetting claims in corporations' climate action programs.

However, it is clear that the VCM remains small in relation to the anticipated demand. With increasing pressure on corporations to show climate action, VCM demand is expected to grow x5-10 over the next ten years and x10-30 by 2050 from 95 million metric tonnes of CO2 equivalent (MtCO2e) in 2020, according to Trove Research [2].

We believe understanding the state of the carbon project developer ecosystem and its level of maturity can inform supply-side views on the market's ability to deliver on the integrity claims and volumes needed, as well as can shed light on the developers actively contributing expertise and know-how to the growth of this market.

Here are some key observations summarised below.

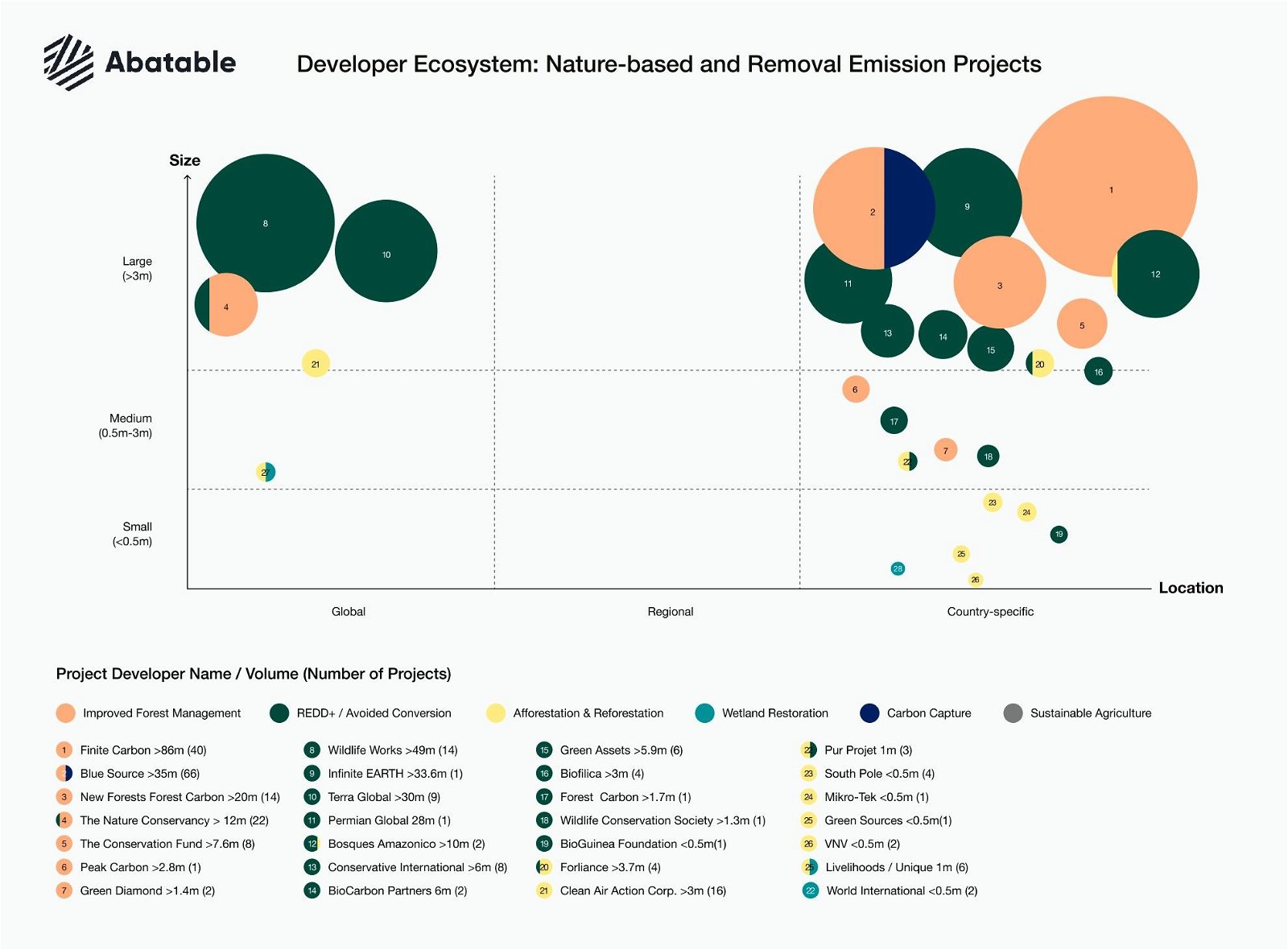

The carbon project developer ecosystem remains hyper-localised and highly concentrated by volume into a few carbon developers, with a long tail of small and mid-sized developers operating smaller carbon portfolios.

- The top 20 developers by number (out of 1382) account for over one third (39%) of total volumes issued to date, and the top 5 are responsible for 15% of all issuances. Three-quarters (75%) of developers by number have developed a single carbon project portfolio, and about the same percentage has issued less than 500,000 MtCO2e to date.

- 97% of developers have experience developing carbon projects only in one country, with very few global and regional operators. The developer market includes operators predominantly in India, the United States, China and Turkey. There are only a few developers implementing projects in Europe, despite many active offset buyers preferring projects in proximity to their operations.

- Notable deals announced this year suggest that intermediaries and capital providers have started forming partnerships with large developers or are considering acquiring carbon development platforms to internalise carbon project experience and accelerate carbon credit supply formation across regional and global portfolios. This trend may result in increased market consolidation with smaller carbon credit developers risking being overlooked by market participants.

Developers with experience developing avoided carbon emissions projects, such as renewable energy and industrial efficiency, dominate by number relative to nature-based.

- Developers with a focus on renewable energy projects were formed as a result of carbon finance incentives provided under the Clean Development Mechanism (CDM) during the period 2005-13 and before the market price collapsed for CDM credits, which have left developers with legacy avoidance portfolios questioned by buyers for poor quality criteria.

- Recent supply shifts see developers leverage carbon project development and verification expertise into nature-based projects in response to buyers' preferences for such projects. Lack of expertise in implementing more complex nature-based projects may result in developers' taking higher project development risks (e.g. biological growth uncertainty, fire and other natural climate risks) relative to the legacy, industrial-based projects.

- Within nature-based developers, outside of predominantly avoided emissions projects such as REDD+ or improved forest management, the number of developers and issuances in carbon removal projects, such as afforestation and reforestation or carbon capture, remains very limited.

Few nature-based avoidance developers may continue to lead by issuances due to high entry barriers.

- Nature-based developers represent over 45% of total carbon credit issuances. The market of developers with experience in nature-based projects is highly concentrated and remains small relative to demand.

- Most issuances are concentrated into a few large operators of large-scale avoided conversion and REDD+ projects (mainly in the Global South) or improved forest management projects (mainly in the United States). The latter continue to partner with large U.S. timberland funds to develop projects under state carbon programs (e.g. California’s Compliance Offsets Program under the cap-and-trade system).

- Buyer preferences are increasingly pushing developers towards nature-based solutions and removal credits, but in the absence of new market entrants, the market risks failing to meet short-term demand for removals, with potential pricing implications.

- Developers are equally focused on expanding large-scale nature-based avoidance carbon credits, which are estimated to be contributing significantly to supply in the next decade; however, those projects are jurisdictionally more complex to implement and may present higher barriers to entry.

This article summarises key findings of “The State of the Carbon Project Developer Ecosystem 2021”, a report published by Abatable which seeks to lay out key developer-level observations and better understand supply-side implications for the VCM.

Energy Voices is a democratic space presenting the thoughts and opinions of leading Energy & Sustainability writers, their opinions do not necessarily represent those of illuminem.